Mike Ashley Gets Desperate With Debenhams Bid

Mike Ashley Gets Desperate With Debenhams Bid

(Bloomberg Opinion) -- So Mike, what took you so long?

Sports Direct International Plc said late Monday that it was considering a cash offer for the shares in Debenhams Plc that it did not already own.

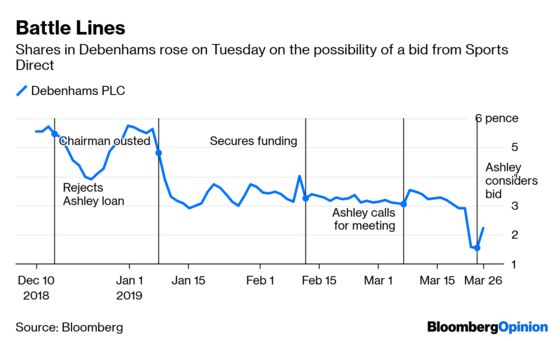

In one respect, Sports Direct founder Mike Ashley’s timing looks impeccable. Shares in Debenhams were trading at an all time low of 1.55 pence on Monday. Even with the increase to over 2 pence on Tuesday, it would still cost Ashley only about 19 million pounds ($25.1 million), before any takeover premium, to buy out other shareholders. A year ago, the price would have been around 180 million pounds before any premium.

He can also answer Debenhams’ legitimate challenge: if he wants control of the retailer he can make a cash offer.

But on the other hand, Ashley looks increasingly desperate.

As I have argued, his mistake was buying Debenhams’ equity rather than debt. Had he been a lender he would have been in the driving seat in the event of any debt for equity swap. As it stands, as an equity holder, he faces the prospect of being heavily diluted.

If he really wanted to secure the department store for his empire, he could have made an offer some time ago. Still, he got there in the end.

Sports Direct makes clear that there is no certainty of a bid. But assuming it does, and that it is successful, Ashley would gain the power to stop any debt for equity swap or administration that would severely disadvantage shareholders. Though he’s already taken some of the pain by writing down the value of his stake, for other investors, receiving something from a Sports Direct bid is better than being wiped out.

Sports Direct already has the headroom to manage the offer, since it has its own 1 billion pound facility that it can draw on. It could also refinance any debt that it takes on, potentially on better terms than Debenhams would be able to achieve.

The problem for Ashley is that while Debenhams’ equity might be cheap, and its pension is in decent shape thanks to its years in private equity hands, the debt has reached about 560 million pounds. And his bid won’t stop the department store’s plans to secure another 200 million pounds of borrowing facilities.

Sports Direct had 505.5 million pounds of net debt at Oct. 28. Assuming it took on the whole of Debenhams’ borrowings, net debt would be about four times forecast full-year Ebitda. That ratio could hamper its financial flexibility, at a time when it is already facing heavy investment to revive House of Fraser, expand Flannels and maintain Sports Direct. A turnaround of Debenhams would also require further spending.

Sports Direct shareholders should already be worried about whether its management team has enough bandwidth to deal with its rapidly expanding empire. Taking on Debenhams could be a significant distraction at a time when high street conditions remain challenging.

If a firm bid does emerge from Ashley, that would be the most palatable option for Debenhams shareholders. For Sports Direct investors, the prospect is less appealing. Even so, shares in the sportswear retailer rose more than 1.5 percent on Tuesday. It looks like they are becoming increasingly resigned to the House of Ashley.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.