Powell’s Hawkish Tone Fails to Tamp Down Inflation Expectations

Powell’s Hawkish Tone Fails to Tamp Down Inflation Expectations

(Bloomberg) -- Federal Reserve Chairman Jerome Powell is amping up his hawkish tone. Still, the U.S. central bank’s favored bond-market measure of long-run inflation expectations keeps rising. That’s a problem.

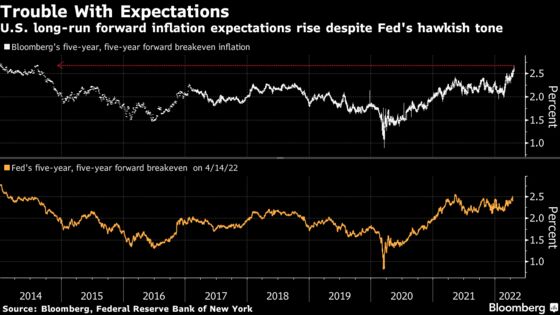

A day after Powell outlined his most aggressive approach to taming inflation to date, the so-called 5-year, 5-year forward breakeven rate, which measures investor expectations for price pressures over the half decade that begins in 2027, reached its highest since mid-2014, according to data compiled by Bloomberg. The Fed has used that measure since the early 2000s to help guide policy; they have their own model, which as of its latest update on April 14 was at its 2022 high.

U.S. central bankers have long believed that expectations for inflation ultimately can drive actual price pressures, whose current pace of increases already has the Fed scrambling to rein them in. On Thursday, Powell endorsed two or more half percentage-point interest-rate increases, leading bond traders to price in four of them by the end of September.

“Notwithstanding all the tightening expected to come, it has done absolutely nothing to quell inflation expectations in the TIPS market,” said Peter Boockvar, chief investment officer at Bleakley Advisory Group. Higher inflation is “the kryptonite that has exposed” Fed policy failures, he said.

The 10-year spot breakeven rate reached a record high on Friday at 3.08%, while the 30-year measure has plowed to its highest for 2022.

Breakeven rates are derived from comparing yields on Treasury Inflation Protected Securities (TIPS) and ordinary Treasuries. The forward rate uses a mix of both five- and 10-year TIPS and nominal Treasuries. Such a mix was seen as ideal by D.E. Shaw’s Brian Sack when he was at the Fed, partly as it strips out temporary inflation factors.

The Fed’s initial hawkish pivot late last year, after months of saying decade-high consumer prices would prove transitory, tamped down inflation expectations, but the move hasn’t lasted. The central bank has been slammed by some as being too slow, putting policy makers in catch-up mode. Federal Reserve Bank of St. Louis President James Bullard said this week that the central bank shouldn’t rule out rate increases of 75 basis points.

At the Fed’s policy meeting last month staffers raised the possibility that elevated inflation could cause longer-term inflation expectations to become unanchored. It’s a risk, on a global basis, that the International Monetary Fund cited as well on Tuesday. U.S. consumer prices rose 8.5% in March from a year earlier, the most since late 1981.

TIPS are tied to consumer prices, which have historically exceeded the inflation measure that the Fed targets -- the personal consumption expenditure index -- by about 40 basis points. Thus, ten-year TIPS show the market is pricing the Fed’s preferred gauge as averaging about 2.66% annually over the coming decade -- above the central bank’s 2% target.

Official signals for a front-loaded and aggressive monetary tightening to come is making some headway toward tightening financial conditions, something the Fed desires, with stocks sliding and short-term Treasury yields rising Friday.

“Stocks are weaker this morning on the conviction behind faster policy tightening,” said Jim Vogel, an analyst at FHN Financial. “Yet, the list of markets marching stubbornly on an upward trend is longer. The highlights: government yield curves, commodities, inflation expectations, corporate bond issuance are all largely undisturbed -- implying tightening guidance to date is still too little too late.”

©2022 Bloomberg L.P.