ADVERTISEMENT

Pound Option Traders Are Not as Short as Risk Reversals Suggest

Pound Option Traders Are Not as Short as Risk Reversals Suggest

17 Oct 2018, 04:01 PM IST

(Bloomberg) -- While the option market is the most bearish on the pound in two years amid Brexit anxiety, it’s by no means a one-way street.

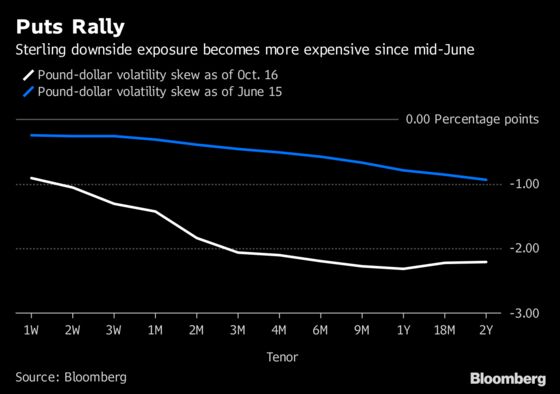

Demand for sterling calls has been almost as strong as that for puts since mid-June, data from the Depository Trust & Clearing Corporation show, even as risk reversals showed faster increases in the cost of contracts to bet on pound weakness.

- While pound volatility rose disproportionately in favor of put options over the past four months, demand for structures benefiting from a stronger sterling haven’t been out of vogue

- Looking back at trades since mid-June, when a strong rally in risk reversals led by puts started at the back end of the curve, a total notional of 297 billion pounds ($391 billion) traded for vanilla options. Out of these, 155 billion pounds represented put structures, or 52 percent

- By and large, the difference in implied volatilities between similar-maturity call and put options reflects market expectations in terms of the direction of a pair and reveals investors’ positioning. A negative number, especially a deep one as that for pound risk reversals, suggests the market expects a substantial move downward in the U.K. currency

- In theory, this would translate to traders adding dollar calls by a greater margin; reality suggests that either investors are hedging short-pound cash positions or simply taking advantage of relative cheap pricing to bet on Brexit resolution

- The pound could gain more than 2% to $1.35 if a divorce deal is agreed, or slide as low as $1.20 if Britain crashes out of the bloc without an economic agreement, according to strategists

- NOTE: Vassilis Karamanis is an FX and rates strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

To contact the reporter on this story: Vassilis Karamanis in Athens at vkaramanis1@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma, Neil Chatterjee

©2018 Bloomberg L.P.