One Strategy Wins for Yen Traders While Losses Pile Up Elsewhere

One Strategy Wins for Yen Traders While Losses Pile Up Elsewhere

(Bloomberg) -- Yen traders looking for an edge this year would have done well to focus on an obscure technical indicator that can help predict the direction of currencies based on their recent movements.

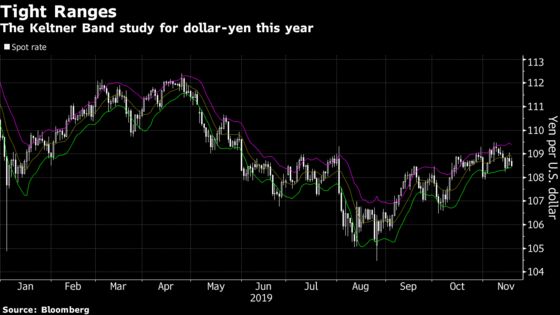

Since the start of the year, the clear winner of the 22 trading strategies featured on Bloomberg’s basic backtesting function has been the KBand, or Keltner Band.

While there are variations, the Keltner Band typically features a center line that reflects the average of recent trading levels, with upper and lower lines that are calculated based on recent highs and lows.

The slope of the band can send trading signals, along with the position of the current price against the lines. The backtest function measures the performance of the KBand by assuming traders go short when the pair closes above the upper band and cover and place longs when prices settle below the lower band.

Using technical studies to trade the yen has been particularly rough this year amid abnormally low volatility -- 16 of the 22 strategies on the basic backtesting function are flashing red.

In other words, there has been a better-than-average chance that a given strategy will have lost money for yen traders. The results are not much better for euro dealers.

Here’s a look at the table for yen strategies, in a year when Japan’s currency has gained about 1% through Tuesday to around 108.54 per dollar:

What’s equally startling is the large discrepancy between the winning and losing strategies.

Using the KBand to trade dollar-yen this year has produced profits that are more than triple that of the second-best strategy, the Rex oscillator -- another scheme that uses intraday price volatility to measure entry and exit points.

The Bollinger Band, one of the money-losing strategies, is similar to the KBand, but uses standard deviations to calculate the upper and lower lines rather than recent price extremes. Another difference is that the KBand tends to outperform when price moves are relatively muted.

The wide profit disparity between closely related strategies shows how one measures volatility can have a pivotal influence on outcomes.

The KBand has proven useful before. This is the second straight year in which the KBand has outperformed when trading the euro and the ICE U.S. Dollar Index. By contrast, the strategy lags on cross-currency and emerging-market bets.

While currency volatility could resurface at any time, the KBand might be worth keeping an eye on until the current calm breaks.

To contact the reporter on this story: Robert Fullem in New York at rfullem5@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Greg Chang, Mark Tannenbaum

©2019 Bloomberg L.P.