Pimco Sees Defaults Rising in Asia as Stimulus Is Wound Back

Pimco Sees Defaults Rising in Asia as Stimulus Is Wound Back

(Bloomberg) -- Company debt defaults are set to rise as policy makers cut back on widespread support and shift toward more targeted pandemic spending, according to Pacific Investment Management Co.

Trillions in government and central bank spending have shielded a majority of companies from the worst of the epidemic but this may not continue, said Robert Mead, Pimco’s co-head of Asia-Pacific portfolio management in Sydney.

“The next phase of policy will be much more targeted” globally, Mead said. For companies that are too highly leveraged or struggling to conduct business in a post-pandemic world, “we think a lot more of those will be allowed to fail.”

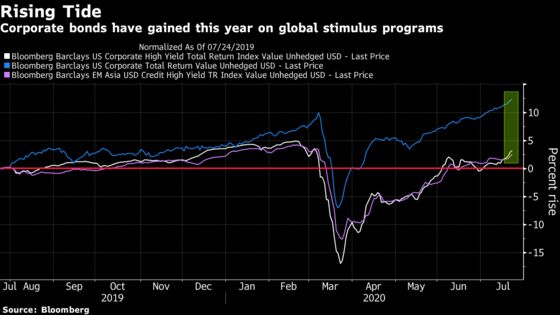

From Goldman Sachs Group Inc. to Moody’s Investors Service, analysts are warning that debt delinquency could rise as a drawn-out pandemic chokes off demand and dries up businesses’ cash flow. Policy makers including the Federal Reserve have pledged to keep stimulus pumping for as long as needed to sustain growth.

The trend may already be underway: a growing number of Asian firms are deferring their bond payments on mounting financial stress, while a rising number of investment-grade companies are slipping into junk territory.

“You can almost count on one hand the number of defaults that are taking place around the world, and we think that the potential for high-yield defaults to potentially be double digit,” said Mead.

He points to Australia’s example where new measures to safeguard jobs will be offered at a lower rate.

“There’s an unrealistic assumption that the policy will save every company,” he said. “Policy will be much more selective, much more targeted going forward and that will have implications for every section of the economy globally.”

Pimco likes well-managed investment grade companies which understand their leverage, Mead said. It also favors new distressed debt deals as their covenants are such that they tend to offer better protection.

Here are some of Mead’s other edited market views:

Roll Strategy

In our Aussie curve positions, we like to buy securities that roll down to the three-year point, given the yield-curve control of around 25 basis points in that part of the curve. We like the five-to-seven years, and taking advantage of spreads in the semi-government market.

Rangebound Treasuries

We’re in the middle of the range in 10-year U.S. Treasury yields. The Fed is likely to be on hold for an extended period, we don’t see any sort of inflationary pressures given the backdrop of unemployment.

Debt-Buying Programs

To the extent that there are QE programs around the world, there’s a flavor of direct support in government bond programs as a coordinated policy response. The most important thing though is to have a limited time frame within which these programs exist. There needs to be a very rapid move into a black and white, clear view that central banks are independent.

RBA Tools

It’s unlikely the RBA will enter into too much rhetoric around the Aussie dollar. There are policy tools they can use to influence the currency indirectly, they’ve been supportive through RMBS programs, through the Australian Office of Financial Management. They’ve also been absent from their QE bond buying program for months now, I think that would be their next natural move if they did feel like financial conditions were getting too tight.

Aussie Appeal

The bond’s curve is pretty steep, the attractiveness for foreign investors to buy Australian bonds hedged is still there. It’s about the high yield, combined with the economic and inflation outlook, the quality of the AAA bond. There are a lot of things global investors, local investors should find relatively attractive.

©2020 Bloomberg L.P.