Morgan Stanley Says Quit Worrying About Giant Treasuries Supply

Morgan Stanley Says Quit Worrying About Giant Treasuries Supply

(Bloomberg) -- Bill Murray’s rousing speech in “Meatballs” had his character reassure summer campers fearing failure with the refrain “it just doesn’t matter, it just doesn’t matter, it just doesn’t matter.”

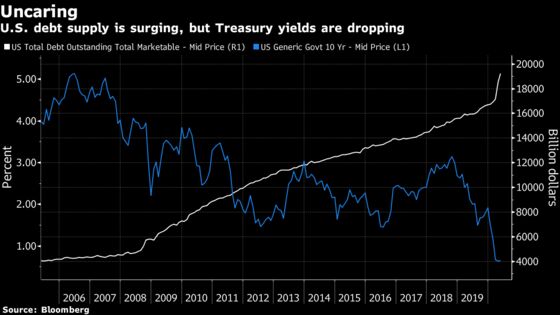

That’s pretty much what some experts are saying about the record deluge of U.S. government debt this year, when it comes to its potential impact on bond yields. Morgan Stanley’s Guneet Dhingra put it this way in a note Wednesday: “supply will go up. So will demand.”

The Federal Reserve’s plan to buy about $80 billion of Treasuries a month isn’t sufficient to mop up the federal government’s issuance. The Treasury Department last month said it expected to issue about $677 billion in marketable debt in the July-to-September quarter. And recent T-bill sales have shown evidence of supply concerns, potentially affecting interbank rates.

Nevertheless, Dhingra, Morgan Stanley’s head of U.S. interest-rate strategy, predicted that “an increase in Treasury demand will match the upcoming additional supply.”

While China is unlikely to help, overall foreign demand will probably rise, with Japan in particular having scope to boost purchases, Dhingra wrote. “Domestic investment funds, including mutual funds, have been a strong source of demand for Treasuries and are likely to remain so,” he added. Money-market funds are also seen as buyers, and Dhingra highlighted evidence that hedge funds stepped up during 2008-09 and 2018-19 episodes.

‘Not Potatoes’

It’s a fundamental misconception to think of supply and demand for Treasuries in the same way as, say, for potatoes, according to HSBC Holdings Plc’s Steven Major. While conceptually it might sound reasonable that bigger supply would drive down prices, that doesn’t work without considering demand, he wrote in a deep-dive look at the issue earlier this year.

Major found that government-bond demand is elastic, meaning it’s responsive to price: cheaper prices mean buyers are willing to take down a larger amount, in turn diminishing the price move when supply shifts out.

“Whilst supply expectations can have an impact” on intraday trading of bonds, “they are not meaningful to the long-term horizon bond yield forecasts,” Major wrote. “Even a big increase in supply does not have to result in a meaningful shift lower in the price.”

Yields ultimately are determined by expectations for short-term interest rates, plus any premium for buying longer-dated securities, the theory states. So it would take boosting prospects for growth and inflation to lift yields, Major concluded.

©2020 Bloomberg L.P.