Money-Market Funds Contemplate a Return to Abyss of Low Rates

Money-Market Funds Contemplate a Return to Abyss of Low Rates

(Bloomberg) -- The specter of a return to ultra-low U.S. interest rates is haunting money-market funds.

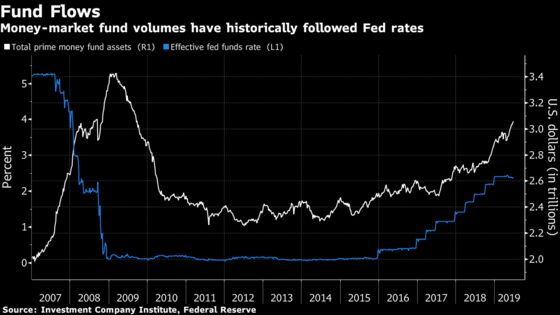

Cash is flooding into these highly liquid vehicles for investing in short-term debt for now, and the amount of assets held in taxable money-market funds this year poked back above $3 trillion for the first time in close to a decade. But there is growing disquiet among those who run and invest in them about the problems that might be caused by potential rate cuts from the Federal Reserve.

Treasury yields that veer closer to zero could prompt those with spare cash to seek out alternatives, and may also make the job of actually running the money that remains in such funds more difficult, according to investors and strategists at a conference in Boston earlier this week.

Bets on central bank easing have already dragged one-year Treasury-bill rates below 2% for the first time since early 2018, and that’s even as certain Fed officials appear to be pushing back against some of the more extreme easing scenarios -- such as a 50-basis-point reduction in July. The prospect that T-bills and other short-dated debt instruments may soon yield even less could at some point prompt a slowdown or reversal in money-fund flows.

Possible central bank easing is “not a death sentence, but it spells reduced margins and potential losses for the industry,” said Deborah Cunningham, chief investment officer of global money markets at Federated Investors in Pittsburgh. “It’s the fear of the unknown. Is it 50 basis points? Is it a program that takes us back to zero?”

The market has been here before. When the Fed lowered its policy target rate toward zero at the end of 2008, the amount of assets in taxable money funds was more than $3 trillion. Cash peaked at around $3.4 trillion in March 2009 and then proceed to drop by more than $1 trillion, bottoming out around the middle of 2012.

If the Fed does ease, prime retail funds are most vulnerable to outflows, according to Mark Cabana, head of U.S. interest-rate strategy at Bank of America Corp. That’s because money funds “will be seen as less desirable” amid a re-steepening of the Treasury yield curve, he said during a panel discussion at the Crane’s Money Fund Symposium.

Alex Roever, JPMorgan Chase & Co.’s head of U.S. rates strategy, said that money funds have historically tended to suffer from outflows around one-to-two years after Fed reductions, and the low overall level of rates plays a greater role in driving that than the actual process of easing.

Of course, the problem of low yields is just one of the many challenges facing the short-end of the U.S. interest-rate market. While that topic dominated discussion at this year’s Crane’s conference, attendees also grappled with issues ranging from America’s debt ceiling to the Secured Overnight Financing Rate and sponsored repurchase agreements. Here’s a brief rundown on some of these issues:

SOFR Debt

Issuers have been selling debt linked to the new benchmark developed by the New York Fed as a potential replacement in dollar markets for the London interbank offered rate. Yet while money-market funds have been scooping the debt up, there appears to be some hesitation about fully committing to the rate, which is derived from pricing in the repurchase-agreement market. The lack of a credit component -- which Libor has -- is one potential question mark hanging over it, and SOFR has also experienced various growing pains since its introduction.

Todd Bean, a fund manager at State Street Global Advisors, said at the conference that he expects portfolio managers to remain cautious about getting involved with any longer-dated floating-rate notes linked to the benchmark. Federated’s Cunningham, meanwhile, said that the end of Libor is “not a done deal,” and in a pun-laden panel discussion on the topic opined “it ain’t over ’til it’s SOFR.”

Sponsored Repo

Government money-market funds have grown since 2016’s industry reforms, spurring an increase in appetite for repurchase agreements that in turn is fueling demand for so-called sponsored repo. These are transactions in which dealers on the Fixed Income Clearing Corporation’s cleared repo platform sponsor non-dealer counterparties, and the amount of money-fund cash invested in this area last month climbed to a record $154 billion.

Travis Keltner, managing director of funding and collateral at State Street, said sponsored repo will be an issue regardless of what the Fed does with monetary policy. He also underscored the idea that an increased supply of Treasuries is creating more volatility in repo generally, helping to drive activity in the market. Michael Bird at Wells Fargo Asset Management said this week that FICC-sponsored repo now accounts for more of his firm’s repo volume than any other single counterparty. FICC is about “as sexy as you can get” for new government-sponsored repo products, he said.

The U.S. Debt Ceiling

The next stage in the seemingly constant battle over America’s debt limit is looming on the horizon, with the Treasury Department potentially exhausting its current borrowing authority around October. But with questions around the Fed taking center stage, concerns over the ceiling are taking a back seat for many investors.

Jeff Weaver, head of money funds and short duration at Wells Fargo Asset Management, said that he’ll start to get concerned about the debt limit around late-August or early-September, but nevertheless expects the government will “come up with what is correct and right” at the last minute. Yet even if there is an agreement in Washington, the very resolution of the ceiling dilemma may create waves in short-end markets and add to funding-market turbulence in the fourth quarter.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.