PG&E's Last Bust Offers Caution for California Bond Investors

PG&E's Last Bust Offers Caution for California Bond Investors

(Bloomberg) -- When PG&E Corp. went bankrupt almost two decades ago, an energy crisis and the dot-com crash were hurling California toward a financial abyss of crippling budget deficits, soaring debts and escalating penalties in the municipal-bond market.

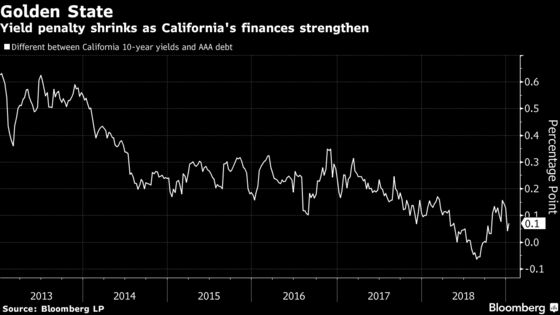

This time, California’s finances are buttressed by a surging economy and record reserves, while officials have shown little interest in bailing out the beleaguered utility, which said Monday it faces $30 billion in liabilities from deadly wildfires. And its plan to file for bankruptcy hasn’t triggered a pullback from state bonds by investors, who are eager to own them as a tax haven.

But the fallout from the company’s 2001 insolvency -- triggered by botched deregulation of electricity markets -- offers investors reasons for caution if the state must step in again to protect its residents. Then, California’s credit rating took a hit and it was forced to sell what was then a record amount of bonds to keep the lights on.

"I don’t anticipate the state at this point making any sort of a financial commitment," said Paul Mansour, head of municipal research at Conning. "But it doesn’t preclude them from being creative in using the state’s stronger credit quality like they did in 2001 in some undetermined form to help keep costs down for California ratepayers."

Governor Gavin Newsom and other state officials say they want to ensure that power service isn’t disrupted; that compensation flows to wildfire victims and ambitious climate-change targets remain on track amid intensifying fire seasons. Those are challenging goals in a state where utility customers already pay among the highest electric rates in the country.

"This is a real huge problem," said Howard Cure, head of municipal research in New York at Evercore Wealth Management. "The state is under enough pressure already to keep businesses in state."

Different Situation

State fire investigators have blamed PG&E’s equipment for starting 17 of the wildfires that tore through Northern California in 2017. The company’s electric lines are also suspected of sparking last year’s Camp Fire, the deadliest in California history, which killed 86 people and destroyed the Butte County town of Paradise.

The situation was markedly different last time around. After lawmakers partially deregulated the power market, wholesale prices, manipulated by companies such as Enron Corp., jumped more than tenfold in 2000 and 2001, and the utilities were barred from passing the cost on by raising rates. Rocked by rolling blackouts, the state agreed to buy power at above-market prices to prop up insolvent utilities and sold $11.2 billion of municipal bonds to finance the contracts.

Related: PG&E Customers Still Paying for Crisis That Led to Its Last Bust

The state suffered several credit-rating downgrades as it grappled not only with the power crisis, but the fallout from the dot-com bust. California’s revenue, which is heavily dependent on the wealthy, is notoriously volatile and vulnerable to market gyrations.

"Those two things together were a big driver of what happened to the state’s credit rating,” said Matt Butler, an analyst at Moody’s Investors Service.

All Options

Now, thanks to an economic boom and financial safeguards such as a voter-mandated rainy-day fund, California’s ratings are at the highest since that era. While its tax revenue is still vulnerable to swings, investors and ratings analysts point to the progress state officials have made in paying off its obligations and boosting its savings.

For now, Newsom says he’s considering all options. The state could decide to own a slimmed-down version of PG&E, said Bloomberg Intelligence analyst Jaimin Patel in a report. He called it a "more viable option" than directly supporting an investor-owned utility.

And California is likely to give PG&E more flexibility to raise customers’ bills, said Jason Ware, head of trading at brokerage 280 CapMarkets. But that’s still a negative for the state’s credit, he said. California’s cost of living is already high, something that was exacerbated by the federal limit on state and local tax deductions enacted last year, Ware said.

"There’s very little wiggle room for California to go out and ask the taxpayer for more money," Ware said.

--With assistance from Claire Ballentine.

To contact the reporters on this story: Romy Varghese in San Francisco at rvarghese8@bloomberg.net;Amanda Albright in New York at aalbright4@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, Michael B. Marois, William Selway

©2019 Bloomberg L.P.