Nothing Is Certain But Death, Taxes and Muni Bond Advantages

Nothing Is Certain But Death, Taxes and Muni Bond Advantages

(Bloomberg Opinion) -- If the last few days are any indication, the denizens of Wall Street either aren’t as sharp as they seem or they’re dreading the prospect of paying more in taxes. I say this because two of the most popular articles on the Bloomberg terminal this week boiled down to the simple fact that U.S. municipal bonds offer income that’s exempt from federal taxes, and often state and local ones as well.

Consider the first article, “Invesco Money Manager Faces SALT Bite, Turns to This Tax Break.” It chronicles Mark Paris’s dismay that as a New Jersey resident, he’s going to end up paying more in taxes because of the new $10,000 federal cap on state and local tax deductions. So what’s the head of municipal strategies at Invesco going to do about it? Buy more tax-free munis, of course.

Just two days later, Bloomberg readers couldn’t click fast enough on another article, “Your New York Taxes Are Too High? Muni Bonds May Offer an Answer.” In it, Anthony Roth, chief investment officer of Wilmington Trust Investment Advisors, said some people in high-tax states like California, Connecticut, New Jersey, New York and Massachusetts would find that they owe more, which should boost demand for — you guessed it — tax-exempt municipal bonds.

So my question is this: Are people really so unaware of municipal bonds’ obvious tax advantages? I realize my own bias, having covered the $3.8 trillion market for almost five years for Bloomberg News. But any investment adviser would have been remiss to not recommend at least a small allocation to munis as a cornerstone of any portfolio through the years. They’re one of the easiest ways to lower taxable income on both a federal and state level. For those on Wall Street who live in New York City, some bonds are even “triple tax-exempt,” which means avoiding a fairly significant local income levy.

One of my favorite anecdotes about munis comes from Joe Mysak’s “Encyclopedia of Municipal Bonds.” The entry is about the widow of the automotive titan Horace Dodge. Anna Thompson Dodge lived to be 103, and her 1970 obituary in the New York Times features a paragraph that amounts to a sales pitch for municipal bonds:

“Horace Dodge died in December, 1920, a year after John. The $594 million Mrs. Dodge inherited was put into tax‐free municipal bonds. The money was said to have earned on the average of $1.5 million a year, and Mrs. Dodge never had to pay a Federal income tax.”

It’s almost too perfect that Mrs. Dodge came to embody a way to dodge taxes. Of course, there’s a reason municipal-bond interest is tax-exempt — the proceeds are often used to build or repair roads, bridges, railways, airports, water systems and schools. In other words, it’s an incentive to finance public works. But it’s not just a boon to investors, because states and cities can usually lock in lower borrowing costs than they would otherwise.

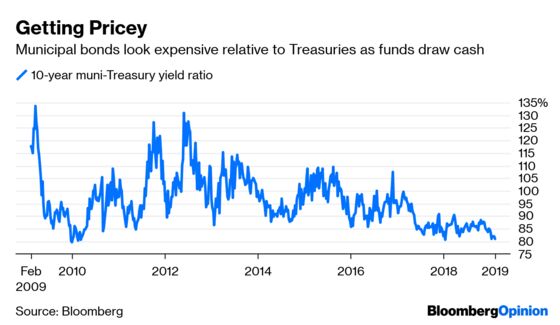

In fact, it’s rarely been cheaper for state and local governments to issue debt (and expensive for buyers), relative to the prevailing level of U.S. Treasuries. A top-rated 10-year municipal bond currently yields 2.18 percent, whereas the benchmark 10-year Treasury note yields 2.7 percent. That amounts to a so-called muni-Treasury ratio of 81 percent. In Bloomberg data going back almost two decades, the lowest ratio ever was 78 percent in June 2007. Even at that level, the taxable equivalent yield on munis is better than Treasuries and even high-rated corporate bonds.

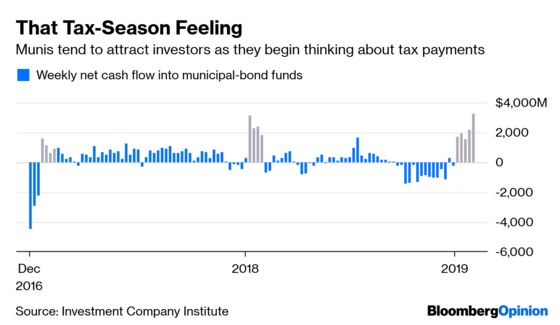

To be fair, recent data suggest investors aren’t entirely oblivious to the tax advantage of owning munis. Funds focused on state and local government debt drew $3.3 billion of cash in the week through Feb. 6, the largest weekly inflow since at least 2007, according to Investment Company Institute data. On Feb. 7, President Donald Trump said he’d consider changes to the SALT cap, though Senate Finance Committee Chairman Charles Grassley shot down the idea through a spokesman. Needless to say, there was rampant interest in that potential change.

Tax season traditionally buoys munis, for the obvious reason: People are thinking about how much they’re paying, and it reminds them they should probably try to structure their finances in the most advantageous way. For at least a brief time, the often-neglected corner of the larger fixed-income universe has its moment. Maybe that’s behind this latest rush to read up on the municipal market, too.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.