Powell Resets Fed Goals for Job Market in Light of Covid Reality

Powell Resets Fed Goals for Job Market in Light of Covid Reality

(Bloomberg) -- Federal Reserve Chair Jerome Powell has tempered his ambition to restore the labor market to its pre-pandemic strength, as the central bank confronts surging inflation and a workforce still constrained by Covid-19.

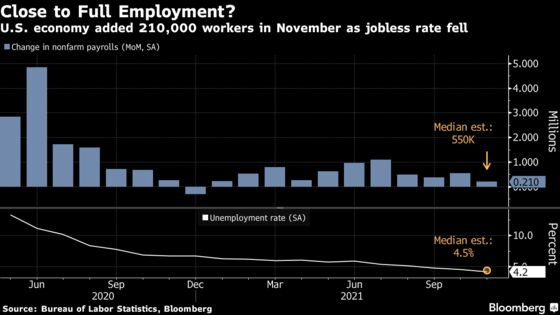

The Fed on Wednesday reiterated that reaching full employment was an expected step for raising interest rates, but officials also penciled in three hikes in 2022. While about 3.9 million workers are still missing on payrolls, Powell said maximum employment needs to be defined in the context of the “reality” of today and that the U.S. is already very close to the mark.

“We’re not going back to the same economy we had in February of 2020,” Powell said at a press conference following a meeting of the Federal Open Market Committee. Early on, that had been the sense of where the country was headed, he said. But not any more: “The post-pandemic labor market and the economy in general will be different.”

The Fed hasn’t given an explicit definition of its employment goal. Powell said the evolving definition of what a full-employment labor market would look like is subjective and a committee judgment, unlike the more tangible definition of reaching the 2% inflation goal. In previous press conferences and speeches, Powell and other Fed officials have cited the shortfall of millions of jobs from the February 2020 level as slack that would return to the labor market.

Powell and his colleagues have come to see that the labor force will be constrained by continuing issues caused by the virus, said Diane Swonk, chief economist at Grant Thornton LLP.

“The idea that we return to pre-pandemic norms requires the pandemic to abate, which it hasn’t. Within the context of where we are, it is past time that the Fed acknowledges we move beyond pre-pandemic norms,” she said. “The one constant of the Powell’s tenure as Fed chair is his humility and willingness to adjust course when necessary. He shows no hubris.”

But some saw Powell’s remarks as backtracking on prior guidance that Fed officials would be patient before raising rates in order to achieve full employment that was both broad and inclusive.

“They are trying to redefine what maximum employment means,” said Aneta Markowska, chief U.S. financial economist at Jefferies LLC. “Up until now they said they would look at broad measures of slack, and all of that seems to be out the window basically. He was pretty explicit: He said there were structural reasons that participation is down and we don’t have the luxury of time because inflation is high right now.”

The chair, defending the progress already made toward restoring maximum employment, cited the rapid decline in the jobless rate to 4.2%, which is near the 4% level that officials see as full employment. He also called out record job openings, increasing wages, rising numbers of people quitting their jobs and improvements among how various demographic groups are faring.

“The labor market is, by so many measures, hotter than it ever ran in the last expansion,” Powell said, hearkening back to a period that, before the pandemic, delivered the lowest unemployment rate since 1969.

What Bloomberg Economics Says

“Powell reiterated several times that the labor market is making “rapid” progress toward maximum employment. He also said he does not expect it to return to the February 2020 level. Given the rate at which the labor market is approaching maximum employment, he does not anticipate the committee will need to invoke the provision in the Fed’s framework that specifies what to do when the two components of the dual mandate are in tension with one another.”

-- Anna Wong, Yelena Shulyatyeva, Andrew Husby and Eliza Winger

The one measure that has been “disappointing” has been labor-force participation, Powell said. While there had been the expectation that many workers would return in the fall with schools reopening, that didn’t happen. Still, the chair made it clear that metric alone wouldn’t be enough to stop interest-rate hikes.

“The reality is we don’t have a strong labor-force participation recovery yet, and we may not have it for some time,” Powell said. “At the same time, we have to make policy now. And inflation is well above target, so this is something we need to take into take into account.”

The latest shift represents a change for other Fed policy makers too. Fed Richmond President Thomas Barkin, among others, has cited the percentage of Americans who are employed as a key metric. It remains far below its peak before Covid.

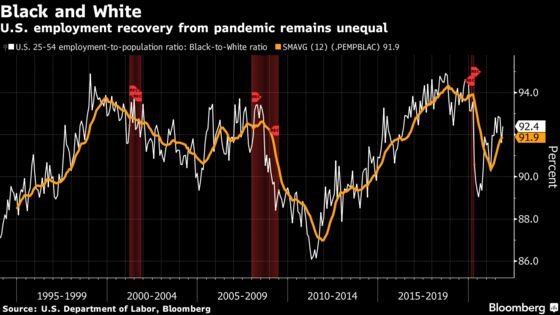

What’s more, the Fed’s new policy framework, adopted before inflation became a hot issue, called for full employment to be defined as a goal that is “broad-based and inclusive,” indicating all groups should be faring well in the job market.

The 4.2% unemployment rate last month was still above the 3.5% rate that prevailed before the pandemic, but way down from the peak of 14.8% in April 2020. In November the White unemployment rate was 3.7% while the Black unemployment rate was 6.7%.

“The Fed is embracing the Great Resignation theme,” said Thomas Costerg, senior U.S. economist at Pictet Wealth Management. It’s a “sudden U-turn from the Fed, which has long highlighted the hidden slack in the labor market to turn very suddenly and now highlight the quit rate and the very tight labor market.”

Among the indicators, Powell spent some time in his press briefing highlighting the quits rate, which is near a record, as a sign of workers’ confidence in the job market.

It’s “one of the very best indicators” and suggests a very tight labor market, he said. It was also a favorite labor market indicator of former Chair Janet Yellen, now Treasury secretary.

“I wouldn’t say they’re throwing in the towel on full employment but rather gradually learning what that means in this environment,” said JPMorgan Chase & Co. chief U.S. economist Michael Feroli.

©2021 Bloomberg L.P.