Poloz Enters Home Stretch Hawkish on Rates

Poloz Enters Home Stretch Hawkish on Rates: Decision Day Guide

(Bloomberg) --

Stephen Poloz is heading into the final few months of his term as Bank of Canada governor showing few signs of giving up his status as one of the industrialized world’s most hawkish central bankers.

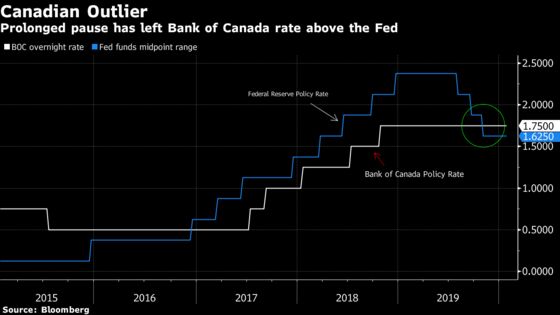

At a decision Wednesday, the bank is widely expected to hold its key interest rate at 1.75%, keeping it unchanged for a 10th-straight meeting and leaving Canada with the highest rate among advanced economies.

Markets also don’t see much chance that Poloz, who leaves office in June, will lower borrowing costs in any of his final three meetings after this one, with odds of a cut at less than 40% over that time. That’s despite having reason to cut, given the economy looks to have slowed sharply at the end of last year.

Here are some of the reasons why he’s seen remaining on hold:

Neutral Tone

In public appearances since October, including a number from Poloz, officials have sought to accentuate the positive, highlighting the nation’s strong jobs market and on-target inflation. At the same time, they’ve been reluctant to put much stock in weaker indicators they say are transitory.

Last month, Deputy Governor Timothy Lane defended the Bank of Canada’s decision to buck the global easing trend, saying the nation’s resilient economy is allowing it to “chart its own course in monetary policy.”

“The more that we hear from Bank of Canada the less they seem willing” to cut rates, said Frances Donald, Toronto-based global chief economist at Manulife Investment Management.

Inflation

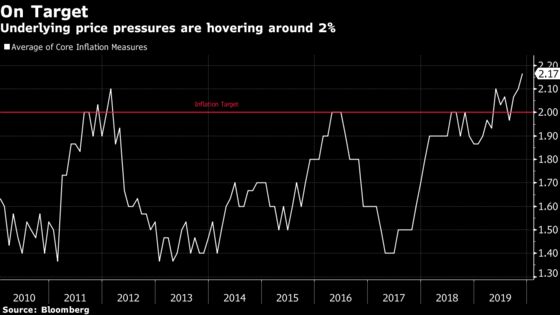

Underlying price pressure as measured by core inflation has been stable near the Bank of Canada’s 2% target for about two years. That reflects an economy running nicely at around its capacity -- neither too hot nor too cold.

Of course, what matters more for policy makers is where inflation is headed rather than where it’s been, and the central bank will update its outlook with new quarterly forecasts on Wednesday. They will probably revise down fourth quarter growth estimates, from their October projection of 1.3%. Growth is trending at less than 1% for the final three months of last year, according to the latest Bloomberg survey of economists.

But the net effect of the changes isn’t clear. For all of 2019, growth may be higher than the bank previously forecast because upward historical revisions by Statistics Canada means the economy probably had less slack to begin with.

A weak fourth quarter also doesn’t necessarily mean the central bank will cut its growth forecasts for 2020, given the stabilizing outlook for the global economy and some positive developments on the trade front.

Home Prices

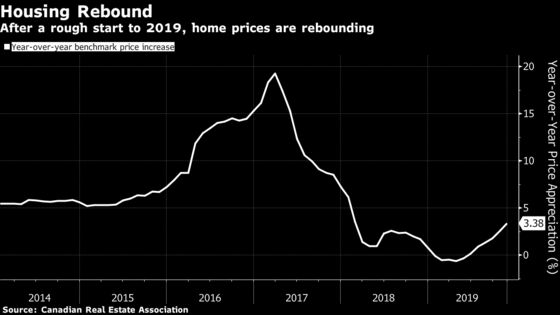

Officials sometimes downplay the extent to which household debt and financial stability factor into rate setting, but the recent housing rebound and acceleration in borrowing will only amplify their concern.

Poloz highlighted the possibility earlier this month that speculative activity is returning in some major real estate markets. That’s one more reason not to cut.

Core Mandate

To be sure, Poloz won’t hesitate to lower rates if there’s a discernible worsening in the outlook. The central bank’s primary inflation-targeting objective is aimed at ensuring the economy grows at a sustainable pace over the medium term. Financial stability is a secondary concern.

So if the data continue to disappoint, a rate cut may be in the offing. While investors are sanguine about a move, nine of 17 economists surveyed by Bloomberg are anticipating at least one rate cut by June.

| What Bloomberg’s Economists Say |

|---|

“Bloomberg Economics still sees a compelling case for an easing adjustment by midyear, though we acknowledge a call for a cut as soon as March is in clear jeopardy depending on the BoC’s post-meeting messaging” -Andrew Husby, Bloomberg Economics Click here for the full report |

Nor, if history is any guide, will Poloz’s imminent departure hinder him from acting. David Dodge cut rates in his final decision as governor in January 2008. So did Gordon Thiessen in 2001.

That said, as long as the economy remains in a relatively good place and household debt levels continue to pick up, Poloz may be content to simply stand pat before he stands down.

To contact the reporter on this story: Theophilos Argitis in Ottawa at targitis@bloomberg.net

To contact the editors responsible for this story: Theophilos Argitis at targitis@bloomberg.net, Chris Fournier, Stephen Wicary

©2020 Bloomberg L.P.