Pimco Warns That Central Banks Can’t Rescue the Bond Market

Pimco Warns That Central Banks Can’t Rescue the Bond Market

(Bloomberg Opinion) -- Pacific Investment Management Co. has a new secular outlook. Suffice it to say, the fixed-income behemoth isn’t looking at the debt markets through rose-colored glasses.

“We have probably the riskiest credit market that we have ever had,” said Scott Mather, chief investment officer of U.S. core strategies at Pimco. It’s like before the financial crisis, he said. “We see it in the buildup in corporate leverage, the decline in credit quality, and declining underwriting standards — all this late-cycle credit behavior we began to see in 2005 and 2006.” Meanwhile, ever-popular collateralized loan obligations will bear the brunt of losses in leveraged loans when the business cycle turns, according to portfolio manager Beth MacLean. And to top it off, the U.S.-China trade war is poised to cut into already decelerating global growth, noted Tiffany Wilding, Pimco’s U.S. economist. A recession in advanced economies might be in the cards in the next three to five years, the period covered in the firm’s outlook.

Basically, as Pimco Global Economic Adviser Joachim Fels put it to Bloomberg Televison’s Jonathan Ferro: “We’re seeing the end of an era. … We’re now entering an age of disruption.”

Frankly, those concerns aren’t exactly novel. The fact that a growing share of the U.S. investment-grade corporate bond market is rated triple-B is so well-known by now that I’ve argued it’s unlikely to be the flashpoint for a crisis specifically because the risks are so well telegraphed. As for CLOs, well, they own two-thirds of the leveraged-loan market, so it’s only natural they’d be the ones suffering a big hit when weak covenants come back to haunt investors — again, a much-publicized issue. And MacLean specifically highlighted the equity portion of the structures as taking much of the potentially $150 billion in losses, which is exactly what they’re supposed to do to shield highly rated tranches.

Rather than those warnings, what caught my attention from Pimco was an idea that should be somewhat scary to all investors — that central banks are no longer all-powerful and don’t have the capacity to help support markets. Here are some select quotes from Mather:

“Markets have become used to an environment where central banks are really powerful in terms of taking volatility out of the market and pumping asset prices up. That era is coming to an end.”

“The U.S. is about the only central bank that was able to normalize policy rates, but elsewhere, there’s basically no monetary firepower left.”

“People are starting to come to a more realistic outlook about both the forward-looking growth prospects, as well as the power of central banks to pump up asset prices.”

There’s nothing much to disagree with there. The European Central Bank and the Bank of Japan have done virtually nothing to scale back their extraordinary stimulus measures and appear destined to keep current policies indefinitely. The Federal Reserve was at least able to boost interest rates several times and reduce the size of its balance sheet, but it has less room than ever to maneuver in the next downturn. In fact, Bloomberg Opinion did a six-part series just last month that envisioned what the Fed could do to better combat a potential recession.

Some investors will surely say they’d welcome the end of central-bank meddling in markets. With great volatility comes great opportunities, after all. Indeed, Pimco’s Fels, Andrew Balls and Dan Ivascyn wrote in their outlook that the firm “will emphasize flexibility to respond to events, keeping some powder dry and emphasizing liquidity over chasing the very highest yields.”

Still, active managers’ swagger aside, the prospect of weakened central banks raises serious and difficult questions about how the world’s leading economies will foster growth in the years ahead. To some, the obvious answer is a boost in fiscal spending, as advocates of Modern Monetary Theory suggest. Others, like BlackRock Inc.’s Rick Rieder, have floated even more unconventional ideas from the monetary policy side, like having the ECB team up with regional governments to buy equities. And then there are those who say that persistently low interest rates have completely backfired because individuals are forced to sock away ever-larger sums of money just to make the same return, rather than spend today.

For now, Pimco’s executives simply urged investors to play defense by investing in Treasuries and U.S.-guaranteed mortgage-backed securities. Of course, that would have been a better move seven months ago, when 10-year yields were about 100 basis points higher than they are today. But if their outlook is correct, and central banks can’t do much to contain market turbulence, hiding in havens still looks like a good wager.

Of course, there’s always the possibility that Pimco is underestimating the Fed, ECB and BOJ. Mario Draghi’s pledge to do “whatever it takes” will go down in history as effectively summing up policy making in the post-financial crisis era, as will the mantra of “don’t fight the Fed.” While it’s risky to project the recent past onto the future, it’s worth remembering that investors who have gone against central banks have often been burned.

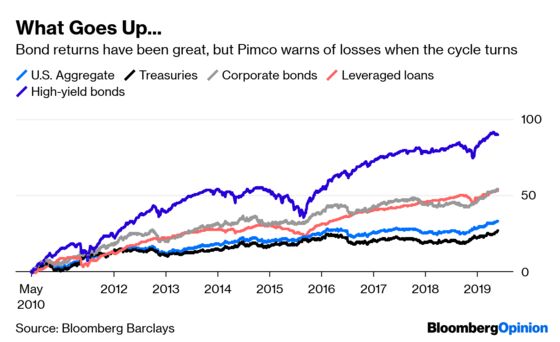

At the very least, Pimco is raising some important red flags and reminding investors that the current fixed-income environment — 8% year-to-date returns on U.S. high-yield, 6.6% on investment-grade corporate bonds, 3.4% on Treasuries — can’t go on forever. But with interest rates as low as they are, it can last for quite some time.

Conspicuously, Pimco didn’t specify what will bring about the end of the current era, nor precisely when the cycle will turn. Even the riskiest credit market ever is merely a “vulnerability” and “not at the point where it will fall of its own weight.” It turns out timing the future is hard, even for a $1.76 trillion asset manager. But the overarching message out of Newport Beach, California, is clear: Bond investors ought to be vigilant.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.