Meredith Whitney Was Flat-Out Wrong About Municipal Bonds

Meredith Whitney Was Flat-Out Wrong About Municipal Bonds

(Bloomberg Opinion) -- “Being too far ahead of your time is indistinguishable from being wrong.”

That’s what Howard Marks, chairman and co-founder of Oaktree Capital Group LLC, wrote in a memo to clients about 11 years ago. Around that same time in late 2007, banking analyst Meredith Whitney made a prescient negative call on Citigroup Inc. that exacerbated a market sell-off and, she said, prompted death threats. Perhaps emboldened by that experience, she made another headline-grabbing prediction in a December 2010 broadcast of CBS Corp.’s “60 Minutes” program: There would be “50 to 100 sizable defaults” in the U.S. municipal market in the coming year, totaling “hundreds of billions of dollars.”

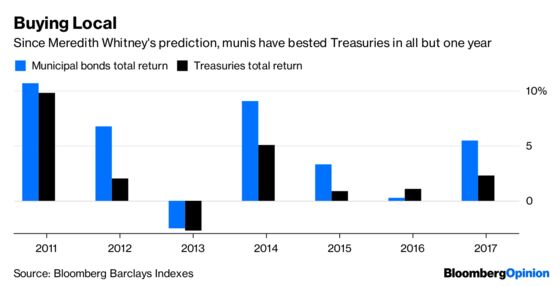

That didn’t happen. Her call was widely ridiculed — and remains so to this day — by members of the $3.8 trillion municipal market. In November 2014, Bloomberg News’s muni maven Joe Mysak provided a comprehensive takedown: a 34-page special report titled “The Muni Meltdown That Wasn’t.”

Well, she’s back. Or, at least, the ideas that Whitney represents. The Wall Street Journal published an article last week titled “Prophet of Muni Market Doom Wasn’t Wrong — Just Early.” The takeaway is that Whitney simply erred by putting a precise number and time period on her prediction, but her analysis was sound.

“Since then a dramatic decline in the finances of state and local governments has made it increasingly likely that she will be remembered as right but early. Municipal bond investors should heed the warning … ratings firms and fund managers in the sleepy sector operate under the assumption that everything will somehow continue to work out.”

First of all, Whitney is hardly a “prophet.” Six months before her “60 Minutes” appearance, none other than Warren Buffett predicted a “terrible problem” for state and local government debt in the years ahead. Second, a large swath of investors in the so-called sleepy market were wide awake ahead of defaults from Detroit and Puerto Rico. Their reckoning was a long time coming, and many of those bonds wound up in the hands of distressed funds. Lastly, a reminder: Being early is the same as being wrong.

Few muni investors are oblivious to Whitney’s criticisms of state and local government finances. I’ve read her book, “Fate of the States: The New Geography of American Prosperity.” It’s easy to fly through because the analysis is uncomplicated and it repeats the same conclusions. Some states (primarily on the coasts) have too much debt and have inflated promises to retirees, the argument goes. People will take note and pack up for places with lower tax rates and cheaper cost of living.

No one’s denying that’s what happened over the span of decades in Detroit, nor that a population exodus helped exacerbate Puerto Rico’s woes. Illinois, the lowest-rated U.S. state, is starting to face a similar problem, with a steady trickle of outmigration for four consecutive years. The Chicago Tribune’s editorial board declared that “what we call the ‘Illinois exodus’ is real.” I’ve written about how Connecticut officials shouldn’t outright dismiss the possibility that the state could one day default, in no small part because of demographic shifts.

The thing that Whitney and her ilk failed to grasp was that for all but the most distressed cities, the issues of a demographic death trap and pension funding remain firmly a long-term question — even now, eight years later. Yes, maybe state and local governments could have done more to shore up their systems during this bull market in stocks. But their tax revenue exceeded their 2008 levels only once in the following six years as the economy recovered from the recession, according to Census Bureau data. That’s hardly a palatable time to dump money into pensions.

And yet the plans as a whole aren’t in as dire shape as many might think. A study last year by Milliman found the aggregate funded ratio of the 100 largest public pension plans was 70.7 percent, even though one-third of the funds reduced their discount rates, which makes their figures look worse (though probably more truthful). A 100 percent ratio isn’t necessarily optimal at a given point in time — in fact, research suggests 80 percent is a reasonable level. Taken as a whole, state and local government pensions aren’t so far off that a doomsday is inevitable.

Not surprisingly, the outliers steal the spotlight. “Zooming in on the weakest links is downright scary,” the Whitney article says, pointing to Connecticut, Illinois and New Jersey. It’s true that those states have real problems and politicians can no longer employ the tried-and-true method of passing the burden to their successors. But the death knell isn’t necessarily higher interest rates, as the article describes. In fact, for pension funds, which invest a healthy amount in fixed income, a return to historically normal yield levels should provide a source of safe returns that was absent for much of the post-crisis era.

It’s fair to ask whether some states and cities are prepared to withstand another deep recession. Or whether 177 basis points of extra yield is enough to compensate for the risk of owning Illinois debt versus top-rated munis. But it’s simply revisionist history to say Whitney was right all along with her 2010 call, which ignited a bout of panic in the municipal market about events that never materialized. The truth is, she whiffed.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.