Note to Powell: Four Big Questions From Bond Markets This Week

Note to Powell: Four Big Questions From Bond Markets This Week

(Bloomberg) -- Bond investors know not to expect more dramatic action from Wednesday’s Federal Reserve policy decision -- the past six weeks of emergency relief measures worth trillions of dollars are still coursing through markets.

But this meeting, Morgan Stanley strategists have warned, is “more important than you think.” There are several points on which traders will be seeking clarity, either from the Fed’s statement or from Chairman Jerome Powell at his news conference.

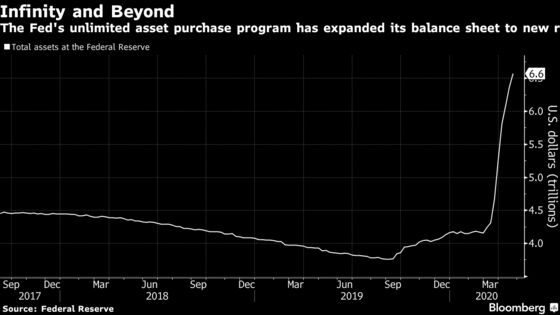

They’ll want guidance on the pace of bond purchases, since the Fed cut its target to zero in mid-March and embarked on an open-ended asset-purchase program that has added more than $1.4 trillion of Treasuries and $570 billion of mortgage debt to its balance sheet. There will also be plenty of interest in whether policy makers are preparing to anchor government borrowing costs in a return to the yield-curve control policy employed during World War II.

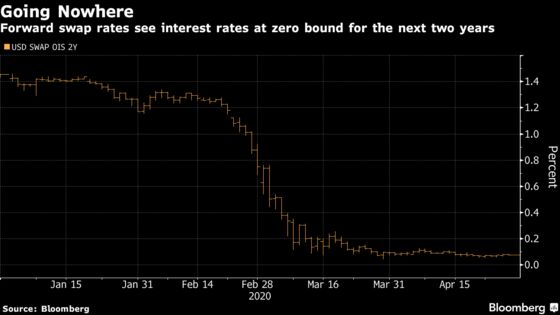

While former Minneapolis Fed President Narayana Kocherlakota’s notion that it’s time for negative rates hasn’t gained traction, it may be a topic of questioning for Powell. The only likely policy move -- at least by some accounts -- is that the Fed may adjust its interest-rate floor to help keep market rates from slipping below zero.

Here’s a rundown of some key points bond traders are waiting to hear more on, in addition to officials’ latest assessment of the economic damage from the pandemic and updates on municipal and corporate-bond programs yet to launch:

Forward Guidance

- This is particularly key with respect to asset purchases. Initially, Treasury purchases were capped at $500 billion of Treasuries and $200 billion of mortgages. A week later, as markets continued to reel, the caps were removed. At its peak the program was targeting $75 billion of Treasuries a day; this week, the Fed is buying an average of $10 billion a day. The daily averages have been announced weekly, and the general consensus of strategists is that now is the time to shift to a monthly targeted amount. Bank of America and Morgan Stanley envision $150 billion a month; Barclays says $75 billion a month could suffice.

IOER Debate

- Because the federal funds rate -- for which the FOMC set a target range of 0% to 0.25% in March -- has averaged 0.04% twice in the past week, market strategists anticipate it may tinker with the rates it uses to enforce the fed funds range. Officials have done that in the past when the effective fed funds rate came within 5 basis points of the bottom of the range. The Fed’s asset purchase and liquidity programs are putting downward pressure on the fed funds rate that the central bank can counter by raising the reverse repo (RRP) rate that acts as a floor (from 0%) and the interest on excess reserves (IOER) rate that acts as a cap (now 0.10%), Barclays strategist Joseph Abate said last week. Barclays and Bank of America expect both to be increased by 5 basis points, with BofA favoring a 10-basis-point IOER increase. But there’s disagreement, and Deutsche Bank says an IOER increase could counterproductively tighten pricing for some of the Fed’s credit facilities.

Commercial Paper

- Credit facilities may also come up at the meeting. Strategists at Bank of America and TD Securities have been looking for Fed to lower rates on its money markets and commercial paper programs to encourage more participation and further declines in Libor, the benchmark interbank borrowing rate. NatWest doesn’t consider that likely, given that three-month Libor has been on a steady downward trend this month.

Curve Control

- Finally, strategists are discussing the prospect that the Fed later this year will adopt curve control -- targeting Treasury yields at specific levels to prevent the government’s borrowing costs from getting out of hand as it unleashes relief packages worth trillions of dollars. Yield-curve control has been Japan’s policy for several years, and Australia’s central bank officially pinned its three-year rate last month. Vanguard portfolio manager Gemma Wright-Casparius expects that the Fed may soon start laying the groundwork for its own version. “By June when we start to get their economic forecasts, we’re looking for liquidity support to shift to policy support and purchases may change again,” she said.

©2020 Bloomberg L.P.