Value Quest Among Pricey Saudi Stocks Leads Some to Mouwasat

Quest for Value in Pricey Saudi Stocks Leads Some to Mouwasat

(Bloomberg) -- Saudi Arabian stocks are becoming pricier as the country heads for inclusion in major emerging-market benchmarks. But analysts believe they have spotted a bargain that may have been overlooked by many investors.

Mouwasat Medical Services Co., a health-care provider with a market value of about 7.6 billion riyals ($2 billion), is seen as an attractively valued and fundamentally interesting bet by firms ranging from Morgan Stanley to EFG Hermes Holding. Proponents say it stands out in an industry struggling with squeezed margins amid an exodus of expatriate employees following Crown Prince Mohammed bin Salman’s imposition of levies on foreign workers in 2018.

As stock gauges compiled by FTSE Russell and MSCI Inc. start including Saudi assets this year, several analysts see Mouwasat as among few companies listed in Riyadh that are more enticingly priced than global peers. It trades at a 12-month price-to-earnings multiple of 19, lower than the average of 23 for members of the MSCI EM Health Care Index. Using the same metric, Saudi Arabia’s Tadawul All Share Index has been more expensive than emerging-market benchmarks since November 2017.

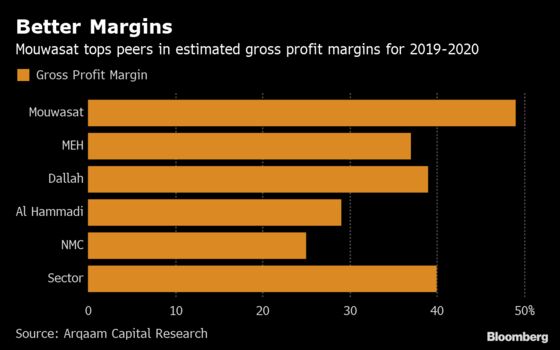

The earnings outlook is appealing to some too: Mouwasat’s gross profit margin remains in the high-40 percent range, far outpacing the figures for Saudi competitors, said Asim Bukhtiar, an analyst at Saudi Fransi Capital in Riyadh. Last month, Morgan Stanley’s Saul Rans upgraded the stock to overweight, calling it a “class leader.”

The company benefits from contracts with the Saudi Ministry of Health and accreditation for its hospitals from local, U.S. and European industry bodies enable the facilities to command higher premiums, according to Christine Kalindjian and Jaap Meijer, analysts at Arqaam Capital Ltd.

While EFG-Hermes Holding analysts including Hatem Alaa described Mouwasat’s fourth-quarter results as “disappointing,” they noted that the hospital operator’s first revenue decline since 2014 was related to the changed treatment of some costs under new accounting standards. Alaa has a buy recommendation on the stock and the highest price target among analysts tracked by Bloomberg, at 120 riyals. Mouwasat’s stock advanced 0.4 percent on Wednesday, trimming this month’s loss to 0.3 percent.

Here is more on how analysts view Mouwasat:

Morgan Stanley |

|

Arqaam Capital |

|

Saudi Fransi Capital |

|

EFG-Hermes |

|

To contact the reporters on this story: Abeer Abu Omar in Dubai at aabuomar@bloomberg.net;Filipe Pacheco in Dubai at fpacheco4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, John Viljoen, Hanna Hoikkala

©2019 Bloomberg L.P.