Morgan Stanley Sees IPO Revival, But It Comes With a Big Caveat

Morgan Stanley Sees IPO Revival, But It Comes With a Big Caveat

(Bloomberg Opinion) -- At this point in the earnings season for big U.S. banks, it was clear that Morgan Stanley’s figures were going to be down — the more pressing question was by how much. After all, the firm derives almost all of its revenue from market-related fees, a weak spot for competitors like Bank of America Corp. and JPMorgan Chase & Co., which made up the shortfall with their consumer units.

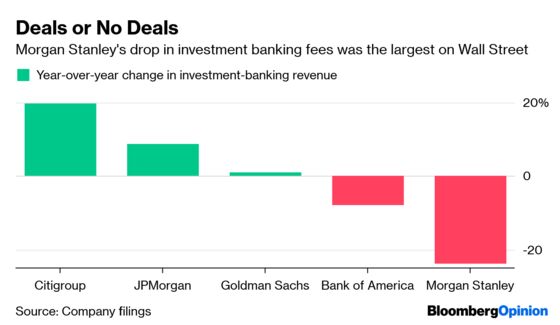

Investment banking came in especially weak, with Morgan Stanley posting the biggest decline among competitors. It brought in just $1.15 billion for advising on mergers and acquisitions, debt offerings and equity capital markets, which was 24 percent lower than the same period last year. Using nearly identical language to Goldman Sachs Group Inc.’s Chief Executive Officer David Solomon, who called it “a muted start to the year,” Morgan Stanley CEO James Gorman said the firm weathered “a slow start to the year.”

Morgan Stanley CFO Jonathan Pruzan was quick to turn to the future and pivot away from the first quarter in an interview with Bloomberg News’s Sonali Basak. “M&A is actually quite healthy — a lot of ingredients are in place to expect another robust year,” he said. “We gained market share in that business last year. We would expect to maintain or grow that market share.”

Wells Fargo Securities analyst Mike Mayo wasted little time in pressing for specifics in the question-and-answer segment of Morgan Stanley’s conference call. Pruzan stuck to adjectives. “We did see a significant portion of the IPO calendar get pushed out — not canceled, but pushed out,” he said. “Backlogs are healthy, and it’s really going to depend on the market’s openness and willingness to bring these deals from the pipeline into the market.”

That’s a significant caveat to the supposed brighter outlook. As I wrote earlier this week about Goldman, companies shouldn’t take anything for granted in late-cycle financial markets. Yes, the first three months of the year brought back renewed investor confidence, but any number of risks are still lurking, from continuing trade talks to a potential slowdown in global growth. Still, management’s initial optimism was good enough for Morgan Stanley investors, as shares rose more than 2 percent in pre-market trading after the earnings release.

In one of the more revealing parts of the Q&A, Gorman threw a bit of cold water on those expecting market exuberance to return. Less than 24 hours earlier, BlackRock Inc. CEO Larry Fink said “we have a risk of a melt-up, not a meltdown here” in equities. “Despite where the markets are in equities, we have not seen money being put to work. We have record amounts of money in cash,” he told CNBC on Tuesday.

Gorman, on the other hand, stressed that Morgan Stanley plans to remain vigilant in managing expenses, given that he and other senior officials can’t say for certain whether the rest of the year will be as strong as the same time in 2018:

“The fourth quarter was disappointing from a revenue perspective. We could see the decline coming. We didn’t know how the turnaround would happen. The shutdown appeared imminent and then actually happened. The trade wars were heating up, was taking down sentiment. There was a lot of negativity building through the end of the year. Around September-October, we started taking a hard look at expenses…”

“My view is we keep this discipline. The world remains uncertain. I’d love to think the next three quarters are better than the last three quarters of last year, but I’m a betting man – I’m not sure I’d make that bet right now. The world is uncertain, and until we see more clarity, we’re going to be very disciplined. It’s not a panic – it’s just good, smart expense management.”

That’s a fitting sentiment to cap off Wall Street’s earnings. No matter how you slice it, it’s going to be a tougher slog for banks than in recent years. For Morgan Stanley and Goldman, it remains to be seen whether markets really open up again after the severe losses of late 2018 and whether trading revenue can bounce back. In the IPO market specifically, Lyft Inc.’s high-profile fall from its opening level doesn’t exactly inspire confidence for the debut of Uber Technologies Inc., which counts both firms among its underwriters. As for the more retail-oriented banks, lower long-term interest rates means they can’t lean on rising net interest margins as they did before.

It was always going to be a rough quarter, and banks largely came out of it better than analysts expected. With stocks back near record highs, junk-bond sales accelerating and expectations for the IPO backlog to ease, they’ll likely face a much higher hurdle next time around.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.