Negative-Yield World Lures Central Bankers to Canada Muni Market

Negative-Yield World Lures Central Bankers to Canada Muni Market

(Bloomberg) -- From a suburban office in Victoria, British Columbia, Peter Urbanc finds himself spending more and more time fielding calls from reserve managers and institutional investors halfway around the world.

That’s because as head of the Canadian province’s Municipal Finance Authority, he’s got something they desperately want: AAA rated bonds that actually pay those who hold them.

In May the authority, which provides funding to more than 200 local governments, agencies and hospitals, sold C$800 million ($606 million) of five-year notes to yield 2.18%, about 54 basis points more than Canadian government debt. About 36% went to international investors, including three central banks in Eastern Europe, the Middle East and Africa, as well as an official institution in Asia. That’s up from 26% and 14% in two previous similar-maturity deals.

The fact that foreign money managers are delving into Canadian municipal bonds -- which account for just 1% of trading in the country’s C$2 trillion public sector fixed-income market -- is a testament to how hungry they’ve become for high quality, higher-paying assets in a world where at least $13.8 trillion of debt is now in negative-yield territory. Throw in the fact Canada has given little indication it will follow the global move toward easier monetary policy, and the market is fast becoming a magnet for sophisticated investors seeking to boost returns.

“If you’re sitting in the Middle East, Asia or Europe and you’ve got all this negative yielding debt, it makes a lot of sense to look for the hidden gems such as these excellent quality municipals,” said Avi Hooper, a portfolio manager at Invesco, which has $1.2 trillion under management, including bonds issued by the city of Montreal. “One has always to be careful with the liquidity of course. Big institutional investors are not going to get involved with $50 million deals.”

The Municipal Finance Authority of British Columbia’s C$725 million of 3.05% notes due in 2028 have returned about 6.6% over the past six months, outpacing the 5.6% advance of the Bloomberg Barclays Canada Aggregate corporate index over the span.

A second quarter economic recovery along with a central bank that’s standing pat even as the Federal Reserve and European Central Bank turn dovish has made the loonie the best performing group-of-10 currency this year, further boosting gains for international investors.

Urbanc says offshore money managers who own federal government debt and provincial bonds -- both highly liquid markets -- are increasingly lured to munis for the spread pickup.

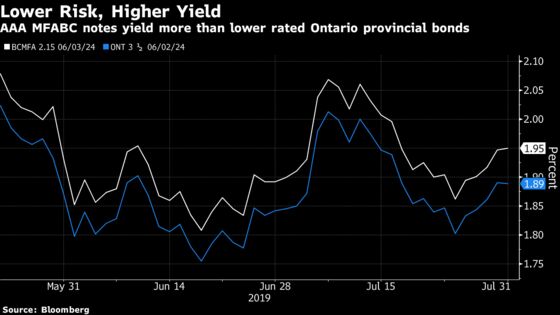

MFABC’s June offering priced to yield about 5 basis points over similar-duration Ontario government notes, despite the fact that the authority’s AAA rating is three steps above that of Canada’s largest province.

Municipalities can have higher ratings than provinces, even the ones in which they reside, because responsibilities and revenues tend to be sufficiently distinct so that credit pressures don’t necessarily transfer, according to Michael Yake, a Toronto-based analyst at Moody’s Investors Service. Municipalities are more dependent on stable revenue sources like property taxes, and those rated above their provinces typically have strong reserve levels and a track record of managing operating pressures.

“You can see it in our spreads, as well as general municipal spreads getting tighter versus provincial spreads, Urbanc said.”

While it’s one of the most liquid issuers in the C$60 billion-plus Canadian municipal market, MFABC is far from the only one benefiting from rising international-investor demand.

Non-residents accounted for about 11% of trading in the market over the first half of the year, compared with about 9% a year earlier, according to a National Bank of Canada report based on data from the Investment Industry Regulatory Organization of Canada. Unlike the U.S. market for local government debt, Canadian securities don’t offer the same attractive tax advantages to domestic buyers, which tend to depress nominal yields stateside.

Toronto and Montreal, the country’s two largest cities, are among other municipal issuers with benchmark-size deals of more than C$500 million outstanding.

Foreign participation in the Canadian muni market will continue to grow as central banks get increasingly familiar with the paper, according to Urbanc.

“Two years ago I went to a Latin American central bank conference in Panama and I didn’t find any Latin American central bank which bought our name,” he said. “Now we’re in dialog with two or three that are taking a bet in municipal names.”

To contact the reporters on this story: Esteban Duarte in Toronto at eduarterubia@bloomberg.net;Paula Sambo in Toronto at psambo@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Boris Korby, David Scanlan

©2019 Bloomberg L.P.