Mortgage Credit for Some Americans Drying Up Amid Supply Deluge

Mortgage Credit for Some Americans Drying Up Amid Supply Deluge

(Bloomberg) -- A flood of mortgage-bond supply combined with a dearth of credit for lower-quality borrowers point to how the U.S. housing market is becoming more uneven when it comes to access to historically cheap debt.

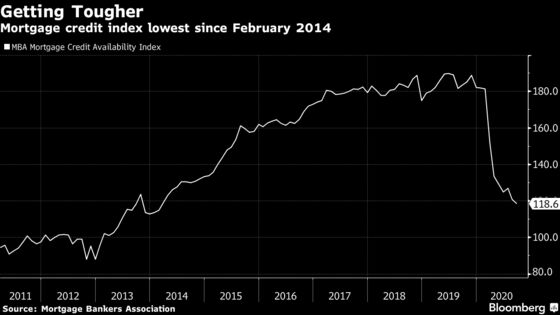

The Mortgage Bankers Association’s index of housing credit availability dropped last month to the lowest since February 2014. The benchmark has slipped eight of nine months this year and stands 35% lower than at the same time in 2019. The index is a broad measure of credit supply that weights various borrower credit characteristics and the range of products available to them.

That jars with a surge in the supply of mortgage bonds driven by increased home refinancings and purchases amid record low borrowing costs. At its current pace gross issuance is set to reach $2.8 trillion in 2020, which would be the most since at least 2003, according to Bank of America Corp. data.

This bifurcation suggests a widening of the gap in the U.S. housing market as homeowners or would-be buyers toward the bottom of the credit scale struggle to qualify for a loan. Lending standards have been tightening amid high unemployment following the Covid-19 lockdowns and fears that the economic recovery is stalling.

“There has been tightening around every margin,” Joel Kan, the MBA’s associate vice president of economic and industry forecasting, said in an interview. “A lot of low credit score programs went away.”

This is particularly so at Ginnie Mae, which is part of the Department of Housing and Urban Development and guarantees loans that are popular with first-time homebuyers and lower-income borrowers. The agency has been tightening the reins for some time now, and the pandemic accelerated the trend.

Ginnie Mae has reduced the flow of credit to borrowers with FICO scores below 700 and debt-to-income ratios above 40%, according to data provided by the Urban Institute. Whereas in January 2019 just over 44% of its purchase mortgages fell into that category, Ginnie reduced it to 38% in January this year and to 36% in August. For homeowners looking to refinance, the drop has been even steeper, from 38.5% in January last year to 12.8% one year later and to just under 5% in August.

“The reduction of available credit is detrimental to those looking to participate in the single best way to build wealth -- via homeownership,” said Laurie Goodman, co-director of the Urban Institute’s Housing Finance Policy Center, a Washington-based think tank.

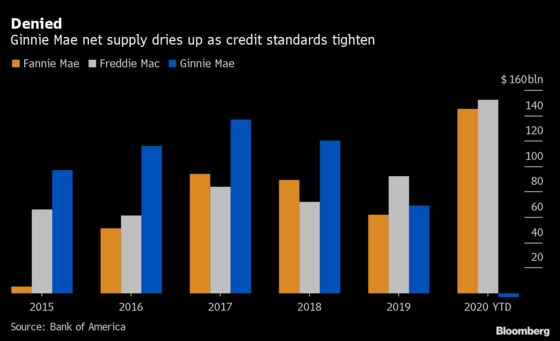

The tightening has halted growth in the universe of Ginnie Mae bonds outstanding. Through the end of September, year-to-date net issuance fell by $3 billion, compared with annual average net supply over the past five years of about $108 billion, according to Bank of America data.

Even looking at gross supply, where Ginnie Mae’s annual output has averaged 34% of the agency MBS total over the past half decade, so far this year is has dropped to 26%.

This may be prudent policy as creating a high rate of delinquent loans is something to be avoided even in the best of times. And servicers don’t like to have such loans on their books, either, according to Goodman.

“It costs more to service delinquent loans than performing ones,” she said in an interview.

And in the current environment that keeps lenders cautious. So while a 30-year mortgage rate of 2.87% is near an all-time low, only those borrowers considered a safe bet by them will reap the benefits.

©2020 Bloomberg L.P.