PG&E Faces a Crisis of Confidence Crisis From Wall Street to San Francisco

PG&E Faces a Crisis of Confidence Crisis From Wall Street to San Francisco

(Bloomberg) -- PG&E Corp.’s financial woes have spiraled into a crisis of confidence on Wall Street and beyond after fallout from deadly wildfires hobbled the company’s credit rating and eviscerated more than $16 billion of market value.

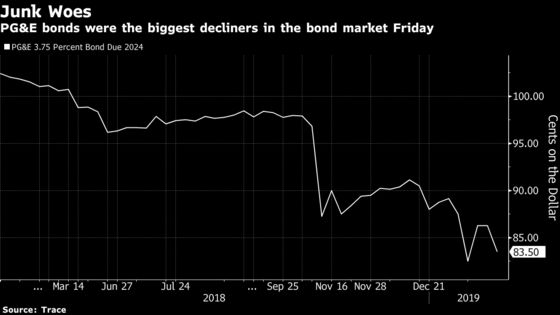

The embattled California power giant’s bonds were among the biggest decliners in the high-yield market Friday. On Thursday, protesters interrupted a California Public Utilities Commission meeting in San Francisco with cries of “perjury” and “murder.”

The onslaught of bad news and public ire engulfing the utility comes as it faces billions of dollars in potential liabilities from blazes in 2017 and 2018 that left more than 100 dead. PG&E’s value has dropped by almost two-thirds since November’s deadly Camp fire began, and it’s said to be considering filing for bankruptcy. Credit agencies have downgraded the company and its debt to junk status, with S&P Global Ratings citing PG&E’s history of legal infractions.

“This is beyond an isolated episode and outside industry norms and leads to an adverse impact on the company’s reputation,” S&P Global Ratings credit analyst Gabe Grosberg said in a statement.

Citigroup Inc. said PG&E faces “a crisis of confidence.” Guggenheim Securities analysts likened the dilemma it poses to investors and lawmakers as “a falling knife.”

The shares declined 1 percent to $17.59 at the close in New York. The utility’s bonds saw mixed performance Friday afternoon. A 6.25 percent note due in 2039 dropped 1.75 cents on the dollar to 87.25 cents on the dollar, but other debt from the company rallied as much as 3.75 cents. Junk downgrades can force some investment-grade bondholders to sell their securities, but also open up a new buyer base of high-yield investors.

Thursday’s turbulence at the California Public Utilities Commission meeting turned what began as procedural meeting into shouting match. Protesters piled in to fight efforts to pass costs to customers for billions of dollars in potential wildfire liabilities. Then state regulators disappointed investors by failing to offer assurances they’ll help keep the utility solvent.

Finally, Moody’s Investors Service Inc. cut PG&E’s credit to junk Thursday, a move that will force the San Francisco-based company to post cash collateral and will kick it out of the biggest investment-grade bond index.

“The other shoe has dropped,” said Carol Levenson, research director at Gimme Credit LLC, in a note Thursday. “This thing is snowballing now that the rating agencies have finally acted (essentially closing capital markets access), which might be the tipping point in favor of a bankruptcy decision.”

PG&E’s credit woes are being felt elsewhere, as well: S&P Global Ratings cut the credit rating of Berkshire Hathaway Energy’s 550-megawatt Topaz Solar Farms to junk, noting the plant counts on PG&E for its revenue.

California’s new governor, Gavin Newsom, hasn’t said whether he’s willing to craft a legislative bailout for PG&E. During an unrelated press conference Thursday, he would only go so far as to say that PG&E’s troubles were at the top of his agenda. Later, in an interview, he said that he’d be appointing people in the next few days to a panel that’ll tackle utility-related wildfire issues.

‘Significant Lobbying’

The California Public Utilities Commission didn’t offer anything by way of assurances to PG&E investors either. Drowned out by cries of “murder,” “perjury” and “manslaughter” from a dozen or so activists, the agency agreed Thursday to open proceedings to develop a so-called stress test for utilities’ wildfire costs. The goal is to see how big a financial blow companies like PG&E can withstand and still remain viable.

“These protests at a procedural CPUC vote lead us to expect significant lobbying against PCG in the legislature, in a repeat of the anti-PCG efforts seen last summer,” Clayton Allen and Katie Bays, analysts at Height Securities LLC, wrote in a note early Friday, referring to the company’s ticker. “This further reduces our expectations that any legislation could move quickly.”

Meanwhile, PG&E now has two junk ratings, following a downgrade earlier this week by S&P Global Ratings. That means it will be required to use cash as collateral to guarantee power contracts, according to the company’s latest quarterly filing, which estimates the utility will have to fully collateralize as much as $800 million of positions. It had $430 million of cash on its books in September, according to a regulatory filing.

Moody’s lowered PG&E’s rating by five notches, to B2 from Baa3, and utility unit Pacific Gas & Electric’s rating by four levels to Ba3. The credit grader also said it may cut the company further.

“We see a much more challenging environment for PG&E,” Moody’s analyst Jeff Cassella said in a statement. “The company is increasingly reliant on extraordinary intervention by legislators and regulators, which may not occur soon enough or be of sufficient magnitude to address these adverse developments.”

In response to its downgrades, PG&E said by email that it’s “actively assessing PG&E’s operations, finances, management, structure and governance — and remains focused on improving safety and operational effectiveness.”

--With assistance from Romy Varghese, Claire Boston, Rebecca Choong Wilkins and Michael Bellusci.

To contact the reporters on this story: Mark Chediak in San Francisco at mchediak@bloomberg.net;David R. Baker in San Francisco at dbaker116@bloomberg.net;Brian Eckhouse in New York at beckhouse@bloomberg.net

To contact the editors responsible for this story: Lynn Doan at ldoan6@bloomberg.net, Will Wade, Christine Buurma

©2019 Bloomberg L.P.