Neuberger Berman Just Rode the Stock Swoon by Selling Volatility

Neuberger Berman Just Rode the Stock Swoon by Selling Volatility

(Bloomberg) -- Trillions got wiped out, volatility surged and investors ran to havens. Yet a racy bet on market serenity bested mainstream stocks in the market swoon.

The options-selling strategy, now a multi-billion dollar juggernaut, was one way Wall Street warded off steep losses this month.

Just ask Erik Knutzen. The CIO of multi-asset strategies at Neuberger Berman shorted volatility by selling put options in the run-up to the May mayhem. Assailed by critics for being short-sighted, the trade keeps getting vindicated by relentless hedging demand that delivers steady income.

The Neuberger Berman investor is still riding the volatility wave while eyeing up beaten stocks on the cheap.

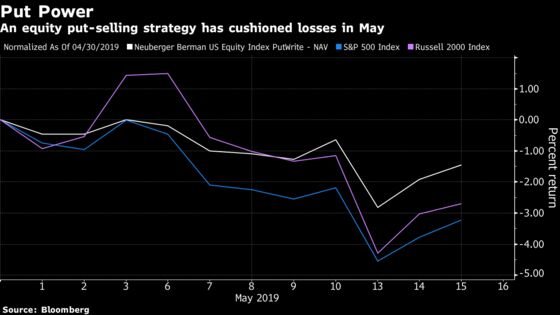

A $280 million Neuberger fund that specializes in writing equity-index puts was down 1.91% this month as of May 14 compared with a 3.58% loss for a mix of S&P 500 and Russell 2000 indexes. That’s even as the Cboe Volatility Index, or VIX, climbed as high as 23 last week, before easing in recent sessions in tandem with the equity recovery.

“We continue to pursue the strategy and are taking advantage of the elevated VIX to capture higher premiums,” said Knutzen, who’s also co-chair of the asset allocation committee at the $323 billion asset manager.

He’s in good company. Real money and hedge funds have heeded Wall Street advice to systematically sell insurance against price swings as a way of getting exposure to the bull market.

Such derivative plays are complementing vanilla equity wagers thanks to technical factors in the underbelly of the derivatives market that give the trade juice.

For Knutzen, loading up on equity-index puts in his multi-strategy funds was a way to offset frothy stock valuations earlier in the year.

“We went neutral U.S. equities, we took risk down to more moderate exposures because we were expecting increasing volatility around inflation and slowing growth in Europe, China and Japan,” he said. “We re-positioned some of our directional equity risk towards equity index-put options.”

Booming Trade

One reason such strategies have been taken up by pension funds and big money managers en masse is the allure of equity-like returns with fewer swings. Research from Neuberger shows a put-writing strategy carries around two-thirds of the volatility of the S&P 500 -- though it will trail the index in a strong bull market.

The Neuberger fund writes protective options on the S&P 500 and Russell 2000 indexes that allow the holder to sell these gauges at a fixed strike price.

For that insurance-like contract, hedgers have been willing to pay an average of 1.5% a month over the past 30 years, or 18% per year, according to the research. The fund collects this premium, along with income from collateral it posts.

While this month’s rout has put the fund on the hook for losses, paradoxically the higher VIX also means it can collect more from selling contracts, cushioning the blow.

Still, for a so-called conservative income strategy, the drawdowns can be severe, such as the 10% loss it suffered in the fourth quarter of 2018 -- though it was less than the S&P’s 14% swoon.

‘Gamma Trap’

The strategy isn’t without its critics. While estimates are hard to come by, the amount of institutional put-selling is anecdotally vast enough to push down implied volatility in U.S. stocks, potentially creating an illusion of market serenity. And should stocks drop dramatically, dealer hedging may exacerbate losses, a phenomenon dubbed a gamma trap.

As for Knutzen right now, he’s mulling whether to add to equity longs, depending on how tensions in global commerce play out.

“We need to see if this trade concern plays through to consumer confidence, CEO confidence, whether the dollar appreciates significantly which would be a further risk-off indicator -- and would be an indication that this is a fundamental shift rather than something episodic,” the investor said.

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.