Nutanix Analysts Lose Patience After Another Weak Forecast

Nutanix Analysts Lose Patience After Another Weak Forecast

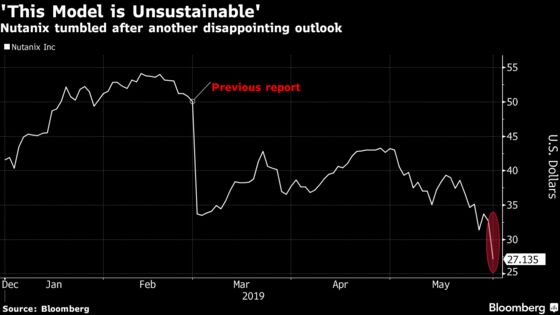

(Bloomberg) -- Nutanix Inc. shares tumbled on Friday after it reported third-quarter revenue that missed expectations and provided a fourth-quarter outlook that fell short of consensus forecasts.

The sell-off follows a similarly sharp drop from earlier this year; the guidance represented the second straight time that the enterprise cloud company disappointed with its outlook. Analysts appeared to be losing patience, as both Morgan Stanley and Stifel put the stock “in the penalty box,” while Piper Jaffray bluntly stated that “it is clear that this model is unsustainable.”

Shares dropped as much as 22% and was on track for its lowest close since November 2017.

Here’s what analysts are saying about the results:

Piper Jaffray, Andrew Nowinski

“It is clear that this model is unsustainable, requiring massive amounts of spending just to support modest revenue growth, which we believe is attributable to competition.”

Downgrades to neutral from overweight, price target cut to $28 from $47.

“The company continues to struggle with execution issues.”

Morgan Stanley, Katy L. Huberty

Missing revenue expectations again “leaves NTNX in the penalty box.” While there’s encouraging growth in the company’s pipeline, the stock should trade “between bear and base cases until investors regain confidence in revenue acceleration.”

Equal weight rating, price target lowered to $35 from $37.

Stifel, Brad Reback

“Chaos still reigns” as both the results and the outlook were disappointing.

“Nutanix remains squarely in the penalty box and we continue to believe it will take several more quarters to evaluate progress.”

Hold rating, price target slashed to $25 from $39.

KeyBanc Capital Markets, Alex Kurtz

“We continue to see a franchise grappling with leadership and model changes but still competing in a growing HCI marketplace.”

“Although challenging to see through all these adjustments, we believe the Company broadly tracked to internal demand targets.”

Overweight rating, price target cut to $40 from $48.

To contact the reporter on this story: Ryan Vlastelica in New York at rvlastelica1@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Will Daley

©2019 Bloomberg L.P.