PG&E Isn’t a Powder Keg, Bond Traders

PG&E Isn’t a Powder Keg, Bond Traders

(Bloomberg Opinion) -- It only took a few days for 2019 to produce its first likely fallen angel in the U.S. credit market.

S&P Global Ratings slashed its rating of PG&E Corp. by five notches, bringing it down to B from BBB-. It was a swift and punishing move from S&P, which was the first credit-rating company to take action on news that the California utility is exploring a bankruptcy filing in response to a wave of wildfire liabilities that could be as high as $30 billion. If history is any guide, it’s only a matter of time before Moody’s Investors Service and Fitch Ratings follow, which would banish PG&E to high-yield indexes.

The superdowngrade, in and of itself, does little to address the looming question of “What’s next?” for PG&E, like my Bloomberg Opinion colleague Liam Denning did. As the S&P analysts say in their report, it merely “reflects what we see as the souring political and regulatory environment and our view of the limited options that the company has to effectively manage its operating, financial, and regulatory risks.” They say they could lower the rating even further “if management does not clearly articulate specific steps it will take to preserve credit quality over the long term.” But it’s not their place to offer suggestions.

S&P’s move is more important in that it refocuses the market on the proliferation of U.S. corporate bonds rated in the lowest rungs of investment grade, just a misstep away from falling to junk. This trend has been the bogeyman of traders for much of the past year, which was the worst for investment-grade U.S. corporate bonds since 2008. By Morgan Stanley’s estimate, more than $1 trillion of the debt could be cut to junk when the credit cycle turns.

Fear not, bond traders. PG&E is not the looming fallen angel you’ve been worried about.

The bond market “powder keg” that’s ready to blow requires a bigger spark than PG&E, which has about $18 billion in bonds. While that’s not exactly a small sum, it pales in comparison to corporate behemoths like AT&T Inc. and General Electric Co., which each have more than $100 billion of debt and also have credit ratings in the lowest investment-grade tier. One of the chief concerns about fallen angels is that they will overwhelm high-yield funds once they drop, causing huge losses and forced selling among existing bondholders as the market struggles to adjust.

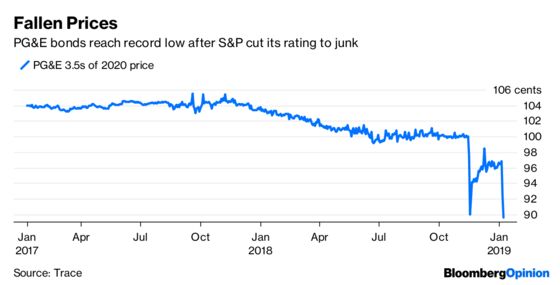

That’s unlikely to happen with PG&E, if for no other reason than the company was already trading like junk before S&P’s downgrade. As Bloomberg News’s James Crombie noted, its bonds have traded at levels consistent with non-investment grade securities since November. PG&E’s 3.5 percent notes due next year recently priced to yield more than 10 percent, well above what most comparable debt is paying.

High-yield investors, for their part, aren’t showing any signs of consternation about the potential new entrant in their market. U.S. junk bonds have already gained 2 percent in the first few days of 2019, easing the sting of the final months of last year. Based on trading in the iShares iBoxx High Yield Corporate Bond exchange-traded fund, it looks like another good day for the debt; the fund, known by ticker HYG, rose to the highest in almost a month.

The rally might just be getting started. JPMorgan Chase & Co. recently raised its forecast for high-yield total returns in 2019 to 8 percent, from 3.3 percent, after the late 2018 sell-off. Even with spreads widening, strategists at the bank said junk bonds were pricing in just a 12 percent chance of a U.S. recession. Given that they predict spreads will narrow by the end of the year, that’s effectively calling for an even lower probability of a downturn. And it also probably means that fallen angels won’t force a reckoning in the speculative-grade debt market.

I said in November that BBB rated borrowers probably wouldn’t bring about a bond-market doomsday because it seemed as if all of Wall Street was anticipating it. It’s the crises that investors choose to ignore that should be more worrisome.

For now, at least, PG&E and its five-level downgrade will capture traders’ attention. The cliff between investment-grade and junk often creates a fleeting opportunity as investors make quick decisions on whether to buy, sell or hold. But it will soon settle into the high-yield market where it belongs as politicians, regulators and company officials begin dealing with the tough questions. As far as the fate of U.S. corporate bonds, PG&E may become a fallen angel, but it will take something much larger to bring the market to its knees.

Technically, Moody's or Fitch or both need to also downgrade PG&E for it to move into high-yield bond indexes. But talk of bankruptcy is usually a good way to get downgraded.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.