Move Over, Bonds. It’s Stocks’ Turn in Emerging-Market Spotlight

Move Over, Bonds. It’s Stocks’ Turn in Emerging-Market Spotlight

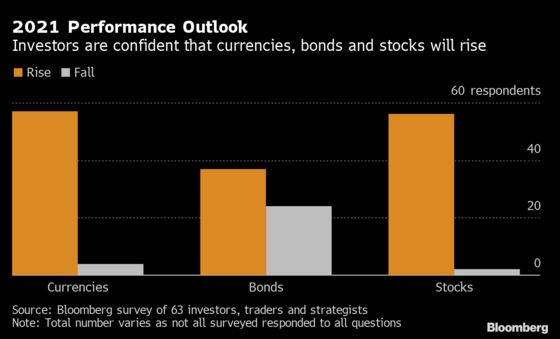

(Bloomberg) -- Stocks are edging out bonds as the choice of 2021 in emerging markets.

The world’s biggest money managers, from BlackRock to JPMorgan and UBS, are betting the post-pandemic economic recovery will be so swift that it’s no longer necessary to be content with the single-digit yields of developing-nation debt. Equities will offer much higher returns in 2021, they say, in a signal that a decade of underperformance may come to an end.

If fund flows are any indication, the rush into equities has already begun. A risk-on shift brought about by Joe Biden’s U.S. election victory and coronavirus vaccine successes has helped exchange-traded funds buying stocks get five times the deposits that bond funds have received in the past six weeks.

“Every standard framework model you use in finance would mean that equities will do better than bonds in 2021,” said Michael Bolliger, the Zurich-based head of emerging-market asset allocation at UBS Group Inc.’s wealth-management division. “Rebalancing tactically makes sense at this point. Our base-case scenario is that the world returns to normalcy and we will see a catch-up in growth and in cyclical markets.”

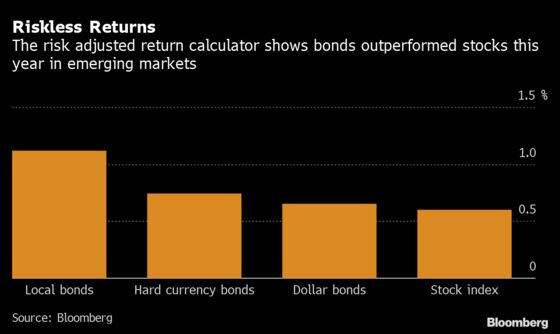

Bonds have been the most profitable asset class in emerging markets over the past decade, beating stocks in volatility-adjusted returns almost every year except 2017. For every $1 that investors gained from equities, they made $3 from local-currency notes and $7 from dollar-denominated debt during the period. A structural slowdown in China’s economy, a plethora of country-specific crises and commodity-price losses kept a lid on equity performance.

But all that’s about to change, money managers say. While the earnings outlook for stocks is increasing at the fastest quarterly pace in 11 years, bond yields have sunk to record lows. At about 3.5%, the average yield on both local-currency and dollar bonds is a full 3 percentage points below equity yields. And in an environment where corporate profits are growing but governments are saddled with unprecedented debt burdens, investors may find it more rewarding to stick with stocks.

“Our favorite asset class within emerging markets is equities because it has the highest potential for returns,” said Jan Dehn, the London-based head of research at Ashmore. “We expect flows to be very strong. When flows come in, financial conditions ease and domestic demand picks up. The domestic demand pickup is very supportive of emerging-market equities, but it ultimately undermines the attractiveness of bonds.”

UBS’s Bolliger agrees. Emerging-market stocks can generate double-digit returns, with so-called value stocks rising as much as 20% in the next six months, he said. His prediction for dollar-bond gains is 3%. MSCI Inc.’s EM equity index is on track for its seventh week of gains, extending this year’s advance to 14%, while dollar bonds have returned more than 6% year-to-date.

BlackRock Inc.’s 2021 outlook includes an overweight position on emerging-market equities because they will be “the prime potential beneficiaries” of the global economic upswing. The firm has a neutral stance on debt. JPMorgan Chase & Co. has similar calls.

“Our positive growth outlook for 2021 suggests more upside for emerging-market equities than for-emerging market sovereign debt,” said Sylvia Sheng, a Hong Kong-based global strategist at JPMorgan Asset Management. “Above-trend global economic growth next year will likely provide a favorable macro backdrop for the more cyclically-sensitive emerging market assets.”

It’s not that emerging-market stocks are cheap. The benchmark MSCI gauge trades at 15 times the projected 12-month earnings of its members, hovering at the 98th percentile of its valuation range of the past decade. If the expected earnings growth fails to materialize, stocks could undergo a rapid re-rating.

However, equities remain the best route to bet on the return of consumption. Bonds, which may benefit from a weaker dollar and a more stable outlook for global trade, will nevertheless be unable to capture the upside from consumer demand.

In fact, next year’s rebound will probably create consumer-price pressures, damping real yields and limiting the outlook for bonds, investors say.

“Rapid economic growth could prompt disorderly inflation, though the policy response is likely to be tempered by the U.S. Fed’s move to average inflation targeting,” said Jacob Grapengiesser, partner and head of eastern Europe at East Capital in Moscow. “In 2022 and beyond, sovereign debt and questions over fiscal sustainability must be expected to plague emerging markets.”

©2020 Bloomberg L.P.