Bets on World of Negative Interest Rates End With Capitulation

Bets on World of Negative Interest Rates End With Capitulation

(Bloomberg) -- At the height of the pandemic, it seemed only a matter of time before negative interest rates -- the last resort of central banks -- ruled global markets.

A controversial strategy that’s yielded mixed results in the euro-area and Japan, traders still piled on bets earlier this year that central banks from New Zealand to the U.K., and even the U.S., were destined to follow suit. The three were among those that most aggressively cut rates through the worst of the virus-induced lockdowns. Yet all ultimately stopped short of going negative.

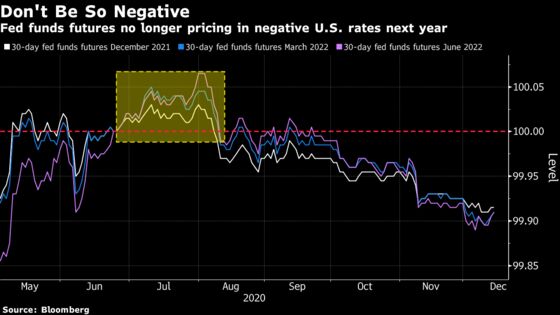

Traders now see a sub-zero move as increasingly unlikely, with policy makers largely favoring a “new conventional” mix of bond purchases and sector-specific aid programs. Of course, trillions of dollars of debt continue to trade with negative yields, effectively guaranteeing a loss for those who hold them to maturity. But with optimism returning about global growth, bond investors are shifting their attention to bets that yields will go higher, not lower.

“Central banks who don’t already have negative interest rates are going to be very cautious about crossing that rubicon,” said James Ashley, head of international market strategy at Goldman Sachs Asset Management. If policy makers need to prop up growth, “would it not be more prudent simply to rely on the unconventional tools like large scale asset purchases.”

Bold Experiment

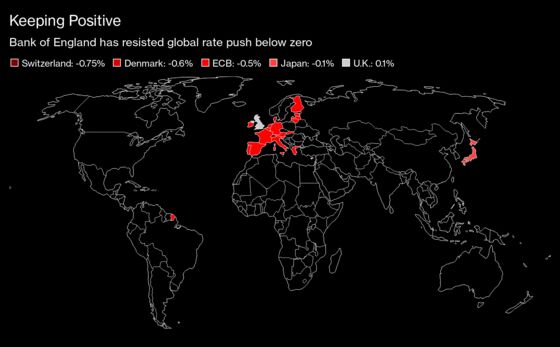

Considered one of the boldest monetary experiments of the 21st century, negative rates were adopted in the wake of the financial crisis to drive borrowing costs lower and penalize banks that hoard cash rather than lending it out. The consequences for bond markets were far-reaching and long-lasting as trading was stymied and yields tumbled. The world’s stockpile of negative-yielding debt climbed above $18 trillion this month, a record, with rates on Spanish 10-year bonds sliding below 0% for the first time.

But despite the sub-zero strategy, both Europe and Japan have seen muted growth and failed to boost inflation to central banks’ targets. In fact, negative rates may have eaten into bank profits and hurt savers. As Federal Reserve Chairman Jerome Powell put it in May, “the evidence on negative rates is mixed.”

“The Fed has investigated a lot of BOJ and ECB policies,” said Kenta Inoue, senior market economist at Mitsubishi UFJ Morgan Stanley Securities in Tokyo. “At this point in time, there is no evidence suggesting that negative rates policy has a positive impact on the economy as well as markets.”

In a way, the holdout central bankers were saved from having to make the decision to go negative by both the success of alternative policies and an improvement in the global economic backdrop. The flood of liquidity to the financial system -- spearheaded by the Fed -- pushed borrowing costs lower, and rapid progress on vaccine development brought forward expectations of a return to normal.

Positive Shift

In money markets, traders have erased bets on negative rates next year in both the U.S. and New Zealand. And while their U.K. counterparts still expect rate cuts to combat the economic blow dealt by the coronavirus and Brexit, the Bank of England is seen stopping at zero.

Read More: BOE Ready to Act If Brexit Talks Fail to Deliver a Deal

Indeed, higher bond yields are now seen in the U.S. and New Zealand, with some strategists from Bank of America to Societe Generale looking for 10-year Treasuries to advance toward 1.5% by the end of 2021.

The vocal pushback from U.S. policy makers on the likelihood of negative rates and economic optimism have seen investors switch to bets on a steeper yield curve, albeit with limits. The benchmark Treasury yield has about tripled from its March low to 0.90% Tuesday.

“Since the Federal Reserve has signaled that it would not cut interest rates below zero, Treasuries have a floor at 0%,” said Saxo Bank strategist Althea Spinozzi. “2021 is going to be all about a yield-curve steepener.”

New Zealand Story

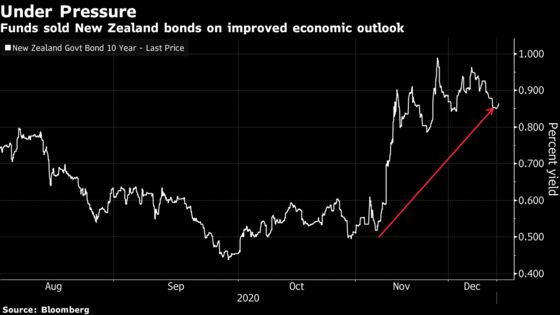

The situation is similar in New Zealand. China’s economic rebound, the Reserve Bank of New Zealand’s more favorable outlook on the economy and a new lending program have slashed expectations for even one more rate move in Wellington, let alone a reduction below zero. The RBNZ has a record-low rate of 0.25%.

Swap markets are pricing just a 30% chance of a 25 basis point cut by the end of 2021, after pricing in almost 50 basis points of cuts in November. And the 10-year government bond yield was trading around 0.87% on Tuesday, about double the September low of 0.44%.

“The hurdle for doing negative rates is going to be very high,” said Bank of New Zealand strategist Nick Smyth. New Zealand bonds are losing their premium to peers and there’s the potential for 10-year yields to climb to 1.5% if Treasuries retreat, he added.

Brexit Blues

Still, the risk of a no-deal Brexit could revive bets on negative rates in the U.K. Although the BOE is currently seen lowering rates by 10 basis points in early 2022, pricing has see-sawed with Brexit headlines, with traders betting on a cut as soon as May last week.

The move comes after Monetary Policy Committee member Michael Saunders flagged room for more cuts, and colleague Silvana Tenreyro said evidence is “supportive” of a sub-zero rates policy.

“We see the BOE taking the bank rate negative next year,” said Peter Schaffrik, a global strategist at RBC Europe Ltd. “Even a Brexit deal is a huge disruption from the status quo, so the odds of negative rates will be lower but not by a lot.”

To be sure, BOE Governor Andrew Bailey has made a point that doesn’t chime with the market movements: that sub-zero rates might be more effective during an economic recovery rather than a slump. Ranko Berich, head of market analysis at Monex Europe Ltd., finds bets on negative rates rising in tandem with expectations of a no-deal Brexit puzzling for this reason.

“The BOE’s own communication has made clear the MPC views negative rates as a tool best used at a time when banks are less worried about balance sheet risks, ideally the initial upswing phases of a recovery,” he said. “This suggests they would be highly unlikely to take rates negative as a knee-jerk reaction to a no-deal Brexit, which is precisely the kind of shock that would get banks worries about balance sheet risks.”

For now, though, the market is being driven by Brexit talks. Concern about the impact of no-deal on the U.K. economy has kept a lid on the nation’s bond yields, with gilts’ performance regularly out of step with peers. The 10-year benchmark yield traded at around 0.24% Tuesday, having fallen as low as 0.15% last week, and investors see more downside as a distinct possibility.

“Gilts offer limited protection, given yields are already low, but they’ll still fall further in a bad Brexit outcome as negative rates becomes the base case,” said John Roe, head of multi-asset funds at Legal & General Investment Management. “We don’t see negative interest rates as a problem per se. We just see it as an outcome that’s positive for gilts, which means it’s dangerous to be short.”

©2020 Bloomberg L.P.