Netflix Analysts See Regained Mojo After Rocky Start to 2021

Netflix Analysts See Regained Mojo After Rocky Start to 2021

(Bloomberg) -- Netflix Inc. started out the second quarter on the front foot, posting its best gain in three weeks as Wall Street sees the stock as poised for a turnaround.

The streaming giant had a lackluster start to the year with its first quarterly decline since September 2019. But analysts are increasingly bullish on Netflix’s dominant market position and improved finances that give it room to resume buybacks and avoid taking on more debt. Such fundamentals are seen lifting the shares even as streaming competition is stronger than ever.

Piper Sandler assumed coverage on the stock Thursday with an overweight rating, writing that its consistent subscriber gains, modest price increases, and original content all create an opportunity for long-term gains.

Such advantages are seen as supporting the stock despite competition from new services like Discovery+ or ViacomCBS’s Paramount+, as well as the rapid growth at Disney+.

Piper is not alone in its optimism. Of the firms tracked by Bloomberg, more than 70% have a bullish view on Netflix, compared to 11% with a negative rating. The average price target points to upside of about 13% from current levels, and its consensus rating -- a proxy for its ratio of buy, hold, and sell ratings -- is 4.20 out of five.

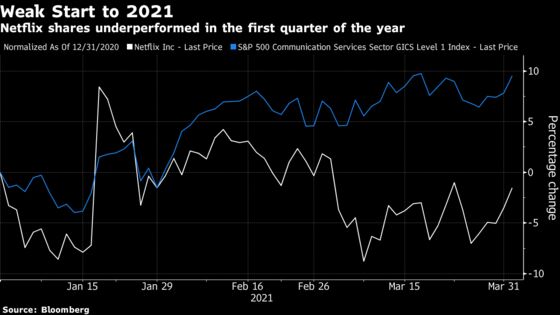

The stock rose 3.4% on Thursday, its biggest gain since March 11. Netflix shares fell 3.5% over the first quarter, underperforming the 7.8% advance in the S&P 500 Communication Services Sector.

Exceeding the 200 million mark and accounting for more than 45% of the market share for streaming subscribers, Netflix’s user base is seen as a singular advantage that can withstand competition.

Earlier this week, Lightshed Partners analyst Richard Greenfield wrote that the debuts of new services have been met with failed predictions that competition would “kill” Netflix. In reality, “as each service has launched, it has accelerated the consumer transition from linear TV to streaming TV rather than cannibalizing each other,” he said.

As streaming has grown, Netflix remains synonymous with on-demand entertainment, to the point that new services like Paramount+ “will be fighting to be the fourth, fifth or sixth streaming service” people use, according to Loop Capital Markets, which prefers Netflix over its competitors.

Password Crackdown

That Netflix viewers won’t jump ship to a rival is a key assumption as the company takes steps to crack down on password sharing among accounts. While there are concerns this could result in elevated “churn” -- users canceling subscriptions -- that risk is seen as offset by the revenue growth that would come if non-paying viewers sign up.

Citi calculated that password sharing costs U.S. companies about $25 billion a year, and that Netflix accounts for about 25% of that lost revenue. Bloomberg Intelligence recently estimated that reducing password sharing could increase Netflix’s revenue by 10%.

Netflix is scheduled to report first-quarter results on April 20, and Wall Street expects revenue of $7.13 billion, which would represent year-over-year growth of nearly 24%.

“There are several reasons we’re enthusiastic about the stock, and it has a lot of levers it can pull for long-term growth,” Matthew Thornton, an analyst at Truist Securities, said in an interview. “I don’t make too much of the underperformance, except to say that it makes the stock look even more compelling.”

©2021 Bloomberg L.P.