Libor’s Heir Hindered by Repo Volatility in Battle of Benchmarks

Last month’s jump in rates on overnight Treasury repurchase agreements pushed the benchmark higher by almost 70 basis points.

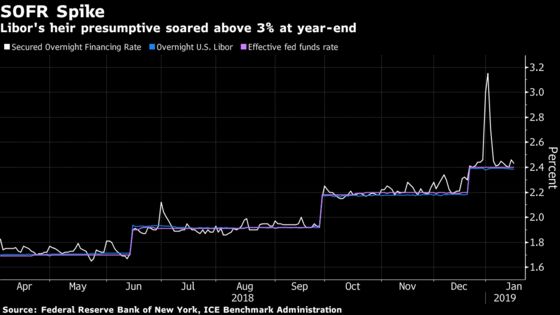

(Bloomberg) -- The benchmark being eyed as a potential replacement for dollar Libor is facing renewed scrutiny after a year-end surge in the market underpinning the new rate. With more volatility possible, Wall Street is increasingly wondering if the nascent Secured Overnight Financing Rate will be up to the task.

Last month’s jump in rates on overnight Treasury repurchase agreements -- the market that supports SOFR -- pushed the benchmark higher by almost 70 basis points over a two-day span. It has since retreated and was set at 2.43 percent for Wednesday. But given that both repo and SOFR are also susceptible to swings in Treasury-bill supply, which itself could become more erratic as the U.S. grapples with the reintroduction of the debt ceiling, some market veterans are forecasting further fluctuations ahead.

Concerns about SOFR range from a lack of term structure to tepid volumes in derivatives that are tied to it. And that has traders and strategists saying the new rate needs to make significant headway in 2019 if U.S. regulators expect it to eventually take the baton from Libor, which still underpins more than $200 trillion of dollar-denominated instruments.

“It’s good to learn we have these issues, but it also suggests we should be looking for something else,” said Ward McCarthy, chief financial economist for Jefferies LLC. Regulators have “really have put a lot of work into developing this and trying to garner acceptance of it. But the bottom line is performance.”

That’s not to say the benchmark, administered by the Federal Reserve Bank of New York, is doomed. The U.S. Treasury is exploring the prospect of selling SOFR-linked notes. Issuers running the gamut from government agencies to banks and municipalities have priced more than $30 billion of debt tied to the reference rate so far.

And the International Swaps and Derivatives Association -- along with other industry groups -- is pushing ahead on fallback language for contracts still tied to the London interbank offered rate. In addition, it appears a near certainty that there will be further regulatory efforts to promote greater adoption ahead of Libor’s intended phase out by the end of 2021.

Here’s where SOFR stands as its quest for credibility continues:

The Headwinds

- Underlying Volatility: Funding rates surged at the end of 2018, spurred by a combination of primary dealer balance sheets loaded with Treasury collateral and a regulatory-induced pullback by those firms from the repo market. SOFR was among the rates sent soaring, and although the benchmark has largely printed in line with expectations since its April debut, this recent bout of volatility underscores how funding conditions could rile the rate going forward.

- The susceptibility of repo rates to swings in Treasury-bill issuance and expectations for seesawing supply surrounding the U.S. government’s debt ceiling may inject more instability.

- In an environment where banks are reducing their excess reserve balances, “repo rates and consequently SOFR will likely only become more volatile,” JPMorgan Chase & Co. strategists led by Alex Roever wrote in a note earlier this month.

- Term Structure Impediments: Because SOFR is derived from overnight repo transactions, there is no term structure similar to that of Libor-based derivatives. Instead, SOFR futures are derived using a compounded calculation over the prevailing period -- either three months or one month. This could make market participants more wary of using SOFR-derived products, depriving these nascent contracts of depth and liquidity.

- Lack of Volume: In its paced transition plan, the Alternative Reference Rates Committee, tasked with developing and implementing SOFR, said that increased trading activity in derivatives tied to the benchmark will facilitate the creation of an indicative term structure. Yet volumes in both futures and swaps remain tepid.

- Total open interest in three-month SOFR futures contracts is roughly 30,000, down from about 42,000 on Dec. 18. On the swaps side, there were 52 SOFR-linked trades in 2018 totaling $6.3 billion in notional value, ISDA data show. There were more than 600,000 Libor-based trades totaling roughly $111 trillion in notional value over the same span.

- “It’s hard to create liquidity from no liquidity,” said Darrell Duffie, a professor at Stanford University who is working with the ARRC on a mechanism for converting Libor swaps to SOFR swaps.

The Tailwinds

- The FHLBs Are Showing Up: Even as some market participants remain wary about adopting SOFR, others are plowing ahead. On Jan. 15, the Federal Home Loan Banks -- the largest issuers of short-term Libor-tied debt -- sold $2.75 billion of SOFR-linked notes in a two-part offering. It’s the entity’s third deal since November.

- The first SOFR-tied floaters from issuers such as the FHLBs that come under the aegis of the Federal Housing Finance Agency have been the “beginning of an intimate dance of what these bonds are going to look like,” according to Jack Phelps, the principal examiner at the FHFA.

- Enter Treasury: The U.S. government is examining how issuance tied to the new benchmark could fit into its overall debt strategy. In a questionnaire released ahead of the Treasury’s quarterly refunding announcement later this month, the department asked primary dealers for their perspectives on the potential debut of issuance tied to SOFR. Specifically, the Treasury asked whether SOFR-linked debt would broaden and diversify its investor base, or reduce demand for and liquidity in existing securities. Should the Treasury decide to issue SOFR-linked debt, strategists say it would be a major step toward facilitating wider adoption.

- Pressing Forward: Despite market participants’ reservations, regulators and industry groups are still preparing for the end of Libor in just under three years. The ARRC expects to introduce an indicative term rate sometime in the first-quarter, according to spokesman Andrew Gray, and the committee is also soliciting feedback on fallback language for bilateral loans and securitizations.

--With assistance from Yalman Onaran.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.