Market's Favorite Recession Indicator Lurches Lower in New Year

Market's Favorite Recession Indicator Lurches Lower in New Year

(Bloomberg) -- Traders return to their desks in the new year with a familiar warning signal flashing even more strongly than before -- the Treasury yield curve got even flatter, feeding the market’s worst suspicions about the U.S. economy.

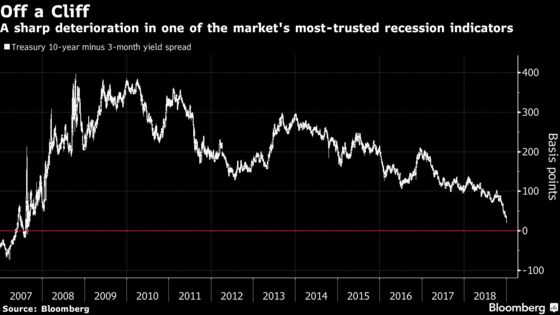

Market watchers noted a dramatic compression in what is arguably the most reliable indicator of recession -- the gap between the 3-month and 10-year Treasury yields.

This spread hit a post-crisis low of just 18.6 basis points in early New York trading Wednesday, barely half the intraday peak it reached on Dec. 31. The gap has since pulled back toward its opening level for the day of around 24 basis points, but the narrowing trend is hard to ignore as U.S. economic data deteriorate and traders start pricing in the possibility of a Federal Reserve rate cut in 2020.

Interest-rate strategists at BMO Capital Markets point out that the slide in this indicator just made Fed Chairman Jerome Powell’s job “that much harder.” While central bank officials have warned against over-interpreting flattening of the widely watched 2-year to 10-year curve, BMO points to “a great deal of academic research” around the curve from 3 months to 10 years, and “it is generally accepted as being a better recession predictor.”

They cite, in particular, analysis by the Federal Reserve Bank of Cleveland, whose own model indicated back in mid-December about a 24 percent chance of recession in the coming year. At that point the spread between 3-month and 10-year yields was considerably wider and BMO strategists reckon that “the next recalculation of this model in two weeks will surely show a material increase in the chance of a recession.”

The strategists draw particular attention to the 20-basis-point level for the spread, which they say has worked as a gauge for Fed policy in the past few decades. They note that crossings of that threshold in 1989 and several times in the 1990s preceded by a matter of months either a rate pause or cut from the Fed. One outlier was in 2006, when officials carried out four more rate hikes before embarking on an easing cycle.

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Vivien Lou Chen

©2019 Bloomberg L.P.