Micron Analysts Cautious About DRAM Chips Ahead of Results

Micron Analysts Still Cautious About DRAM Chips Ahead of Results

(Bloomberg) -- Micron Technology Inc. analysts continued to be cautious about the impact that pricing weakness for the company’s DRAM memory chips would have on its earnings, with BofAML cutting its expectations for the next three years and Cross Research downgrading the stock to hold. The moves come just days before the company’s next quarterly report.

Shares rose 2.0 percent, although this comes after a two-day decline.

The calls were merely the latest examples of analyst concern about Micron, which last week topped Mizuho Security’s "2019 stay away" list, an investor survey it conducted on semiconductor stocks.

BofAML slashed its profit expectations for 2019 through 2021, with 2019’s view going to $6.89 a share from $8.53.

“Like Samsung and Hynix, Micron too suffers from price drops and, thus, margin squeeze,” wrote BofAML analyst Simon Woo. He maintained his buy rating and $50 target on the stock, but expects average selling prices for both DRAM and NAND chips to decline more than 20 percent on a sequential basis in the second quarter.

According to Bloomberg data, nearly 70 percent of Micron’s 2018 revenue came from DRAM chips. The company will report second-quarter results on Wednesday; analysts are looking for earnings of $1.69 a share on revenue of $5.89 billion. This represents an earnings decline of 40 percent and a drop of nearly 20 percent in sales compared with the prior year.

Cross Research analyst Steven Fox also cut his earnings estimates on Micron for 2019 and 2020; he added that this was the third time he had done so in the past six months, and that he doesn’t expect positive earnings growth for another four quarters.

Average selling prices for DRAM chips suggest "we underestimated the extent of excess DRAM inventories (and probably NAND as well)," he wrote, adding that excess inventories would also “limit gross margin recoveries” at Micron.

Also on Friday, Mizuho Securities trimmed its price target by $1 to $44, writing that DRAM pricing trends continued to be down “as inventories remain high.” Analyst Vijay Rakesh added that trends for NAND chips “appear better with 2Q inventories coming down,” joining a recent chorus of analysts who are becoming optimistic about NAND.

Currently, 18 analysts have a buy rating on Micron, while 13 rate it a hold and just one recommends selling the stock. The average price target is $47, which represents upside of nearly 22 percent from the company’s Thursday close.

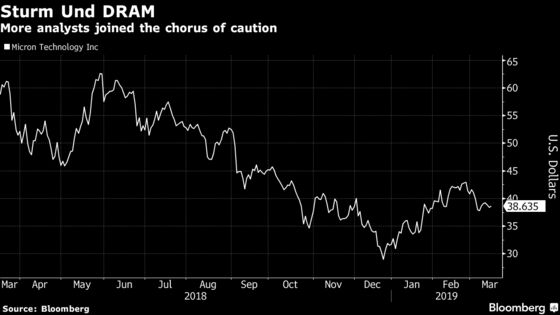

Micron shares have dropped nearly 40 percent from a May peak, though they’ve rebounded 32 percent off a December low.

To contact the reporter on this story: Ryan Vlastelica in New York at rvlastelica1@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Brad Olesen

©2019 Bloomberg L.P.