Mortgage Investors Flock to Specified Pools as Rates Drop

Mortgage Investors Flock to Specified Pools as Rates Drop

(Bloomberg) -- Investors will likely continue to look for ways to protect their mortgage-backed security portfolios as rates drop to their lowest level since November 2016. Buying specified pools is a popular way to do so.

Specified pools are bonds created using borrower characteristics such as credit scores, loan size or geographic distribution, designed to provide more certainty on when the underlying mortgages will be paid off.

That’s in contrast to buying “to-be-announced” or TBA mortgages, where investors know only a few characteristics like the coupon rate until such a time as the actual bonds are delivered by the seller.

Those buying specified pools are looking to shield themselves from dropping mortgage rates, which are encouraging more homeowners to refinance their loans. One of the main variables mortgage traders must accurately forecast to properly value their investment is the speed at which the underlying home loans will be paid off. Faster prepayments can hurt investors that paid more than 100 cents on the dollar for mortgage bonds because they get their principal back sooner than expected and at par, cutting into returns.

And speeds have been rising of late, surging 29% in July for Fannie Mae 30-year fixed mortgages. Next month is forecast to see an increase of about 10%, according to a recent JPMorgan report. And with the 30-year mortgage rate dropping to 3.60%, down from 4.94% as recently as November, the number of homeowners who can refinance has increased.

These lower rates means 64% of borrowers whose loans are bundled into Fannie Mae and Freddie Mac bonds and 78% of homeowners whose mortgages are packaged into Ginnie Mae securities now have enough incentive to refinance, said Scott Buchta, head of fixed income strategy at Brean Capital.

Bondholders that already own specified pools that are designed to protect from a spike in refinancings, such as the ones comprised of loans with low loan balances, have benefited from the rate rally.

That’s especially the case for 30-year conventional 4% and 4.5% pools, where a high risk for a surge in prepayments is thought to be concentrated. They display many “red flags“ that point to borrowers having faster response times to lower rates -- such as high FICO scores and large loan sizes.

The prices that investors are willing to pay (referred to as “pay-ups”) for 30-year 4% and 4.5% low loan balance specified pools, which historically have seen relatively slow prepayments, have risen about 3-13/32 and 3-27/32 year-to-date, respectively, according to data compiled by Bloomberg. Since the end of June, they have increased 31/32 and 1-19/32.

“The mix of high gross WAC coupon differentials across the stack and a large rate rally caused speeds to come in faster than expectations, resulting in deterioration of rolls and investors becoming flush with cash,” said Matt Kirstein, a director at INTL FCStone Financial Inc. in a interview. “These coupled with robust REIT and bank demand caused pay-ups to move meaningfully higher.“

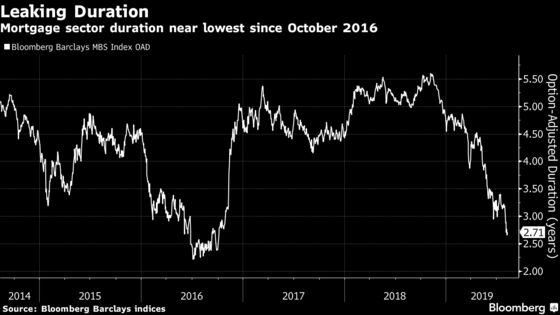

The increased ability of U.S. homeowners to refinance is also reflected in the Bloomberg Barclays U.S. MBS index duration. It now sits at 2.71 years, down from a recent high of 4.47 years on April 22 and at is now at its lowest level since November 2016.

Duration, a measure of a security’s price sensitivity to a change in interest rates, will drop on the assumption that principal payments on a given bond will be received earlier than expected. That’s what has happened with mortgage-backed securities.

And here the specified pools designed to protect against higher prepayment speeds can have yet another advantage -- they typically have longer duration than similar coupon TBA.

To contact the reporter on this story: Christopher Maloney in New York at cmaloney16@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Allan Lopez, Dan Wilchins

©2019 Bloomberg L.P.