Profit Pinch Worse Than It Looks With 40% of S&P 500 in Decline

Profit Pinch Worse Than It Looks With 40% of S&P 500 in Decline

(Bloomberg) -- It may be time to worry about earnings season.

Behind a benign facade, things are getting dicey ahead of the first-quarter reporting season that begins in about a month. Weakening profit growth forms a big plank in the case against U.S. stocks. Anxiety about income growth starred as a central villain in last quarter’s market meltdown.

For one thing, the number of companies that are about to report falling first-quarter profits keeps going up. More than 200 firms in the S&P 500 are now expected to earn less than they did a year ago, data compiled by Bloomberg show. That’s a lot more than were in the same boat three years ago, a stretch generally viewed as the worst profit recession of the bull market.

While it’s true that the shallowness of the likely drop has spurred many on Wall Street to brush it off as temporary, the growing breadth has become grist for bears who say the first quarter could be the beginning of something that poses a bigger threat to the 10-year rally.

“This is a broad earnings recession, stemming from broad economic issues,” said Rich Weiss, chief investment officer and senior portfolio manager of multi-asset strategies at American Century Investments. “Very few sectors, if any, can come through unscathed.”

Things that weigh on bottom lines are multiplying. Global demand has sagged and the dollar has rallied. Oil prices are down and workers are getting paid more. More ominously for investors who have watched quarter after quarter of surging profits underpin a quadrupling in the S&P 500: once earnings start to fall, it’s hard to stop.

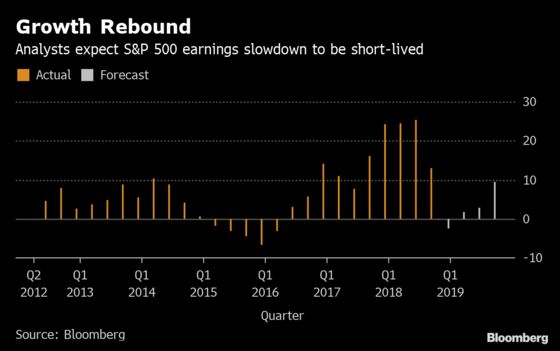

Analysts expect S&P 500 earnings to fall 3 percent during the January-March period before bouncing back for the rest of the year, sparing corporate America a prolonged downturn.

While the decline isn’t as bad as the one at the worst point of the 2015-2016 contraction, its breadth is new. Back then, the whole drop had a single explanation: falling oil prices. Excluding energy producers, S&P 500 profit would have increased.

Now only three industries are forecast to show positive growth: industrial, health-care and utilities. Technology, the biggest group in the S&P 500, may report a 9 percent decline, while energy and materials companies each suffer a 15 percent drop.

Not everyone sees this as a catastrophe. Strategists at Credit Suisse and Goldman Sachs have argued that the current downturn is heavily influenced by the likes of Apple Inc. and other large companies that account for much of the S&P 500’s weight. To BMO Capital Markets, the expected dip is so shallow that if companies repeat their tradition of beating estimates, profits may end up rising.

And stocks have kept advancing despite a persistent reduction in corporate guidance. This quarter is the first time in four years when negative outlooks were greeted by higher share prices, according to data compiled by Morgan Stanley.

“The earnings recession is real and it’s broader than the one we experienced in 2015-16,” Mike Wilson, Morgan Stanley’s chief U.S. equity strategist, wrote in a note Monday. “Until we see counter evidence that these cuts are reversing these negative margin trends, we think the risk is still to the downside for more disappointing releases which is likely to weigh on stock prices.”

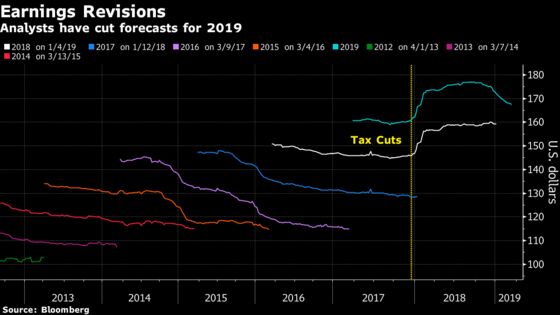

Analysts have reduced their 2019 earnings estimates by 5 percent since September to $167.80 a share. At current levels, that gives the S&P 500 a price-earnings ratio of 16.7. It’s hardly expensive when 10-year Treasury yields hovered near 2.6 percent. But it’s not cheap either, given an average multiple of 16.6 over the past five years.

As much as bulls hope that the first-quarter deterioration will be transitory, history shows that profit declines tend to cluster. Since 1937, only 10 percent of the quarterly slides have lasted exactly three months, data compiled by S&P Dow Jones Indices and Bloomberg showed. In the 18 instances where profits fell by three quarters or more, all but four were accompanied by bear markets.

“The U.S. economy is in the middle of a ‘soft patch’ that is likely to last three to four months,” said Chris Senyek, chief investment strategist at Wolfe Research. “Our sense is that current quarter earnings results are going to be underwhelming and that management guidance is likely to remain lackluster as well,” he added. “We are tactically cautious and recommend positioning portfolios defensively until economic readings take a positive turn.”

--With assistance from Wendy Soong.

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Chris Nagi, Richard Richtmyer

©2019 Bloomberg L.P.