Oracle’s Cerner Purchase Prompts a Trio of Debt-Downgrade Warnings

Oracle’s Cerner Purchase Prompts a Trio of Debt-Downgrade Warnings

(Bloomberg) -- Oracle Corp. could see its investment-grade ratings fall to the cusp of junk if it loads up on debt to fund its nearly $30 billion acquisition of medical-records company Cerner Corp.

Following the announcement of the $28.3 billion purchase of Cerner Monday, all three major U.S. ratings graders said they may downgrade Oracle if it increases leverage to carry out the transaction. S&P Global Ratings indicated the software company could be cut by as many as two notches to BBB-, adding that it’s likely to retain its investment-grade rating though some curtailment of share buybacks would probably be required.

At the same time, Fitch Ratings said the agreement “could result in the company deviating from its previous plan to reduce its debt,” as Oracle has repurchased $15 billion of its own shares in the first half of fiscal year 2021. Moody’s Investors Service also placed the company under review, noting that even prior to the acquisition, “Oracle did not have any publicly articulated medium or long-term financial policy goals.”

Read More: Oracle Bonds Drop on $28.3 Billion Cerner Acquisition

If the assessors move forward with the downgrades, they would be doing so after already cutting Oracle’s ratings from the single A tier to BBB earlier this year. S&P lowered the company in June, citing increased leverage and “aggressive” share repurchases. Moody’s and Fitch made similar moves in March.

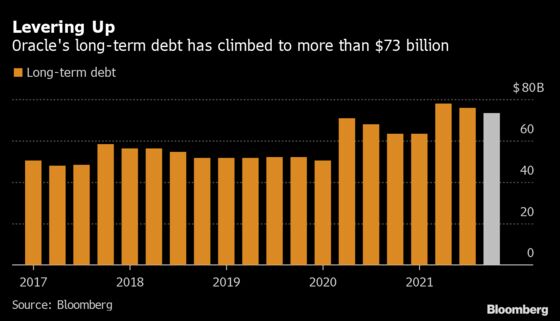

Despite having the second-largest debt load in the tech industry at almost $79 billion, according to Bloomberg estimates, the software provider said it “anticipates retaining an investment-grade credit rating” in the wake of the acquisition. Its long-term debt stands at more than $73 billion, data compiled by Bloomberg show.

But Oracle’s “aggressive use of cash” to fund shareholder returns and acquisitions is pushing the company to the cusp of junk, according to Bloomberg Intelligence analysts Robert Schiffman and Suborna Panja, and that may require the tech giant to make a “dedicated commitment” to decrease debt over the next two years.

“Having likely lost the trust of both bondholder and raters, spreads could continue to leak in the near term, even if required new bond issuance is small,” the analysts wrote on a Tuesday note.

Read More: Citi Says Beware $70 Billion Downgrade Wave in High-Grade Credit

The negative outlook comes amid concerns that many blue-chip companies are likely to boost their borrowings next year until they’re rated just a few steps above junk, a risk the market may not be fully prepared for, according to strategists at Citigroup Inc.

Borrowing costs are still low for companies, even as the Federal Reserve talks about hiking rates three times next year. And the penalty is minimal for being rated in the BBB tier in terms of the extra yield corporations have to pay compared with being rated one tier higher. Spreads on BBB bonds are just 0.41 percentage point wider than those on notes in the A level, according to Bloomberg index data, close to historic lows.

Should Oracle fall to junk, it would become the largest component in the high-yield index, which would shrink its debt investor base, dramatically increase borrowing costs and meaningfully enhance refinancing risk, Schiffman said separately. Its bonds had weakened Monday, and were among the most actively traded today.

“Oracle appears willing to push its total debt load to the brink of high yield, potentially as high as $100 billion, but realizes it can’t fall over that cliff,” Schiffman added.

©2021 Bloomberg L.P.