Powell Faces Tough Campaign to Convince Traders of Fed’s Resolve

Powell Faces Tough Campaign to Convince Traders of Fed’s Resolve

(Bloomberg) -- The Federal Reserve succeeded in pushing back against market expectations for a rate hike in the next two years, but only partially.

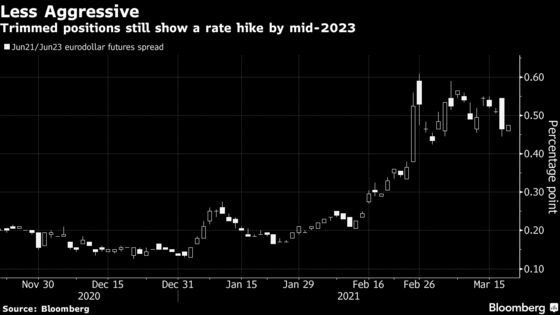

The central bank envisages keeping rates near zero to the end of 2023 despite a significantly brighter assessment of growth and higher inflation over the near term. After the release, traders trimmed some of the more-aggressive positioning they’ve been building for a “lift-off” by earlier in 2023.

But a 25 basis-point hike by the first quarter that year is still reflected in Eurodollar futures, which are priced off Libor and are a decent proxy for future borrowing costs. So traders haven’t exactly brought their views on the timing that much closer to the central bank’s guidance.

“The market will need to be reminded again and again of the Fed’s commitment” to support the recovery, said Anne Mathias, global rates and currencies strategist at Vanguard Group Inc. “If higher yields don’t slow the economy down, don’t upset the stock market, don’t upset risk-taking, then the Fed doesn’t need to push back hard against them,” she said in an interview.

Current rates-market pricing reflects a lingering conviction that the pace of the recovery will spur the Fed to action, earlier than it anticipates, though Chair Jerome Powell reiterated Wednesday that the Fed needs to see “substantial further progress” on its employment and inflation goals before thinking about a hike.

That statement helped short-end rates fall. Seven-year yields remained elevated, however, which suggests positioning for higher interest rates may be building further out the curve. A later rate hike could force the central bank to move faster to tame inflation.

Market gauges of inflation expectations imply some faith in the central bank’s ability to keep it under control. The five-year breakeven rate, which is derived from the difference between yields on Treasuries and their inflation-protected counterparts, is around the highest since 2008, at 2.63%. That compares with a lower 10-year breakeven rate showing price pressures returning to the Fed’s target over the decade.

That chimes with the Fed’s guidance, in Mathias’s view.

“We’re going to see some interim inflation pressure from pent-up spending,” she said. “Net-net, though, the overall secular forces that have kept inflation at bay have not changed.”

©2021 Bloomberg L.P.