Morgan Stanley Gives Up on Flattening Yield Curve Too Soon

Morgan Stanley Gives Up on Flattening Yield Curve Too Soon

(Bloomberg Opinion) -- Matthew Hornbach, global head of interest-rate strategy at Morgan Stanley, has never been afraid of making bold calls in the $15.3 trillion U.S. Treasury market. Even if they sometimes don’t pan out.

In July 2016, when the 10-year Treasury yield reached an unprecedented low of 1.32 percent, he pushed the envelope, declaring “the year of the bull for rates markets” would push the global benchmark to 1 percent. That didn’t happen. In what the bank’s chief cross-asset strategist deemed Morgan Stanley’s “most controversial call, by a country mile,” Hornbach projected in late 2017 that 30-year yields would fall to a record low 2 percent by the end of this year. That hasn’t happened, either: The 30-year bond just topped 3.4 percent for the first time since 2014.

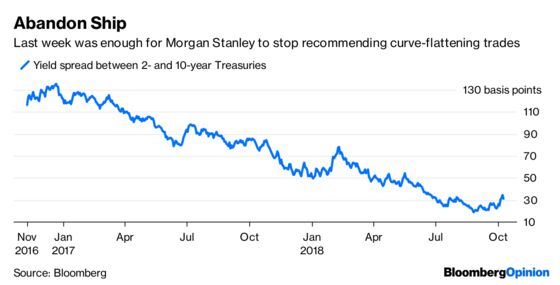

But even amid these too-bullish calls on longer-term Treasuries, the crucial prediction that Hornbach held on to was a wager that the U.S. yield curve would flatten toward zero. And that turned out to be not just the right call, but the story of 2017 — and much of 2018 — for the world’s biggest bond market. The spread between two- and 10-year notes narrowed to less than 20 basis points in August, from almost 140 basis points in December 2016. Investors and Federal Reserve officials alike were closely watching as it seemed destined for inversion, which historically has presaged a recession.

That trend reversed last week as 10-year and 30-year Treasury yields set new multiyear highs. The curve steepened by the most in eight months. Still, with a spread of just 30 to 35 basis points, it seemed more like a blip to strategists at Bank of America Corp., Barclays Plc, BMO Capital Markets and Societe Generale. Indeed, on Tuesday, the curve from two to 10 years flattened by 3 basis points, while the spread between five-year and 30-year Treasuries easily bounced off its 200-day moving average.

But Morgan Stanley apparently saw enough last week to issue a “mea culpa.”

“We were wrong to expect Treasury yields to be capped at previous year-to-date highs,” Hornbach wrote in an Oct. 5 note. And while it may not be the right time to enter curve-steepening trades, he said he could no longer recommend curve flatteners, either.

It was a surprisingly abrupt change of heart, particularly because the increase in yields last week seemed largely driven by the market breaking through key technical levels. Strong U.S. economic data helped initiate the sell-off, but positioning and momentum exacerbated the move. As I wrote, bond bears couldn’t form a clear narrative. When you’re blaming the surge in interest rates mostly on a rising term premium, it’s basically acknowledging that yields are going up because it feels as if they should.

To be fair, that was a perfectly reasonable feeling. The 10-year yield was range-bound for months even though the Fed showed no signs of slowing its rate increases; equities nevertheless managed to set records.

But Treasuries appear to be settling into a new range rather than lurching higher. On Tuesday, U.S. yields fell, even though bonds across almost all other developed countries sold off. And that rally came in the face of a big slate of auctions. On Wednesday, the Treasury will sell $36 billion of three-year notes and $23 billion of 10-year debt. On Thursday, it will offer $15 billion of 30-year bonds.

Of course, it’s no sure thing that the sell-off will abate. Ira Jersey at Bloomberg Intelligence wrote this week that a sustained break of the 3.25 percent level could push 10-year Treasury yields toward a test of 3.6 percent.

But what looks more and more certain is that Fed officials will keep boosting interest rates until something strongly indicates they shouldn’t. And that means short-term yields will continue to grind higher. But don’t just take my word for it. Here’s what Hornbach has to say:

“If economic data continues surprising to the upside, we think investors will begin looking for FOMC participants to become even more hawkish into year-end. What would a more hawkish FOMC look like? … We think scope remains for higher 2019/2020 median dots which could come at the December FOMC meeting. If market participants price in a more aggressive rate path in 2019 and 2020, the yield curve will find it tough to trend steeper, in our view.”

That sounds like someone who, deep down, is not quite convinced that his previous stance was all that wrong after all. Long-term yields don’t have much more room to rise, while the market could very well price in a faster Fed? It’s the same argument, just with yields at higher absolute levels.

It’s simply too soon to call the end of the flattening trend. Sure, much of the “easy money” has been made on the trade over the past two years. It’s one thing for the curve to flatten toward inversion, but it’s another to actually see two-year notes trade at a higher yield than 10-year Treasuries.

Morgan Stanley could turn out to be right that Treasury yields move in largely parallel fashion for the next few months. That’s a straightforward and respectable call. It’s just not what I expected after years of out-of-consensus forecasts.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.