Putting Libor Out of Its Misery Is Proving Easier Said Than Done

Putting Libor Out of Its Misery Is Proving Easier Said Than Done

(Bloomberg) -- Weaning off the scandal-plagued Libor benchmark is a gigantic problem for global rates markets, one that increasingly looks too burdensome for a single replacement to handle in the U.S.

Global regulators decided to move away from the London interbank offered rate -- a vital part of the financial system given that it’s linked to, at last count, about $350 trillion of loans, derivatives and other instruments across various currencies -- after prosecutors found that banks around the world manipulated it. It also didn’t help that volumes underlying the benchmark dried up. For the U.S., a group backed by the Federal Reserve picked something called the Secured Overnight Financing Rate, or SOFR. It launched a year ago Wednesday.

But the Bank for International Settlements, which serves as the bank for central banks, said in March that a one-size-fits-all alternative may be neither feasible nor desirable. Although SOFR solves the rigging problem, it doesn’t help participants gauge how stressed global funding markets are. That means SOFR is likely to coexist with something else.

“The market likes the idea of having something that has credit risk embedded in it, so if the market wants it, I’m not sure the Fed is going to be able to stop it,” said Mark Cabana, head of U.S. interest rates strategy at Bank of America Corp.

How this actually plays out in the U.S. is uncertain. Revamping Libor itself makes sense given that it remains the guidepost for fixed-income markets. Intercontinental Exchange Inc.’s ICE Benchmark Administration division, which oversees Libor, has outlined another possible successor called the Bank Yield Index. Another option is Ameribor, the brainchild of Richard Sandor, who in the 1970s helped invent the interest-rate futures market while serving as the Chicago Board of Trade’s chief economist.

Here are the leading contenders, and their pros and cons:

SOFR: The Heir Presumptive

SOFR, which debuted in April 2018, is set daily based on overnight repurchase agreement transactions secured by U.S. Treasuries. It was the preferred benchmark of the Fed’s Alternative Reference Rates Committee, a collection of regulators and representatives from the private sector. Futures and other derivatives linked to it are already trading. Right now, it’s just tied to overnight funding, but officials intend to introduce longer-term rates.

- Pros:

- There’s already a lot of trading in the repo markets that underpin it, with volume on related securities averaging about $843 billion a day since the benchmark’s launch a year ago, according to data compiled by the Fed Bank of New York. That’s vastly more than the median daily volume of funding transactions that support three-month Libor, which is less than $1 billion.

- The SOFR futures market is growing. Total open interest in CME Group Inc.’s one- and three-month SOFR futures contracts was roughly 149,000 as of March 19, up from about 51,000 at the beginning of 2019.

- The Federal Home Loan Banks, the largest issue of short-term Libor-linked debt, are issuing floating-rate securities tied to SOFR. FHLBs have issued about $32 billion of the securities since November.

- Cons:

- It got quirky around the end of 2018, surging from 2.46 percent on Dec. 28 to 3.15 percent on Jan. 2, then back down to 2.45 percent two days later. Since then, the rate has jumped by about 20 basis points at the end of each month. Many downplayed the significance of this jumpiness, explaining that SOFR-linked repos got tumultuous as banks tidied up their balance sheets at the end of the year, when regulatory surcharges are calculated. But it does show funding conditions could rile the rate in the future.

- While total open interest on SOFR futures continues to rise, the number of swaps transactions is erratic. Swaps transactions amounted to about $13.1 billion of notional value in March, a new monthly record, according to data compiled by Depository Trust & Clearing Corp. Yet $10 billion of that was simply hedging against the possibility that repo rates would spike at the end of the quarter.

- Market participants are still awaiting the creation of a term structure, or maturities beyond overnight. Libor and other rates already have these, but minutes from the Federal Open Market Committee’s January meeting showed the central bank is still working on this area for SOFR. Fed staff issued a paper in February about inferring term rates from SOFR futures prices.

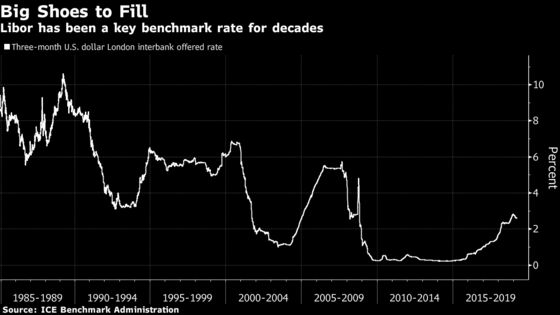

Libor: The Devil You Know

Through a daily survey, about 20 large banks estimate how much it costs to borrow from each other without putting up collateral. Since taking over Libor from the British Bankers’ Association in 2014, ICE Benchmark Administration has tweaked the rate’s calculation to incorporate commercial-paper transactions when possible. These are real trades, not just estimates, and act as a guard against manipulation.

- Pros:

- The market is still huge. Despite the push from regulators to shift outstanding contracts to a new reference rate, more than $350 trillion of securities are still tied to Libor across currencies, with $200 trillion of that denominated in dollars.

- Because it’s based on wholesale bank transactions, Libor currently acts as a key benchmark of credit risk in the global financial system.

- Libor gives a longer-term peek into funding conditions because it’s published across seven maturities, ranging from overnight to one year.

- Cons:

- Volumes for transactions that underpin Libor have been anemic lately compared with those tied to SOFR and the upstart Ameribor rate.

- Regulators believe there’s still a stigma surrounding Libor because of the rigging scandal.

- Now that the benchmark is calculated from actual trades -- through the use of what’s called a waterfall methodology -- it may be more sensitive to changes in bank funding conditions. For example, the three-month tenor plunged by 4 basis points on Feb. 7, the largest one-day slide since May 2009.

U.S. Dollar ICE Bank Yield Index: Not Quite There

The Bank Yield Index was introduced by Libor’s overseer, ICE Benchmark Administration, or IBA, in January. The new gauge is designed to measure the yields at which investors are willing to lend U.S. dollars to large, internationally active banks on a wholesale, unsecured basis to meet the needs of lenders, borrowers and other cash-market participants.

- Pros:

- The Bank Yield Index is based entirely on real trades, including banks’ commercial paper and certificate of deposit transactions.

- No single issuer is allowed to represent more than 10 percent of the transactions used to determine the rate, an attempt to prevent a single firm from skewing the result.

- It looks at more than overnight rates, with IBA producing it on a preliminary basis for one-, three- and six-month tenors.

- Cons

- It’s not ready yet. IBA collected feedback from market participants through March 31. IBA hopes to begin publishing the rate in the first quarter of 2020.

- Despite being transaction-based, the bigger issue is that unsecured bank funding remains thin after regulations stemming from the 2008 financial crisis. This is a problem it has in common with Libor.

- IBA has said there’s no guarantee it will continue to test BYI, be able to source the data or publish the index in the future. It advised Libor users not to rely on its potential publication when devising Libor transition or fallback plans.

Ameribor: The Dark Horse

This nascent daily benchmark reflects the borrowing costs for transactions between members of the American Financial Exchange -- small- and mid-size U.S. financial institutions, mostly banks.

- Pros:

- Unlike SOFR, Ameribor has been steady at month- and year-end periods.

- Since launching in December 2015, both volumes and the number of users have grown. The exchange had roughly 700 banks on its platform as of the end of March, with average daily outstanding volume amounting to $1.45 billion. That’s up from 11 institutions and $13 million in volume when it started out.

- In addition, commercial banks have started issuing loans tied to Ameribor. On March 5, Brookline Bank in Boston become the second bank to issue a commercial loan indexed to the reference rate, with more in the pipeline, American Financial Exchange Chairman and Chief Executive Officer Sandor said. He also said that Ameribor futures are planned for the second or third quarters.

- Cons

- Its global breadth is unknown. Ameribor targets financing conditions for smaller U.S. banks, whereas Libor and BYI are more geared toward dollar-denominated global funding conditions for multinational financial institutions.

- The term structure is in its infancy. The American Financial Exchange intends to move further out the curve with the creation of a 90-day rate, although it has only recently introduced a 30-day tenor.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker

©2019 Bloomberg L.P.