Nothing Is Certain But Bailouts: How Stimulus Works in a Vacuum

Nothing Is Certain But Bailouts: How Stimulus Works in a Vacuum

(Bloomberg) --

Here’s what investors don’t know: How many people will lose their jobs. How far profits will fall. How deep the recession will be. The only thing they’re sure of is that the government has pumped $4 trillion into the economy and is hell-bent on seeing it work.

A world of total uncertainty, and one observable fact. Is it any wonder what markets are clinging to?

The deluge of stimulus has pushed the S&P 500 to a 27% rally since mid-March, a stretch that halved its bear-market plunge by way of the fastest 15-day rally in eight decades. There’s more to come -- Congress is negotiating an additional $250 billion for small businesses, while Federal Reserve chairman Jerome Powell has vowed the central bank will never “run out of ammunition.”

Heading into one of the murkiest earnings season on record, bulls and bears are getting a lesson in how risk works in a vacuum. When the choice is between unknowable pain and a promise that nothing will be spared to contain it, you act on the latter -- particularly after a decade in which every bet against government rescues ended in disaster.

The implicit promise of further stimulus is buoying stocks even as evidence of the pandemic’s economic impact piles up. U.S. retail sales dropped the most on record in March as millions of workers lost their job, with more than 5 million Americans filing for unemployment benefits last week. The grim figures only briefly rattled traders -- after initially wavering, stocks resumed their rally Thursday and capped a second straight weekly gain.

“There is no playbook. That’s why there’s uncertainty, and you can’t focus on ‘Look at all those people out of work,”’ said Kim Forrest, chief investment officer of Bokeh Capital Partners. “The biggest thing that has stopped the market from falling is the Fed’s intervention and their multi-asset way of doing this. That’s powerful and unnerving all at the same time.”

Investors have been conditioned for success -- for better or worse. While the market’s buoyancy strikes many observers as inexplicable, recent history has examples of all-or-nothing propositions being resolved in bulls’ favor. First among them is the financial crisis. While a handful of short sellers got rich and famous riding the S&P 500’s plunge through the March 2009 bottom, more money was made on the way back up -- a trade that involved going all-in on the Fed at a time unemployment was at a 50-year high.

With the slowing pace of new infections and death, the sheer magnitude of the policy response is responsible for a “big chunk” of the rebound, according to QMA’s Ed Keon. That’s helping steady markets as companies begin to report profits for the first quarter, with analyst predictions rendered effectively useless in the wake of the virus’s abrupt onslaught.

“Earnings are going to be terrible, guidance is going to be terrible. It’s the further change in policy that’s going to be more useful as a market guide than earnings right now,” said Keon, QMA’s chief investment strategist. “My guess is the market already knows it’s going to get the maximum possible policy response.”

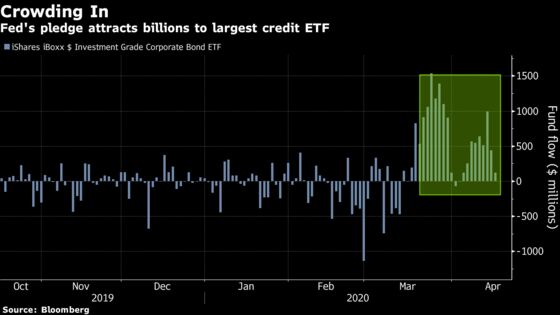

Among the unprecedented measures taken by the Fed is a corporate bond-buying program that allows it to purchase of up to 10% of an issuer’s outstanding bonds and up to 20% of the assets of eligible exchange-traded funds. The program was expanded last week to include debt from companies that recently lost investment-grade status in an effort to keep credit flowing. All told, the facility is expected to support as much as $850 billion in credit.

Backstops in the bond market have reignited debates about moral hazard -- the idea that policy makers are encouraging risky behavior by shielding investors from losses they deserve to take. It was a frequent criticism lobbed at the Fed during the last financial crisis, when the central bank unleashed quantitative easing for the first time.

“From a price discovery and market functioning perspective, we will come out with more zombie firms that should have died in this shock,” said Ed Al-Hussainy, a senior strategist at Columbia Threadneedle. “And finally from an investor perspective, active managers who would have been taken to the woodshed will remain in business.”

Measures of credit risk have eased dramatically following the Fed’s announcement, after solvency fears spiked in mid-March. Junk bond spreads to Treasuries have narrowed to 740 basis points as of Wednesday, according to the Bloomberg Barclays U.S. Corporate High-Yield index. Spreads had reached 1,100 basis points on March 23, the widest level since the 2008 global financial crisis.

Like with most things related to the virus, there’s little precedent for the federal government’s response, which has unleashed over $2 trillion in aid so far. President Donald Trump, who has staked much of his reelection bid on the economy, has said he’s determined to do whatever needed for the country to claw back economically.

Of course, it’s hard to argue that the government or the Fed shouldn’t be pumping up the economy in the face of a devastating human disaster that’s infected more than 2 million people globally. Nevertheless, the effects of the stimulus -- and the implicit guarantee that global central banks stand ready to intervene in such a manner -- will distort asset pricing for years to come, according to Cantor Fitzgerald.

“No one wants to make the case that the Fed should not be bailing us out of a pandemic,” said Peter Cecchini, Cantor’s chief market strategist. “The downside is those policies never end. Risk no longer prices, and we no longer have a capitalist democracy left.”

To Michael Purves at Tallbacken Capital Advisors, the Fed’s decision to purchase high-yield debt in particular will leave a lasting memory in markets. The magnitude of stimulus delivered in such a short amount of time is the driving force behind the rally -- and unlike 2008, investors have been “trained” how to process quantitative easing, he said.

“The signaling there, that will have muscle memory that will go on for a long time,” said Purves, Tallbacken’s chief executive officer. “We are well-trained and the machines are well-trained to know how to process this, and the Fed has given us 150 basis point cuts in three weeks and an enormous expansion in the balance sheet in a very short period of time.”

©2020 Bloomberg L.P.