A Plastic-Maker That Was Crushed in 2019 Is Now a Top Pick for 2020

A Plastic-Maker That Was Crushed in 2019 Is Now a Top Pick for 2020

(Bloomberg) -- There’s no containing the excitement on the Street for Berry Global Group Inc. Negative sentiment on plastic be damned.

The Evansville, Indiana-based containers and plastics company has been named the top pick for 2020 by almost all of the analysts covering the industry, including those at Goldman Sachs and Robert W Baird & Co Inc. The recommendations follow Berry’s underperformance against its peers in 2019, attributed in part to mounting debt concerns, slow-to-no growth and environmental worries.

After avoiding a sell rating from the Street for its entire history, Berry Global now has analysts going one step further, pounding the table for 2020 with bets the company can expand sales, lower debt and increase free cash flow. “We think a combination of much easier year-ago comparisons and discrete new business wins” in Engineered Materials and Health, Hygiene and Specialties units “will drive modest volume growth in FY’20,” Goldman Sachs analyst Brian Maguire wrote in a note naming Berry the “most compelling risk-reward idea for 2020.”

In 2019, even as corporate borrowing costs tumbled, concern about Berry’s junk-rated debt emerged. Debt/Ebitda had been on the decline since Apollo Global took the company public in 2012 with debt levels in excess of Berry’s peers. But “mis-execution, investor concerns over balance sheet leverage and what we characterize as peak plastics packaging negativity” weighed on the stock last year, according to Baird analyst Ghansham Panjabi.

Even with the leverage, however, Wall Street continued to sing its praises. The stock never prompted a sell rating, even when shares hit highs in 2018 and the valuation was most elevated in 2012/2013, according to data compiled by Bloomberg.

If analysts are correct, it’s possible that 2020 may be the year for a breakout. “Given our confidence on the volume improvement dynamic and our view that the narrative on plastics packaging should be better balanced 2020 onwards (driven by technology for chemical recycling), we believe that the shares of BERY are in a gradual valuation multiple expansion phase that should drive outperformance in 2020,” Baird’s Panjabi wrote.

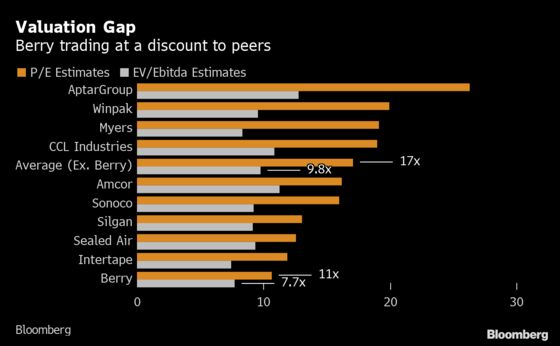

Lending credence to the idea is the stark valuation gap versus other plastic packagers, based on the average estimates among analysts. Berry’s price-to-earnings multiple for the next twelve months is about 10.7 times, which is a 37% discount to the peer average of 17 times. And Berry’s enterprise value-to-Ebitda estimate is 7.7 times, or a 21% discount to a peer average of 9.8 times.

The 2020 outlook, then, for Berry’s share prices seems to be bright, with just a few more minds to change -- only 2 analysts have anything but a buy rating, according to data compiled by Bloomberg. The most reluctant, however, are advocating caution until dynamics change.

Morgan Stanley analyst Neel Kumar, who has the lowest price target on the stock with a hold-equivalent rating, said that although Berry “is better positioned into F2020, we believe the company will likely continue to trade at a discount to peers until it is able to consistently demonstrate volume growth.”

To contact the reporter on this story: Aoyon Ashraf in Toronto at aashraf7@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Scott Schnipper

©2020 Bloomberg L.P.