Malaysia Debt Could Do With More Central Bank Love Amid Deficit Fears

Malaysia Debt Could Do With More Central Bank Love Amid Deficit Fears

(Bloomberg) -- Malaysian bonds are starting to show some concern about the nation’s rising fiscal deficit. It may be time for the central bank to respond.

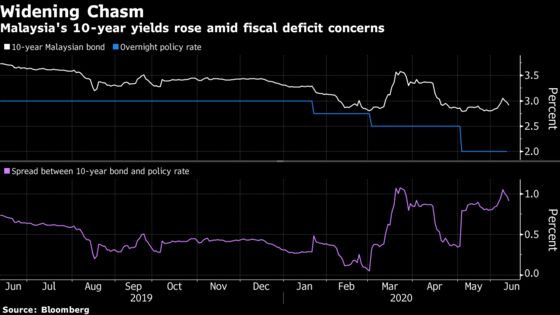

The nation’s 10-year yield briefly climbed above 3% this week, from as low as 2.79% in May, after the authorities pledged to pump in another 35 billion ringgit ($8.2 billion) to counter the impact of the coronavirus. That’s on the top of the 260 billion ringgit announced earlier. The government is now forecasting the fiscal deficit to widen to 5.8% to 6% of gross domestic product, the most in a decade.

Demand for bonds by domestic investors was lackluster even before the latest round of stimulus was announced on June 5. Total bids at an auction of three-year Islamic debt on June 3 only just scraped in above the amount on offer, compared with a bid-to-cover ratio of more than three times at a similar sale of 10-year Islamic securities in April.

The spread between benchmark 10-year yields and the central bank’s overnight policy rate has more than doubled over the past six weeks. It climbed above 100 basis points earlier this week, matching the peak seen at the height of the coronavirus sell-off in March. The prospect of further interest-rate cuts may revive demand for local bonds, but the market isn’t pricing in a full 25 basis-point move at any point in the next three months, according to swaps data compiled by Bloomberg.

Igniting Interest

There’s something else the central bank could do though to revive local interest.

While policy makers have already lowered the reserve requirement ratio for local banks by 100 basis points to 2% and included bonds as reserve-compliant assets, there’s room to go further. The ratio was cut as low as 1% in 2009 during the global financial crisis. Both Indonesia and the Philippines have lowered their respective ratios by 200 basis points, albeit from a much higher base, and this has helped ensure onshore banking book demand remains robust despite widening budget deficits.

Other regional central banks have also directly intervened to support their domestic bond markets. Bank Indonesia is buying up to 25% of the government’s debt offerings in primary auctions as well as in the secondary market. The Philippines central bank snapped 300 billion pesos ($5.98 billion) of government debt in March under a repurchase agreement, with scope to buy more.

Of course, Malaysian policy makers can point to a number of other factors that will help support the bond market even without their intervention. The recent doubling of Brent crude to around $40 per barrel will be positive for the nation’s budgetary position, while muted inflationary pressures will continue to underpin real yields.

In the near term though, it’s likely Malaysian bonds will remain under pressure unless the central bank takes further steps to shore up demand.

What To Watch

- Bank Indonesia meets Thursday after unexpectedly keeping its benchmark unchanged at its previous gathering on May 19. The U.S. equity rout sparked a rupiah selloff on Friday, with Bank Indonesia stating its intention to intervene to support its spot, domestic NDF and bond markets. Rupiah weakness going into the Tuesday decision may reduce the odds of a rate cut

- Indonesia’s next conventional bond auction on Tuesday will be closely watched after demand climbed to the highest in more than four years at the prior sale on June 2

- Thailand will auction five- and 15-year bonds on Wednesday. The government said Friday it is mulling a 20 billion baht ($646 million) stimulus program to boost tourism, although no details were provided on how it would be funded

Note: Marcus Wong is an EM macro strategist who writes for Bloomberg. The observations he makes are his own and not intended as investment advice.

©2020 Bloomberg L.P.