Quant Factors Swing Most in a Decade in Wild Wall Street Trading

Quant Factors Swing Most in a Decade in Wild Wall Street Trading

(Bloomberg) -- Quants are getting lashed by some of the most violent stock swings in more than a decade as fears of a second virus outbreak fuel huge waves of selling on Wall Street.

With the Federal Reserve sounding the alarm on the long road to an economic recovery, systematic traders betting on reflation are getting crushed in the S&P’s biggest plunge since March’s mayhem.

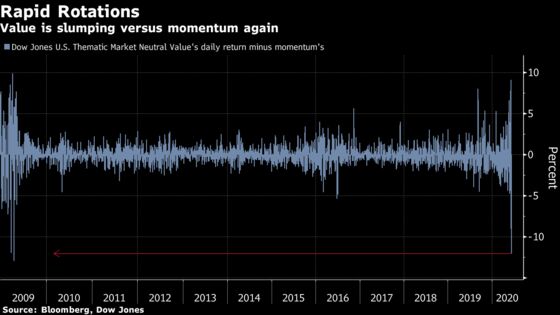

The value factor versus momentum is on track for its third-worst performance since 2009 in Thursday trading. The popular investing style -- which scoops up cheap companies over recent market winners -- posted its biggest loss since the global financial crisis on Wednesday.

Investors are dialing back the optimism that turbo-charged stocks back toward records in the grip of the recession, while new American infections raise fresh fears about a once-in-a-century pandemic.

As the S&P 500 tumbles more than 5%, cyclicals from banks to energy producers are selling off by the most since March. All the whiplash is creating big allocation headaches for quants who dissect companies by their traits from how cheap they look to how much their share prices have rallied.

“Value is representative of a lot of beaten-up names,” said Sean Phayre, the global head of quantitative investments at Aberdeen Standard Investments. “It remains to be seen how much impact the unprecedented support from governments and central bank agencies will actually have.”

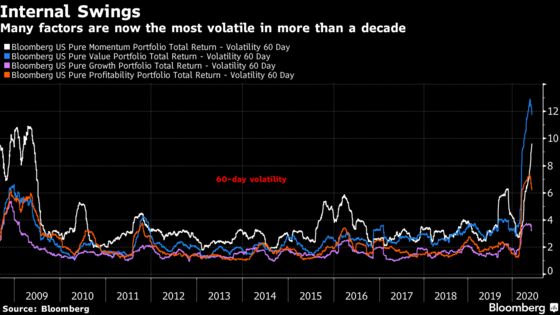

Another sign of whiplash on Wall Street: the size factor, which wagers on small caps, had its worst day since 2009 on Wednesday, after a volatile revival in recent weeks between stimulus cheers and pandemic fears.

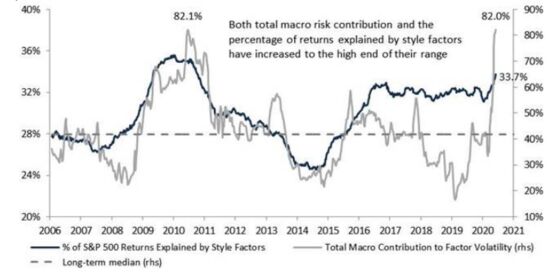

Factors are now accounting for the highest portion of the S&P 500’s returns in about a decade, Evercore ISI’s analysis shows.

That’s a sign that active investors are likely struggling to make strategic calls on individual companies on the basis of traditional metrics like earnings. Instead Evercore’s analysis suggests factor exposures -- intended or otherwise -- appear to be driving large swings in portfolio returns. Macro risks are now driving 82% of factor volatility, the highest in about 10 years, it says.

All this is happening under the surface and hard to say for sure. But one thing is clear: The risk-on rotation in late May was almost as violent as the March madness, as optimism over economic re-openings drove investors to underperforming factors such as value and size.

Gyrations in the Treasury curve are playing a role. Value stocks like banks tend to be more cyclical and dependent on near-term cash flows, whereas growth stocks like Facebook Inc. are pricey because of their promise of long-term profit expansion. Because of this, a steeper yield curve tends to bode well for stocks that look cheap relative to fundamental metrics like corporate earnings.

“Equities have moved from the ‘non-linear’ world of distressed debt investing to the more ‘linear world’ of earnings revisions, sales growth and valuations,” Jefferies strategists led by Sean Darby wrote in a Wednesday note before the Fed meeting. “From the nadir of the steepening of the U.S. yield curve, the market has rewarded more value-orientated sectors.”

Yet after the U.S. central bank policy decision, key segments of the Treasury yield curve flattened, a move signaling economic pessimism that flashes bad news for riskier investing strategies.

Still, the relationship between macro trends and factor returns is hotly contested among quants. Many argue that bond moves should never affect factor allocation while the sharp discount in value stocks is reason enough to be bullish.

Unprecedented fiscal and monetary stimulus could potentially deliver all manner of bullish surprises in the months ahead, says Aberdeen Standard’s Phayre. That’s why the quant is sticking with the value in his multi-factor model.

“When it does rally, it rallies so hard and so fast that if you’re not in it, you’ll have missed it pretty quickly and that can be quite painful,” he said.

©2020 Bloomberg L.P.