Lyft and Uber Are Easy to Understand and Hard to Value

Lyft and Uber Are Easy to Understand and Hard to Value

(Bloomberg Opinion) -- What is Lyft Inc.? It seems like an easy question. Lyft connects people who want a ride with ersatz taxi drivers. But for investors in Lyft’s coming public stock offering, the answer is trickier.

Investors want to be able to classify companies into familiar categories. When Facebook went public in 2012, its business model was half-baked but investors understood the financial dynamics of internet advertising, which gave them a starting point to assess the company. There are lots of comparable companies to measure the value of young business software firms like Slack Technologies Inc., which is also aiming to go public soon.

In one sense, Lyft and Uber are like eBay, Priceline, GrubHub, Craigslist and other “marketplace” businesses that match willing buyers with willing sellers. A marketplace is one of the established business models for technology companies, and investors are relatively comfortable assessing how much to pay for their shares.

The taxonomy game is tough for Lyft and particularly for its bigger and more complex rival Uber Technologies Inc. They are not exactly like any marketplace that has came before. They’re not exactly transportation companies, nor would they want to be valued that way. Novelty means that Lyft and Uber are doing something original. But novelty also complicates the IPO pitch.

Lyft — which may file its IPO paperwork as soon as this week — is like restaurant software company GrubHub, but not really. It’s also like eBay, but not really. Similarly, it’s like Booking Holdings Inc.’s online travel businesses such as Priceline.com, but not really. Lyft and its bankers will twist themselves into pretzels to come up with some rational comparable companies that investors can assess. This exercise in rationality is necessary but ultimately pointless.

The narrow question is how to value each dollar of Uber or Lyft revenue. The broad question and the basis of whether to own shares is whether Uber or Lyft will become lasting, large and valuable. That is an exercise in faith, not mathematics.

For a moment, though, let’s play investment banker.

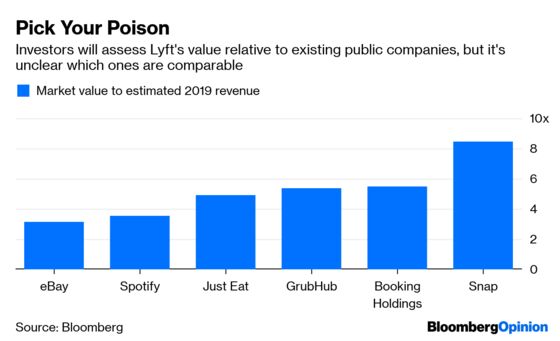

Lyft appeared on pace for roughly $2 billion in revenue for 2018, if I extrapolate the company’s reported revenue for the first nine months of the year. Let’s say Lyft’s revenue nearly doubles this year to $3.75 billion. Applying the same revenue multiple as GrubHub Inc., which connects diners with restaurants for takeout and delivery and in some cases delivers the food itself, Lyft would have a valuation of about $20 billion. That’s about where the company is aiming for its IPO valuation, and it may not be a coincidence. Bloomberg News has reported that investment bankers were targeting Lyft’s valuation based in part on a comparison to GrubHub’s food delivery business.

You could also suggest European restaurant software company Just Eat PLC, Booking Holdings or the digital music service Spotify Technology SA as comparable companies. The first two are about the same revenue multiple as GrubHub.

Again, is it appropriate to pay the same relative price for a Lyft share as for one of GrubHub, Just Eat or Booking Holdings? No. The companies’ businesses are different, their growth rates are different and their profits are definitely different from those of money-losing Lyft. If they believe, investors will come up with a logical justification for paying whatever it costs to buy shares. That doesn’t make the stock purchase rational.

That brings me back to the broader question. Lyft and Uber are hard to value not only because they’re unlike existing public companies but also because it’s not yet clear whether the business of facilitating rides at the tap of a smartphone is financially viable in every city.

Lyft and Uber can be widely popular and transportation-changing phenomenons but still might not be financially sustainable. Lyft and Uber are growing fast, but are those rates a capital-fueled mirage? I don’t know. Even if people keep riding and drivers keep driving, can the business be profitable? And how big is the market? I don’t know. Investors don’t know, either.

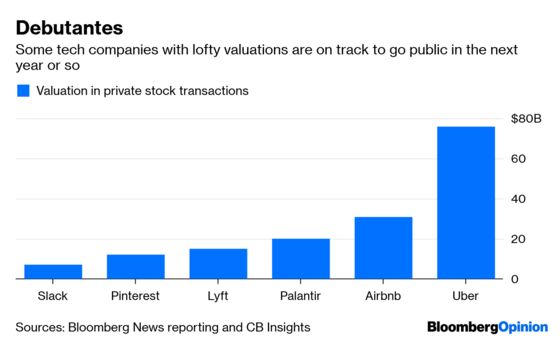

Any IPO is inherently a plunge into the unknown, but some unknowns are more unknowable than others. Lyft and especially Uber are the deepest darkest corner of unknown. Future public companies, including Airbnb and a growing variety of other young marketplace startups, will have similar unknowable unknowns.

My figure will be wrong but not wildly so. Investors will most likely look to 2020 financials to assess Lyft's valuation, but I'm not willing to extrapolate Lyft's revenue by another year.

The comparison to GrubHub is less appealing to Lyft backers than it was when bankers were working on their IPO pitch last fall. At the end of September,GrubHub was valued at 10 times the company's estimated 2019 revenue, compared with 5.4 times now. Using that richer multiple and my extrapolated figures for Lyft's 2019 revenue, the company's valuation could be close to $40 billion.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.