Quarterly Handoff in Treasury Shorts Is Riskier Than Normal

Quarterly Handoff in Treasury Shorts Is Riskier Than Normal

(Bloomberg) -- A decision that U.S. Treasury traders face every quarter around this time is more momentous than usual, in part because of speculation thatfunding-market strains will re-emerge in December.

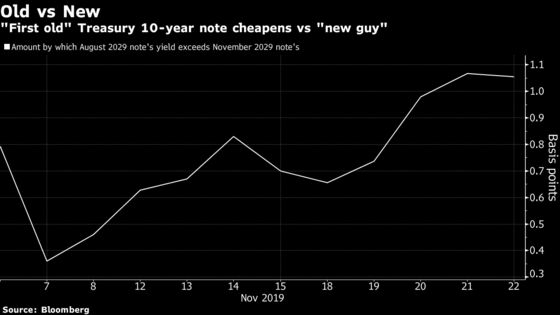

Traders must decide when to move -- or roll, in market parlance -- short positions into the newest security, shifting out of the second-newest one. In the 10-year maturity, for example, traders are now assessing when to roll short positions in the August 2029 note, which debuted in August, into the one issued this month that’s due in November 2029.

Because of the auction cycle -- in which a new 10-year is sold every quarter and expanded via reopenings in each of the next two months -- there’s initially more of the old issue than of the new one. There’s about $93 billion of the August 2029 10-year note outstanding, versus only around $40 billion of the November 2029 securities. The relative scarcity of the newer ones could make it costly to borrow to cover shorts, but their superior liquidity makes them cheaper to trade.

Other factors can affect the decision of when to roll over shorts, however, and two big ones are inducing some traders to hold off.

The first is indications of a large quantity of shorts in the old 10-year, which raises the specter of the current one becoming unusually expensive to borrow once shorts have been rolled. The second is the prospect that shorts in the old 10-year could benefit from a potential surge in overall repo rates in December, similar to the one seen in September.

Market Mystery

The quantity of shorts in a particular issue is normally a mystery, but there are clues. The main one is its repo rate, the cost of borrowing that specific issue, relative to the general collateral rate. An issue whose repo rate is lower -- meaning the borrower receives a lower rate on a loan of cash collateralized by the security -- than the general collateral rate is said to trade special.

As an issue grows in size via reopening auctions, it becomes less likely to trade special. The old 10-year traded special for nearly the entire time it was the newest issue, said Scott Skyrm, who works in sales and trading at Curvature Securities LLC, a securities lending broker-dealer.

“For a triple issue to trade even a little bit special is a big deal,” he said. It’s an indication of a large short base in the old 10-year, which could overwhelm the new issue if it were all to be rolled in a short period of time.

So far that hasn’t happened for overnight transactions. The financing rate for that period for the new 10-year averaged 1.59% Friday morning, just a few basis points lower than the general collateral rate, Skyrm said. For the old 10-year it averaged 1.52%.

But in an indication that traders expect the overnight rate to slump, the rate for financing the new 10-year over a term ending Dec. 16, when its first reopening will have settled, fell below 1% this week.

Why an issue trades special is likewise often a mystery, Skyrm said. It can be because the supply becomes restricted if a large holder doesn’t lend it out. In the case of the old 10-year, financial-market volatility from August through October probably played a role, he said.

But also, despite the Federal Reserve’s efforts to ensure that the banking system has enough reserves on hand, the prospect of another surge in the repo rate for general collateral in December is emboldening traders to keep their shorts in the old 10-year. When repo rates soar, holders of securities are punished by higher financing rates, but traders who borrow them for shorts benefit.

While the general collateral rate stabilized after the mid-September surge, and has stayed within a few basis points of 1.60% since the Fed’s Oct. 30 rate cut, the forward rate for the turn of the calendar year exceeded 3.5% this week. That’s causing traders to suspect that volatility is ahead.

“If you’re long securities and trying to finance them and rates go higher, it’s going to cost you,” said Subadra Rajappa, head of U.S. rates strategy at Societe Generale. “If you’re short it’s the opposite dynamic.”

To contact the reporter on this story: Elizabeth Stanton in New York at estanton@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Nick Baker

©2019 Bloomberg L.P.