Laggards for a Decade and Counting: Emerging-Market Stocks

Lost Decade Lingers as Emerging-Market Stocks Trail U.S. Peers

(Bloomberg) -- The beginning of the end of cheap money was heralded as the moment emerging-market stocks would reverse a decade spent in the shadow of their developed-nation peers.

It’s turning out to be anything but.

After a three-week rally in October that briefly raised hopes of a comeback, the benchmark gauge for the group has sunk back, reaching a 20-year low relative to its main U.S. counterpart. That’s providing early evidence that while global markets are adjusting to the idea of less stimulus from central banks including the Federal Reserve, emerging markets are failing to get much traction.

It’s a familiar story. Despite faster growth and cheaper valuations, developing-nation equities have trailed the U.S. for most of the past 11 years. But, as Fed tapering loomed, money managers including Goldman Sachs Group Inc. and Bank of America Corp. saw a new commodity cycle and corporate growth ushering in an era of primacy for them. Instead, what some investors have described as the emerging-market “lost decade” only seems to be extending.

“U.S. stocks received more flow than emerging-market stocks because fundamentally they are a better story,” said Daniel Gerard, a senior multi-asset strategist at State Street Global Markets in Boston. Investors will this week see how reports on economic activity from China to Russia and Brazil add to that narrative.

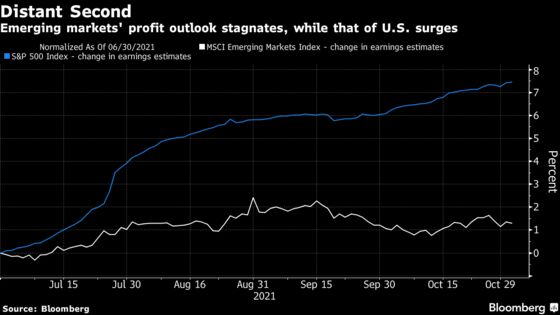

Fundamental Flaw

The MSCI Emerging Markets Index has dropped about 2% this year, compared with a 25% rally in the S&P 500 Index. That’s driven the ratio between the two gauges to the lowest since December 2001. While developing-nations stocks are 40% cheaper than their U.S. peers, a poorer earnings outlook is discouraging investors from buying into that discount.

“We remain cautious on emerging-market equities and prefer to be overweight across developed markets,” said Patrik Schowitz, a global multi-asset strategist at JPMorgan Asset Management in Hong Kong. Performance headwinds have “added up to much weaker earnings delivery in emerging markets than in developed markets.”

Since October 2010, the S&P 500 has soared almost 300% while the emerging-market gauge has added a paltry 14%. The latter also trailed behind Europe and Japan during this period. The market value of U.S. stocks has surged by $39 trillion, while all the designated emerging markets combined added less than $16 trillion.

Tighter monetary conditions may still spark larger capital flight from the U.S., where positioning has been ultra long for years. Yet, emerging markets remain too weak to capitalize on that vacuum as their relative growth advantage shrinks, investors say.

Emerging economies expanded an average 2.4 percentage points faster than developed countries in the six years before Covid-19. That differential has shrunk to an estimated 1.2 percentage points this year as developing nations fail to match richer countries in providing fiscal and monetary support to their economies. The spread isn’t expected to widen again before 2023.

Central to all this is China, which accounts for 42% of emerging markets by stock capitalization. Debt deleveraging and a regulatory clampdown are threatening to shift trend growth in the world’s second-biggest economy to below 6% a year. President Xi Jinping’s “common prosperity” program also has the effect of taking the country back to communist principles of yore.

China’s High Stakes Common Prosperity - GDP Scenarios

Analysts are turning skeptical on corporate performance in the developing world. Average 12-month profit estimates for the members of the MSCI index have stagnated in the second half, while they have increased about 7.5% for the S&P 500.

These are the events and data to look out for this week:

- Leaders of China’s Communist Party gather for a crucial political meeting from Monday through Thursday, in which President Xi Jinping could lay the ground for extending his term as leader

- Even as Xi looks set to rule indefinitely as China’s most powerful leader since Mao Zedong, that doesn’t mean he always gets what he wants. Recent policy actions show the difficulty he faces managing a sprawling bureaucracy in the world’s second-biggest economy

- Inflation data Wednesday will probably show another surge in factory-gate prices to a fresh 26-year high and a pick-up in costs for consumers

- China’s export growth beat expectations in October as foreign demand for its goods continued to surge, despite global supply-chain disruptions, data over the weekend showed

- Mexico’s central bank will probably increase the benchmark rate on Thursday, with data on Tuesday set to show that inflation continued to accelerate in October

- Policy makers in Peru are also set to lift borrowing costs on Thursday as inflation expectations rise

- Thailand’s central bank is likely to keep its benchmark rate unchanged on Wednesday

- South African Finance Minister Enoch Godongwana will present his first medium-term budget on Thursday. A revenue windfall from higher commodity prices and changes to the way GDP is calculated are likely to lead to an improvement in key fiscal metrics

©2021 Bloomberg L.P.