Markets Stare Into Dark Before Lagarde’s First Decision Day

Markets Stare Into the Dark Before Lagarde’s First Decision Day

(Bloomberg) -- A scan of analyst research notes is all that’s needed to conclude investor uncertainty is running high about what to expect from the European Central Bank’s final policy meeting of the year -- which is also Christine Lagarde’s first.

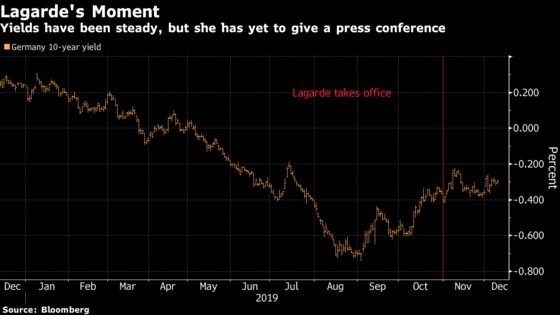

Money markets show no clear expectations for the future direction of interest rates -- prices currently imply a roughly 30% chance of another cut by September 2020. Benchmark German yields remain around the middle of their range over the last two months, and the euro’s one-month implied volatility is near a record low.

In the five weeks since taking office, new ECB President Lagarde has given away little on her views on monetary matters. That at a time when markets are already grappling with a raft of global risks -- from a growth slump to trade tensions and Brexit -- which have reduced room for central banks to maneuver.

Investors will be scouring Lagarde’s press conference for clues on her policy priorities and what she might do if the economy takes a turn for the worse. Any hint that she is willing to further extend her predecessor Mario Draghi’s accommodative approach, by cutting rates further or boosting asset purchases, could fuel a bond rally.

“This is not an autopilot meeting,” Bob Michele, chief investment officer at JPMorgan Asset Management, told Bloomberg TV. “Will she cut rates another 25 basis points? I think so. Will they double the size of the balance sheet expansion from 20 billion euros ($22 billion) to 40 billion euros a month? I think so.”

Former ECB chief Draghi was an ally of the bond market, announcing unprecedented easing measures over the course of his tenure to combat slumping inflation and dire debt dynamics in Europe’s periphery. Aside from calls for more spending from governments and signs that climate change could grow in importance, Lagarde is yet to reveal her policy outlook.

That raises the risk of a surprise for markets. Bank of America Merrill Lynch warns the market may reassess the possibility of the ECB lifting interest rates back to 0% following Thursday’s policy announcement. NatWest Markets is recommending investors short German bonds. Barclays Bank sees a risk of Lagarde unintentionally miscommunicating to the market.

What bank analysts say:

Morgan Stanley

- Markets will be focused on the substance and timing of the upcoming strategy review, what will be required for the ECB to be “resolute in its commitment to deliver on its mandate” and any discussion about the distribution of APP buying, writes strategist Tony Small

- “It’s possible that some of the recent bobl cheapening may be due in part to some uncertainty associated with how the ECB will proceed under Lagarde and what the strategy review may entail”

NatWest Markets

- Investors should “short bunds for 2020, and for what’s left of 2019,” strategist Giles Gale writes in note

- “We expect no change from the ECB, but Lagarde’s first post-ECB press briefing is required viewing”

- “We are lukewarm on another rate cut, although pencil one in for June,” while “we ultimately expect that more hikes can be priced into 2021”

- Has a long position in the euro versus dollar among top trades for 2020

Bank of America

- “The market may reassess the chances of an earlier return to 0%,” write strategists Sphia Salim and Ronald Man, referring to the central bank’s deposit rate

- If the market interprets a potential change to the inflation target as “raising the chances of inflation overshoot, it should support a real rate curve flattener”

- “If instead, the market starts to worry about a change that renders the ECB comfortable with inflation settling closer to 1.5% than 2%, it will be bearish breakevens and front-end rates”

UBS

- “We expect a gradually stronger euro, as the euro zone economy is set to improve in 2020,” write strategists led by Ricardo Garcia

- Sees 2021 inflation largely unchanged from 1.5%; however “Lagarde will also add the year 2022, which should likely show some convergence toward the inflation target, raising questions about the end of QE and the first rate hike”

- Sees bund yields trading sideways into the new year: “we recommend staying in the middle lanes and refraining both from the short end of the curve (which offers an almost certain loss) and from the very long end, which could be hit hard in the case of a positive economic outcome”

Barclays

- “Given the already notable repricing of EUR rates and fairer market levels, we think the bar is not low for another leg of a substantial move one way or another,” write strategists Cagdas Aksu and Max Kitson

- Interprets recent comments from Lagarde as suggesting monetary policy will remain accommodative

- Outlines two risks:

- “The first risk is of unintended miscommunication, especially when Lagarde answers journalists’ questions during the upcoming press conferences”

- The second, “if the strategic review of the policy takes a long time to conclude (which is possible) and the economy shows signs of weakening, the market could quickly go back to testing the ECB’s mandate credibility with disinflationary/deflationary type bull-flattening again”

- Recommends being long the Spanish five-year bond versus the two-year and 10-year, as well as Spain 10s30s vs Germany

Toronto-Dominion

- “This is one where Lagarde needs to spend most of her attention focused on establishing her credibility within the Governing Council rather than with the markets as investor expectations are pretty low this time around,” says Ned Rumpeltin, an FX strategist at the bank

- “We are looking for the FX market to show only a mild reaction to the December ECB policy meeting”

--With assistance from James Hirai.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Paul Dobson at pdobson2@bloomberg.net, Anil Varma, Michael Hunter

©2019 Bloomberg L.P.