Lower-Credit Homeowners Weigh Heavily on U.S. Mortgage Market

Lower-Credit Homeowners Weigh Heavily on U.S. Mortgage Market

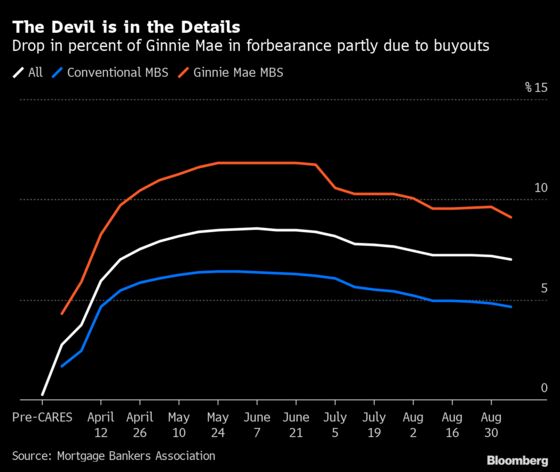

(Bloomberg) -- Almost twice the percentage of Ginnie Mae borrowers have demanded forbearance compared to conventional ones, according to a Mortgage Bankers Association report on Monday.

Mortgages in forbearance have dropped to just over 7% of the overall universe, the lowest since April. However, Ginnie Mae has a higher share of those - 9.1% versus 4.6% for conventional mortgages backed by Fannie Mae and Freddie Mac, the MBA data show.

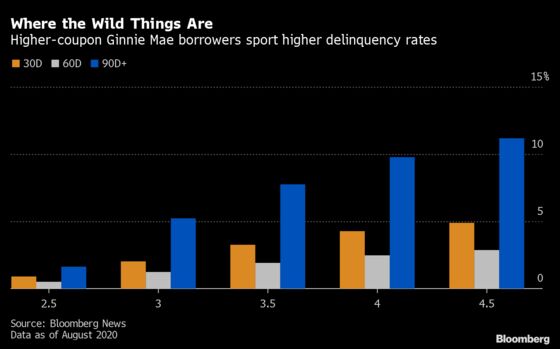

Ginnie Mae is known to cater to homeowners of lower credit quality, and the forbearance numbers highlight the difference. The average FICO score for the Ginnie Mae II 30-year borrower is 705, whereas for the conventional 30-year borrower it’s 758.

When borrowers fall into forbearance and delinquency, this heightens the risk that the loan will eventually go into default and need a buyout, which for mortgage investors are prepayments by another name as it will be bought out at par. This can weigh on portfolio performance.

While the percentage of Ginnie Mae homeowners in forbearance did drop by 50 basis points in the latest report, “at least a portion of the decline in the Ginnie Mae share was due to servicers buying delinquent loans out of pools and placing them on their portfolios,“ said Mike Fratantoni, the MBA’s senior vice president and chief economist.

Looking at the delinquency data for Ginnie Mae II 30-year borrowers shows the issue is particularly acute in the higher coupons. For instance, while the 4.5% of 2016 through 2019 vintages sport 90+ day delinquency rates that average 13.7%, according to data compiled by Bloomberg, the 3% coupon of the same vintages show a relatively paltry 7.2%.

The trend may get worse for Ginnie Mae MBS investors before it gets better. “Forbearance requests increased over the week, particularly for Ginnie Mae loans,” Fratantoni said. “With just under 1 million unemployment insurance claims still being filed every week, the lack of additional fiscal support for the unemployed could lead to even higher increases of those needing forbearance.”

- Christopher Maloney is a market strategist and former portfolio manager who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2020 Bloomberg L.P.