Position Squeeze Could Be Behind U.S. Negative-Rate Pricing

Position Squeeze Could Be Behind U.S. Negative-Rate Pricing

(Bloomberg) -- Wrong-footed positioning -- not fresh expectations of a historic shift in Federal Reserve policy -- could be the reason why futures markets are starting to price in negative U.S. interest rates.

A build-up of short positions in fed funds futures contracts could have resulted in a squeeze Thursday, forcing a mass of traders to hit the exit at the same time and push rate expectations below zero, according to Wall Street strategists. They recommended investors fade the move.

“Markets may be undergoing a repositioning or short squeeze — akin to the recent move in oil futures,” TD Securities’ Priya Misra and Gennadiy Goldberg wrote in a note Thursday. “We do not think this is justified by fundamentals as FOMC members have repeatedly stated that they do not expect to take rates negative.”

JPMorgan Chase & Co. strategist Jay Barry agreed, suggesting investors may have been positioned for higher yields, after the Treasury announced earlier this week a surge in T-bill supply was on the way.

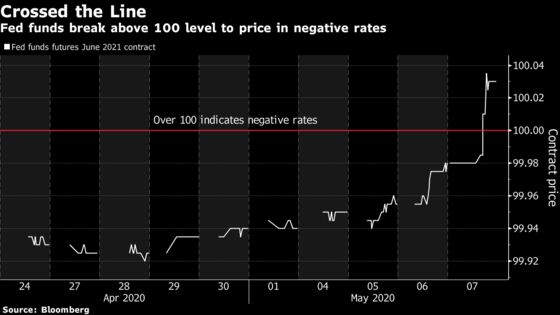

The January fed funds futures contract reached a peak of 100.025 on Thursday in New York -- a record high -- indicating a policy rate of negative two and a half basis points.

A host of dovish rhetoric from Fed officials has reignited speculation of negative U.S. rates after Chairman Jerome Powell dismissed the idea in March. Two-year Treasury yields sank to a record low Thursday as officials including Minneapolis Fed President Neel Kashkari sounded a cautious note about the U.S. economy’s recovery from the virus pandemic.

Many strategists recommended traders fade the move. The TD Securities duo suggested investors sell July 2021 fed funds futures, while strategists at Bank of America preferred expressing this view using January 2021 overnight index swaps.

©2020 Bloomberg L.P.