There Are No Bad Leveraged Loans, Just Bad Prices

There Are No Bad Leveraged Loans, Just Bad Prices

(Bloomberg Opinion) -- Nothing gets the hyperbole going in financial markets quite like a violent sell-off, especially in an asset class that some consider doomed to fail.

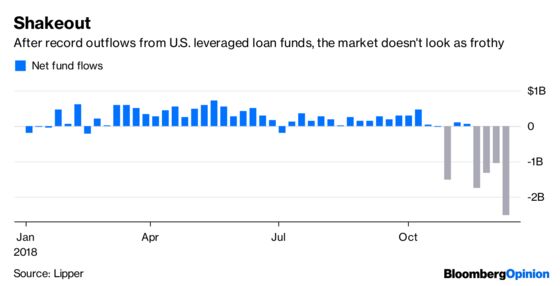

The $1.3 trillion U.S. leveraged-loan market, which has drawn scrutiny from Senator Elizabeth Warren of Massachusetts, former Federal Reserve Chair Janet Yellen and BlackRock Inc., among others, is in a protracted slump. It has declined for five consecutive weeks, with investors yanking an unprecedented $2.53 billion from loan funds in the week through Dec. 12, according to Lipper data. Those sorts of withdrawals have investors like Gershon Distenfeld of AllianceBernstein LP feeling nervous. “Having outflows that are 2 to 3 percent of the market is scary. What happens if we get 10 or 15 percent?” he asked last week on Bloomberg TV.

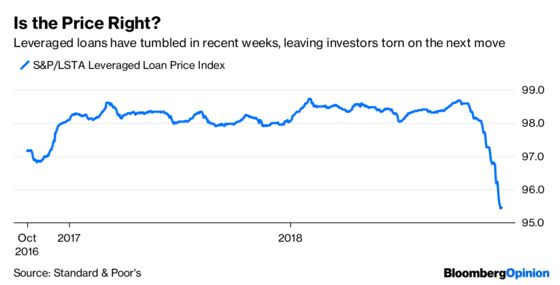

I’ll tell you what would happen in that extreme scenario: Prices would keep dropping. As it stands now, they’re at the lowest since October 2016, according to S&P/LSTA Leveraged Loan Index data. This is showing up in the new issue market, too. Bloomberg News’s Lara Wieczezynski reported that the following companies have either had to offer steeper discounts to par, or wider spreads, in just the past week: Cambium Learning Group Inc., Equitrans Midstream Corp., Jostens Inc., KDC US Holdings Inc., Plaskolite LLC, and Tecta America Corp. It looks as if Callaway Golf Co., Western Dental Services Inc. and Par Pacific Holdings Inc. will do the same.

In the face of all the doom and gloom, these deals are still getting done. This should signal that the hyperventilating about vanishing liquidity and mutual-fund blowups is unnecessary. It brings to mind one of my favorite adages about the fixed-income markets: “There’s no such thing as a bad bond, just a bad price.” It’s a shorthand way of saying leveraged loans aren’t inherently poor investments — they’re only bad when investors aren’t properly compensated for the risks. That was largely the case for most of 2018. In a way, leveraged loans are less scary now than they’ve been in quite some time because borrowers can’t get away with high prices, tight spreads and weak creditor protections.

Of course, prices aren’t everything, and it’s true that some larger trends are working against the market. For one, the Fed looks increasingly likely to take a pause — and an extended one, if markets are to be believed — from raising interest rates after this week, reducing the appeal of floating-rate loans. On top of that (or perhaps because of it), sales of collateralized loan obligations fell 25 percent in the first half of December from the same period last year after declining 10 percent in November. CLOs are a valuable source of demand for leveraged loans specifically because they don’t become forced sellers to meet redemptions.

“Things are on pause right now,” Lauren Basmadjian, portfolio manager at Octagon Credit Investors, told Bloomberg’s Lisa Lee. “No one wants to catch a falling knife.” Indeed, in August 2011 and December 2015, the two other times in recent history that loan funds saw a weekly exodus of more than $2 billion, prices dropped even further.

On Dec. 3, when the average price of leveraged loans was 96.8 cents on the dollar, I wrote that the market was taking a much-needed breather. At 95.2 cents, it’s hard not to feel the same way. Regardless of whether the market is at the bottom or still has room to fall, a smattering of interviews from the end of last week suggests investors want to come back.

The sell-off creates “an interesting dollar-cost average opportunity,” Frank Ossino, senior managing director and portfolio manager at Newfleet Asset Management, told Bloomberg News. “This correction should bring back some much needed discipline to the market,” said John Sherman, a portfolio manager at DDJ Capital. Brit Stickney, a portfolio manager on Allianz Global Investors’s income and growth fund team, was more direct. “This is a buying opportunity,” he said. “When I look at the fundamental backdrop, I think leveraged loans are oversold” relative to high-yield debt.

It’s not as if junk bonds have had a great run in the past few months, either. The Bloomberg Barclays U.S. Corporate High Yield Bond Index is flat for the year after being a star performer in the first three quarters of 2018. Yet it bounced from recent lows, even in the face of $2.1 billion of fund outflows in the most recent period. It helps that no new issues have priced so far in December, but as feeble as markets have seemed lately, few are calling for an uptick in defaults or steep declines in corporate earnings. That’s keeping investors interested in high-yield securities. At some point, the tide should turn for leveraged loans, too.

For those investors who think the credit cycle is about to take a turn for the worse, current spreads might still be too tight. Perhaps that’s fair, given expectations that recovery rates will dip in the next downturn relative to 2008. But that doesn’t make leveraged loans an outright bad investment, nor does it mean loan funds are in for a liquidity crunch. This is a hot market that cooled off in a hurry and is searching for a more reasonable temperature.

From Oct. 7 to Oct. 8 that year, the index price spiked, rising from 95.31 cents on the dollar to 96.85 cents. It was reported at the time that the sharp increase was due to the removal of some TCEH Corp. loans after the company emerged from bankruptcy.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.