Locked Out of Credit Party, CLOs Flash Cash to Do Deals

Locked Out of Credit Party, CLOs Flash Cash to Get Deals Done

(Bloomberg) -- In what’s shaping up to be a vintage year for many credit investors, the corks aren’t popping in every corner of the market.

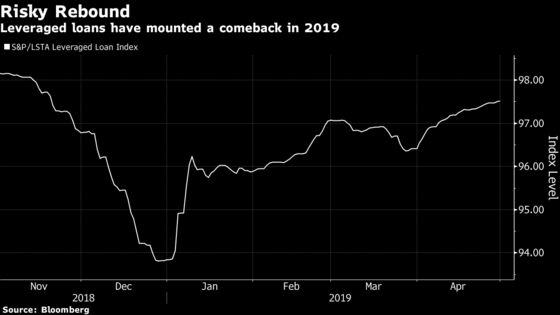

The risk rally pushing leveraged loans ever higher is largely bypassing collateralized loan obligations, the bonds formed when such corporate debts get packaged together.

It’s eating away at the margins that drive the creation of one of Wall Street’s hottest products, and making life a little harder for the managers who bundle them up. A year after rules requiring firms to hold a chunk of their own CLO deals were scrapped, evidence suggests they’re increasingly opting to do so of their own accord.

Put another way: CLO managers are taking on more risk themselves to make it easier to get deals done.

“CLOs getting issued have required more equity support from the manager compared to last year,” said Jim Schaeffer, the deputy chief investment officer at Aegon Asset Management in Chicago. “Managers are being asked to buy a portion of the equity to get deals done.”

Schaeffer’s own firm has retained a small part of one deal, though “nowhere near a control piece,” he said.

Rising Yield

It’s the latest chapter in the story of the $740 billion global market for CLOs, and it stems from the fact the frenzy surrounding them is starting to cool.

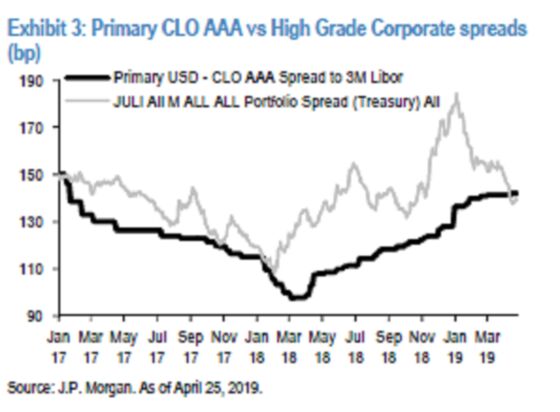

The average yield investors demand to own AAA rated U.S. CLOs has surpassed that on investment-grade corporate bonds for the first time since January 2018, JPMorgan Chase & Co. said last month.

Thank the Federal Reserve’s dovish pivot earlier in the year. Since the interest paid by CLOs moves up and down with benchmark rates, they get less appealing if the Fed is on pause.

CLO managers buy loans that they slice and dice into bonds and equity with varying risk to investors. The securities work by arbitraging the gap between the interest income from the loans and the coupons on each CLO.

If loans default, equity pieces are first to absorb the losses. There’s no public data on how much of that risk is being retained by managers, so it’s hard to show an up-tick -- but market participants acknowledge the shift.

“Managers who can are retaining equity,” said Asif Khan, a managing director and head of CLOs at MUFG Securities. “In this environment it’s giving them a leg up in getting their deals done.”

No Distress

That’s an important point: None of this equates to a distress signal from the industry. For some firms, retaining equity is a standard part of their investment process, while many still have cash left over from before the risk-retention regulations were relaxed. They want to put it to work -- particularly if it makes a deal easier to sell.

“In order to increase the certainty of deal execution and reduce the uncertainty associated with challenging equity arbitrage for third party investors, managers who have the capital are retaining equity,” said MUFG’s Khan. That makes CLO sellers “better able to control their own destiny,” he said.

Meanwhile, the CLO market may have got tougher, but that’s not the same as being tough -- issuance has continued apace in 2019. As of last week, some $45.6 billion in new deals had been issued this year, versus $44.7 billion in the same period a year earlier.

As Aegon markets its latest deal, conditions do seem to be getting a bit more favorable, according to Schaeffer.

“It feels like it is more receptive that it was early in the year,” he said. Though it’s “still not an easy market,” he added.

There may be scope for a recovery in CLO spreads with the Fed recently adopting a more neutral tone, Wells Fargo Securities strategists argued in a note Monday.

Arbitrage Squeeze

In ideal conditions, most CLO managers would prefer to sell the riskier equity portion of a deal to a third party.

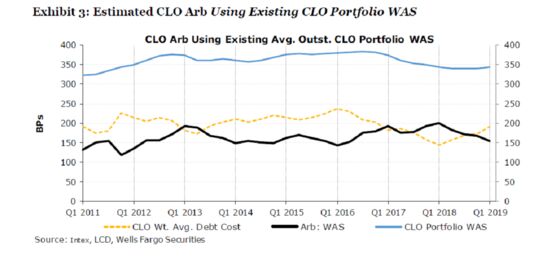

But interest has cooled as the arbitrage that makes CLOs lucrative has shrunk. It’s now the narrowest since the first quarter of 2016, according to Wells Fargo.

That’s because leveraged loans have been doing better than CLOs, even though they also have floating-rate interest and have suffered fund outflows since the Fed pivot. The loans pay higher interest, giving them a broader base of investors, many of whom joined this year’s risk rally.

The fact firms are opting to retain their own equity does hint at some level of discomfort. In doing so they may well be accepting below market returns on their investment, not to mention that equity tranches have missed out on some CLO price gains this year.

Yet the combination of narrowing arbitrage and the legacy of risk-retention rules means CLO managers appear ready to put more skin in the game.

“We plan on raising additional CLO equity funds so that we can continue to participate in the majority equity of our deals and we believe other managers will do so as well,” Mark Sanofsky, a managing director at CIFC Asset Management in New York, said by email. “We think this is a trend that will continue and is not just a function of a difficult market.”

--With assistance from Adam Tempkin.

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Charles Williams in New York at cwilliams204@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Christopher DeReza

©2019 Bloomberg L.P.