New ECB Benchmark Draws Scrutiny After Data Blip

New ECB Benchmark Draws Scrutiny After Data Blip

(Bloomberg) -- Just as money-market traders were getting comfortable with the European Central Bank’s new benchmark short-term interest rate, an unexplained blip in the data behind the measure this week gave reason for pause.

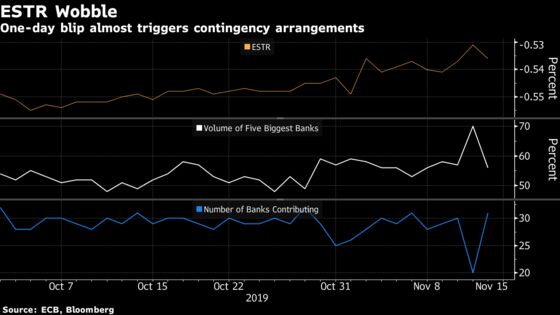

The euro short-term rate for Nov. 13 jumped to -0.531%, figures released Thursday showed, the highest ESTR reading since the ECB began publishing daily reports at the start of October.

Accompanying details showed a slump in the transactions and volume used to calculate the rate. The number of banks contributing to the reading fell to 20, the minimum number required to avoid triggering a contingency procedure, and the five biggest banks were responsible for 70% of the volume used to produce ESTR that day, up from 57% the day before.

While figures released Friday showed those measures returning toward their average, and the rate subsiding, the anomaly may cast doubt on the reliability of the benchmark, which is being introduced to facilitate a move away from Libor-like rates. A spokesman for the ECB declined to comment when asked about the data.

One possible explanation for the wobble is the ECB’s introduction of a tiering system that shields a certain amount of lenders’ cash from its negative deposit rate, strategists at European banks said. While ESTR barely flinched when tiering kicked in, prompting some market watchers to praise the central bank, deposit flows moving around the financial system have the potential to cause ripples and ease downward pressure on rates.

“It is still early days, but the increase in the ESTR fixing alongside the drop in volume and faltering equities need to be monitored closely to assess whether the new fixing remains stable under tiering,” Commerzbank AG strategists Christoph Rieger and Cem Keltek wrote in a note to clients.

Had the number of reporting banks dropped below 20, or the volume from the five most active banks topped 75%, contingency arrangements would have kicked in, according to a methodology on the ECB’s website.

The central bank is able to correct the data if errors are detected and also has a data quality management process, with checks carried out and periodic reviews.

ESTR isn’t the only new benchmark to come under scrutiny as central banks push for a move away from Libor. In the U.S., recent funding-market turbulence has also spurred questions about the viability of the Secured Overnight Financing Rate.

The shift comes after a rigging scandal with the London interbank offered rate undermined confidence in indexes used as benchmarks for roughly $370 trillion of financial products worldwide.

| Read More: |

|---|

|

--With assistance from James Hirai, John Ainger and Paul Gordon.

To contact the reporter on this story: Paul Dobson in London at pdobson2@bloomberg.net

To contact the editors responsible for this story: Jenny Paris at jparis20@bloomberg.net, William Shaw

©2019 Bloomberg L.P.