Pimco Turns to Distressed Debt, Muni Bonds for Aussie Yield Play

Pimco Turns to Distressed Debt, Muni Bonds for Aussie Yield Play

(Bloomberg) -- Investors shunning record-low yields should consider buying distressed debt and Australian semi-government bonds that are likely to benefit from ultra-loose monetary policy, according to Pacific Investment Management Co.

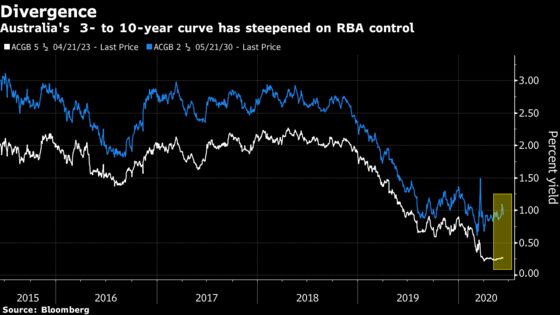

The Reserve Bank of Australia’s pledge to anchor three-year yields around the record-low 25% cash rate means funds should consider traveling further out the yield curve to find value, said Robert Mead, the firm’s Sydney-based co-head of Asia-Pacific portfolio management.

Among his top picks are Australian sovereign notes maturing in five-to-seven years, state paper and debt of companies that have come under pressure amid the global coronavirus pandemic.

“Investors want more than 25 basis points, and I think there’s plenty of opportunity for them to earn more,” Mead said on Bloomberg’s Inside Track webinar series. “We’ve seen the reaction function from the Fed, the ECB, from the Bank of Japan all being very supportive of the high quality credit market.”

Junk bonds to municipal debt have rallied as central banks around the world slashed interest-rates and rolled out multi-trillion dollars worth of monetary stimulus to rescue economies ravaged by the virus. Setting the RBA apart from developed peers is its effort to control short-dated yields at the 0.25% level -- a strategy that has allowed longer-dated bonds to trade freely and opened opportunities to bet on spreads.

Investors are “able to pick up literally percentage points for taking very little additional risk” when investing in securities such as semi-government debt, Mead said.

There will also be “great opportunity” to invest in distressed credit as businesses come under pressure from pandemic-induced losses, he said. At the heart of this is central bank support, with the likes of the U.S. Federal Reserve and European Central bank buying sub-investment grade debt as part of efforts to stimulate their economies.

There are signs this phenomenon is well underway: in Europe, the amount of distressed debt has halved from its peak this year, according to JPMorgan Chase & Co.

“While economies are recovering, they’re not moving back to where they were anytime soon,” he said. There should be “tremendous levels of subordination supporting bond investors” over the next two to three years as ultra-loose monetary policy works its way through the system.

©2020 Bloomberg L.P.