Money Markets Avoiding Risky Bills: Debt Ceiling Anxiety Tracker

Money Markets Avoiding Risky Bills: Debt Ceiling Anxiety Tracker

(Bloomberg) -- Rate-market investors are sharpening their focus on exactly when the U.S. government might breach its borrowing limit, with clear yield premiums becoming evident in the bills market around the date that authorities have indicated is a risk.

And while Congress passed a nine-week spending bill Thursday to avert a government shutdown, the legislation does not include an increase or suspension of the debt ceiling.

U.S. Treasury Secretary Janet Yellen pointedly commented this week that things could come to a head by Oct. 18 -- just a few weeks from now -- while a report from the Congressional Budget Office released Wednesday said the department is likely to exhaust its ability to borrow as soon as late October or early November if politicians in Washington fail to raise America’s so-called debt ceiling in time.

The result is that investors have begun to shun certain securities that are at risk of non-payment, and auctions of four-week securities -- which mature right within the window for possible default -- have also become a no-go zone for some buyers. There is also an increasing tendency to park spare short-term cash in more palatable place. One of those, the Federal Reserve’s reverse repurchase agreement facility, on Thursday saw usage climb to a record $1.6 trillion.

Following are some charts to help gauge just how concerned markets are getting:

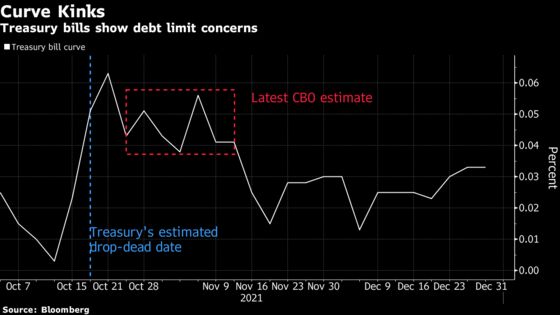

Avoiding Bills

If the U.S. runs out of borrowing capacity, those who hold debt that’s due to be repaid shortly afterward are among those who are immediately most exposed. Investors in those particular securities are therefore demanding a premium to compensate for the risk, and that’s showing up in bill yields. All else being equal, longer-dated bills usually command a higher rate than shorter ones. But right now, those coming due between mid October and early November -- the most likely window for a default -- have noticeably higher yields.

Morgan Stanley analysts said in a note Thursday that previous ceiling episodes, T-bills in the most-affected maturities have seen their yields rise by around 35 to 50 basis points. Their view is that the Treasury is likely to run out of borrowing capacity around Oct. 28 and that bills in that zone could cheapen quickly if there’s no clear resolution of the issue by the week of Oct. 11.

Buyers Absent

The unwillingness of investors to hold paper maturing around the riskier dates is also showing up in the results of government auctions. Four-week bills, the most short-term securities that the government sells on a regular basis, have seen the proportion bought by so-called indirect bidders drop in recent offerings. At Thursday’s four-week offering, indirect bidders were awarded just 5.5% of the $10 billion sale, the lowest since October 2015.

“The November 2 maturity date appears to be ‘hands off’ for the buyside due to the potential for a default at that time,” Jefferies economists Thomas Simons and Aneta Markowska wrote in a note to clients.

Indirect bidders are a group that includes money market funds, suggesting that their appetite for paper due around late October and early November has been waning of late. And the decrease is perhaps even more marked if you take into account the fact that the total size of these sales has also shrunk as the government navigates the ceiling issue.

Full Speed Ahead for Reverse Repo

Of course, investors still need somewhere to park their short-term cash even if they’re avoiding certain T-bills, and that’s helping to add to blockbuster demand to place money at the Federal Reserve’s facility for reverse repurchase agreements. While the record usage of these operations has been driven in large part by a simple lack of T-bills in the market -- an issue also related to the ceiling -- a shunning of particular securities is pushing some traders into the arms of the more trusted counterparty that is the Fed. That means that while Thursday’s quarter-end related result is the high-water mark for now, it’s still possible that usage could climb further.

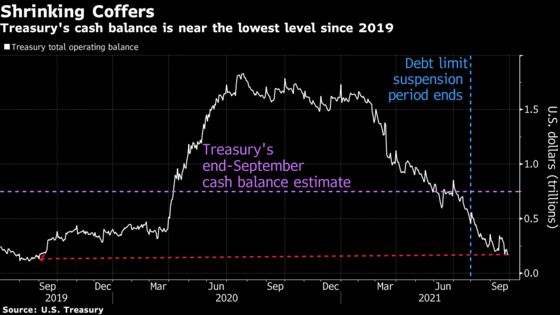

Smaller Buffer

Perhaps one of the most stark measures of how close America is to the edge is to look at the Treasury’s cash pile. Fueled by fiscal stimulus and Fed asset-purchase measures, the cash balance exploded to a record $1.83 trillion in July 2020, but has since shrunk to a fraction of that -- around $174 billion. A large part of that drawdown was planned -- indeed the Treasury was required to reduce its cash balance to a certain level before the ceiling was officially reinstated at the start of August. But the pile is now well below what the Treasury itself had forecast last month for the end of the third quarter. All that means that the government has less of a buffer to pay its bills if there’s a disruption in debt markets, which simply adds to the risks.

©2021 Bloomberg L.P.