Mortgage Investors May Get Relief from Surging Home Refinancings

Mortgage Investors May Get Relief from Surging Home Refinancings

(Bloomberg) -- Aggregate prepayment speeds are expected to show a decline in the next report, and that would be good news for mortgage investors.

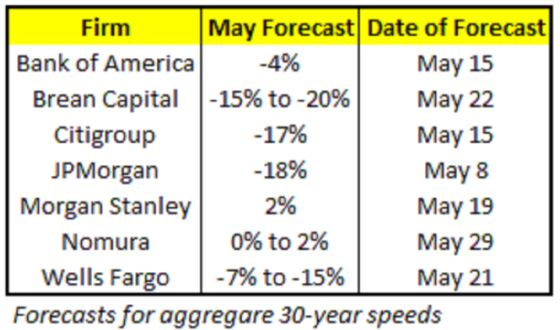

The expected drop of about 10% for May -- according to the average forecast among Wall Street analysts -- would be a relief for investors who saw increases of 26% and 42% the previous two months, respectively. The report is scheduled to be released Thursday afternoon.

A slowdown in speeds would be beneficial to investors because homeowners refinancing their loans return money to mortgage-backed security holders earlier than expected and at par. And with all 30-year MBS trading at a premium in the to-be-announced market, higher refinancings would hurt returns.

This is particularly true with mortgage bonds now trading at such lofty valuations -- the UMBS 2.5% 30-year TBA has surged over 3 points since the Federal Reserve resumed quantitative easing on March 16 -- so even a small change in prepayment speeds can translate to dramatic price moves.

Prepayments are dependent upon a number of variables, such as movements in mortgage rates and day count, which at 20 for May is two days lower than what was seen in April.

Yet, while the 30-year mortgage rate is now at a record low of 3.15%, the lag time between when a homeowner signs the loan paperwork and when the old mortgage is bought out of its pool requires looking back at data from around six weeks ago for any attempt to forecast prepayments. For instance, six weeks ago that mortgage rate was at 3.33%.

One lagging indicator that points to lower speeds is the refinance application index released weekly by the Mortgage Bankers Association. It has moved lower eight out of the last 10 weeks and has dropped over 50% since reaching a year-to-date high of 6,418 on March 6, though it remains 62% higher than it was one year ago. So while the threat of higher speeds have lessened for the next report, overall it still remains a concern for mortgage investors.

Another factor to consider is the potential speed for each specific mortgage cohort, as the more recent, better-credit borrowers are most likely to be willing and able to refinance. In a May 8 report, JPMorgan stated that “the market will likely see a divergence between the haves and have-nots,” while Nomura analysts wrote on May 29 that “recent-vintage cohorts (2019 3.0% and 3.5%) could continue to ramp up, while seasoned higher coupon cohorts could experience slower prepays.”

Over the long term, the issue of forbearance looms over the prepayment landscape. As of May 24, the Mortgage Bankers Association reported that 8.5% of the universe (just over 4.2 million homeowners) has now demanded forbearance. The question is how many of those loans will eventually default and require buyouts from mortgage pools. This can hurt performance because buyouts act in much the same manner as prepayments, returning money at par and earlier than expected to mortgage investors.

With the economy more than likely to take a large hit from a combination of the lockdowns and the uprisings across the country, the risk of a surge in buyouts once the forbearance period comes to an end is elevated.

- Christopher Maloney is a market strategist and former portfolio manager who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2020 Bloomberg L.P.